Offshore banking can protect your wealth, diversify finances, and hedge against currency fluctuations. For U.S. citizens, it’s legal but requires strict compliance with IRS and FinCEN rules. Here’s what you need to know:

- Key Compliance Requirements:

- FBAR (FinCEN Form 114): File if foreign accounts exceed $10,000 in aggregate during the year. Due April 15 (automatic extension to October 15).

- FATCA (Form 8938): File with your tax return if foreign assets exceed thresholds (e.g., $50,000 for single filers living in the U.S.).

- Report worldwide income, including income from offshore accounts.

- Penalties for Non-Compliance:

- FBAR: Up to $17,000 for non-willful violations; 50% of account balance or $100,000 for willful violations.

- FATCA: $10,000 for initial failure, up to $50,000 for continued non-compliance, plus a 40% penalty on underreported taxes.

- Choosing a Jurisdiction:

- Cayman Islands: Strong asset protection, high deposit requirements.

- Singapore: Stable, multi-currency options, strict regulations.

- Switzerland: Wealth preservation, privacy within legal limits.

- Nevis: Affordable asset protection, strong creditor barriers. Many investors combine these accounts with offshore trusts for enhanced security.

- How to Open an Account:

- Documents needed: Passport, proof of residence, IRS Form W-9, proof of funds.

- Choose banks compliant with FATCA and familiar with U.S. clients.

- Minimum deposits vary widely (e.g., $5,000–$1,000,000+).

Offshore banking is a valuable tool when done legally. Stay compliant by meeting reporting deadlines and consulting a tax professional to avoid costly penalties.

US Compliance Rules for Offshore Banking

The U.S. government allows offshore banking but requires full transparency. If you hold funds in foreign accounts, you’re obligated to report them. There are two main reporting systems for this – FBAR and FATCA – and they operate independently. Filing one does not exempt you from filing the other.

Both systems aim to deter tax evasion and ensure global income reporting. Under FATCA, foreign financial institutions directly report your account details to the IRS, providing third-party verification of your filings.

FATCA (Foreign Account Tax Compliance Act) Requirements

FATCA requires you to file Form 8938 if your foreign assets exceed specific thresholds:

- For single U.S. residents: $50,000 at year-end or $75,000 at any point during the year.

- For joint filers: $100,000 at year-end or $150,000 at any time.

- For those living abroad: $200,000 at year-end or $300,000 during the year for single filers; $400,000 or $600,000 for joint filers.

What counts as reportable? Foreign bank accounts, foreign stocks or securities held outside a U.S. bank, interests in foreign partnerships or corporations, foreign mutual funds, and foreign-issued life insurance with cash value. However, accounts in U.S. branches of foreign banks are excluded.

When converting foreign currency balances to U.S. dollars, use the Treasury Bureau of the Fiscal Service exchange rate from the last day of the tax year. Be sure to keep detailed records – like account names, numbers, and maximum values – for at least five years.

FBAR (Report of Foreign Bank and Financial Accounts) Filing

FBAR, or FinCEN Form 114, is filed separately from your tax return through the Financial Crimes Enforcement Network’s BSA E-Filing System. You must file an FBAR if the total value of your foreign financial accounts exceeds $10,000 at any time during the calendar year. This lower threshold means some individuals who aren’t required to file FATCA’s Form 8938 still need to file an FBAR. It applies to U.S. citizens, residents, and domestic legal entities.

FBAR filings are due by April 15, with an automatic extension to October 15. If you jointly own an account, each owner must report the full account value. However, spouses can file a single FBAR if all accounts are jointly held, provided they complete Form 114a.

IRS Penalties for Missing Reports

Failing to file FBAR or FATCA reports can result in harsh penalties. For FBAR, non-willful violations can lead to penalties of up to $17,000 per year. Willful violations are even more severe – 50% of the account balance or $100,000, whichever is greater.

For FATCA, failing to file Form 8938 results in an initial penalty of $10,000. If the IRS notifies you and you still don’t comply, additional penalties of $10,000 may apply every 30 days, up to a maximum of $50,000. On top of that, a 40% penalty can be imposed for any tax understatement tied to undisclosed foreign assets.

Serious violations may lead to criminal charges, including up to five years in prison and hefty fines. Failing to report over $5,000 in gross income or neglecting to file Form 8938 can also extend the statute of limitations on your tax return to six years – or indefinitely in some cases.

If you can prove “reasonable cause” for not filing, penalties might be waived, depending on the circumstances. For missed filings, the IRS offers two programs to help: the Streamlined Filing Compliance Procedures for non-willful violations and the Voluntary Disclosure Program for willful violations, which can help reduce or eliminate penalties.

Next, explore how to choose an offshore banking jurisdiction that aligns with these compliance rules.

sbb-itb-39d39a6

How to Select an Offshore Banking Jurisdiction

Picking the right offshore banking jurisdiction means finding a balance between financial stability, strong regulation, and compliance with U.S. laws. It’s crucial to choose a country with a solid political and economic foundation to avoid risks like government interference or financial instability. At the same time, you’ll need a bank that welcomes U.S. citizens – many smaller institutions now turn away Americans because of the high costs associated with FATCA compliance.

"The most important thing for Americans is complying with tax reporting requirements. This means finding a reputable offshore bank in a stable jurisdiction that’s compliant with the Foreign Account Tax Compliance Act (FATCA)." – Nomad Capitalist

Instead of large, brand-name banks, consider boutique institutions. These often have healthier deposit-to-loan ratios and are regulated by top-tier authorities like MAS (Singapore), FINMA (Switzerland), or CIMA (Cayman Islands).

Key Factors to Consider

- Deposit Protection: Check if the jurisdiction offers deposit insurance. For example, Singapore’s SDIC covers up to SGD 75,000, and Hong Kong protects up to HKD 500,000 per depositor.

- Multi-Currency Support: Holding funds in currencies such as Swiss francs (CHF), Singapore dollars (SGD), or euros (EUR) can act as a hedge against fluctuations in the U.S. dollar.

- Compliance Standards: Ensure the jurisdiction adheres to Global Anti-Money Laundering (FATF) and OECD tax transparency standards. Non-compliant jurisdictions risk having transactions flagged by correspondent banks. With over 100 countries sharing financial data under CRS, offshore account details are automatically reported to the IRS.

Privacy within legal limits is possible, but secrecy is not. Below are examples of jurisdictions that meet these criteria.

Cayman Islands

The Cayman Islands serves as a hub for institutional offshore banking rather than a secrecy haven. With a legal system rooted in English common law, it offers robust asset protection frameworks, making it ideal for investment funds, trusts, and complex corporate structures. The jurisdiction is transparent with U.S. authorities and fully compliant.

"Cayman offshore banking is best understood as institutional offshore banking, not secrecy banking." – OCBF Consulting

Cayman banks typically require minimum deposits ranging from $10,000 to $100,000 or more. Many also prefer in-person account openings or require intermediaries. With oversight from the Cayman Islands Monetary Authority (CIMA), this jurisdiction is better suited for complex investment needs rather than everyday banking.

Singapore

Singapore is a standout choice due to its political stability, strict regulation, and multi-currency account options. The Monetary Authority of Singapore (MAS) enforces some of the most respected banking oversight globally, making it a popular destination for high-net-worth individuals.

Standard accounts in Singapore require deposits of $1,000 to $5,000, while private banking typically starts at $250,000. The SDIC insurance scheme protects deposits up to SGD 75,000. Singapore also offers opportunities for remote account opening through licensed fintech platforms, though some banks still require a physical presence.

For U.S. citizens, Singapore is particularly appealing for digital banking services and access to ASEAN markets. However, its strict Know Your Customer (KYC) rules mean you’ll need to provide detailed documentation, including high-resolution passport scans and proof of wealth. This combination of regulatory trust and technological advancement makes Singapore an excellent option for Americans with business interests in Asia.

Switzerland

Switzerland remains a top choice for U.S. citizens focused on long-term wealth preservation. Known for its tradition of wealth management and strong financial privacy within legal limits, it operates under rigorous oversight from the Swiss Financial Market Supervisory Authority (FINMA). Additionally, the Swiss franc (CHF) offers a reliable way to diversify currency holdings.

"Switzerland continues to stand out as a leading choice for Americans thanks to its financial stability, respected banking tradition, strong regulatory framework, and the strength of the Swiss franc." – WHVP

Swiss private banks cater primarily to high-net-worth individuals, with minimum deposits ranging from $250,000 to over $1 million. Most banks require in-person visits to open accounts, and U.S. citizens must work with SEC-registered advisors to ensure compliance with American regulations. While some standard accounts have lower deposit requirements, Switzerland is best suited for private wealth management rather than everyday banking. Maintenance fees can range from $200 to several thousand dollars annually, depending on the account type.

Anguilla and Nevis

Anguilla and Nevis are known for strong asset protection laws, low taxes, and legal safeguards against frivolous lawsuits. These jurisdictions are popular for setting up asset protection structures like Nevis foundations and LLCs, which also benefit from tax exemptions for income earned outside their borders. Both operate under English common law and maintain stable regulatory environments. Nevis, in particular, offers significant legal hurdles for creditors.

These locations are ideal for U.S. citizens looking to protect assets rather than for everyday banking. Often combined with offshore company formations, they provide a shield against lawsuits or aggressive creditors. Both jurisdictions are fully compliant and report account data to the IRS, ensuring transparency with U.S. tax authorities.

This overview highlights jurisdictions that combine stability, deposit protection, and strong regulatory oversight, helping you make an informed decision.

How to Open a Compliant Offshore Bank Account

Opening an offshore bank account as a U.S. citizen is entirely legal, as long as you follow the necessary steps and comply with reporting requirements. The process involves preparing the right documentation, selecting a bank that works with U.S. clients, and staying informed about your tax responsibilities. Banks will thoroughly verify your identity and financial background through Know Your Customer (KYC) and Anti-Money Laundering (AML) checks.

Documents You’ll Need

To open an offshore account, you’ll need certain essential documents:

- A valid U.S. passport with at least 18 months of validity left.

- Proof of residence, such as a recent utility bill, lease agreement, or bank statement.

- Your Social Security Number (SSN) and a completed IRS Form W-9 to comply with FATCA reporting requirements.

Additionally, most banks will ask for proof of how you earned your funds. This could include wage slips, investment statements, sales contracts, or inheritance documents. Be prepared to provide 6–12 months of bank statements. Some jurisdictions may also require you to submit notarized or apostilled documents, so it’s worth confirming those requirements ahead of time.

Choosing Your Bank and Account Type

Not all offshore banks are open to U.S. citizens, primarily because of the compliance burden imposed by FATCA. Focus on well-established banks that are equipped to handle FATCA reporting, with trained staff and appropriate infrastructure.

Deposit Requirements:

- Traditional private banks often require higher minimum deposits, starting around $100,000.

- Digital multi-currency platforms are more accessible, with minimum deposits ranging from $5,000 to $25,000.

Service Options:

Traditional banks provide a full range of services, including loans and investment options, but they may require in-person visits and extensive paperwork. On the other hand, fintech platforms offer quicker digital onboarding, lower currency conversion fees (typically around 1%), and are ideal for managing foreign income.

Approval Times:

- Digital accounts: 1–3 business days.

- Corporate accounts: Up to 12 weeks.

When choosing a bank, prioritize those under strong regulatory oversight, such as MAS in Singapore, FINMA in Switzerland, or CIMA in the Cayman Islands. Avoid institutions that promise secrecy or fail to request your W-9 form, as these are red flags.

Tax Reporting and Disclosure Requirements

Compliance with U.S. tax laws is a critical part of offshore banking. If your foreign accounts exceed $10,000 at any point during the year, you must file an FBAR. Additionally, FATCA Form 8938 is required if your specified foreign assets cross certain thresholds. For more details on these thresholds, refer to the "US Compliance Rules for Offshore Banking" section.

"Under FATCA, certain U.S. taxpayers holding financial assets outside the United States must report those assets to the IRS on Form 8938." – IRS.gov

Keep in mind that filing one form does not exempt you from filing the other. Penalties for failing to comply can be steep: non-willful FBAR violations can result in fines of up to $10,000 per year, while willful violations may lead to penalties exceeding $100,000 or 50% of the account balance per violation.

To stay compliant, maintain detailed records of all foreign transfers and maximum account balances for at least five years. This will help you meet IRS and FinCEN audit requirements. Given the complexity of these obligations, consulting a tax professional before opening your account is a smart move to avoid potential pitfalls.

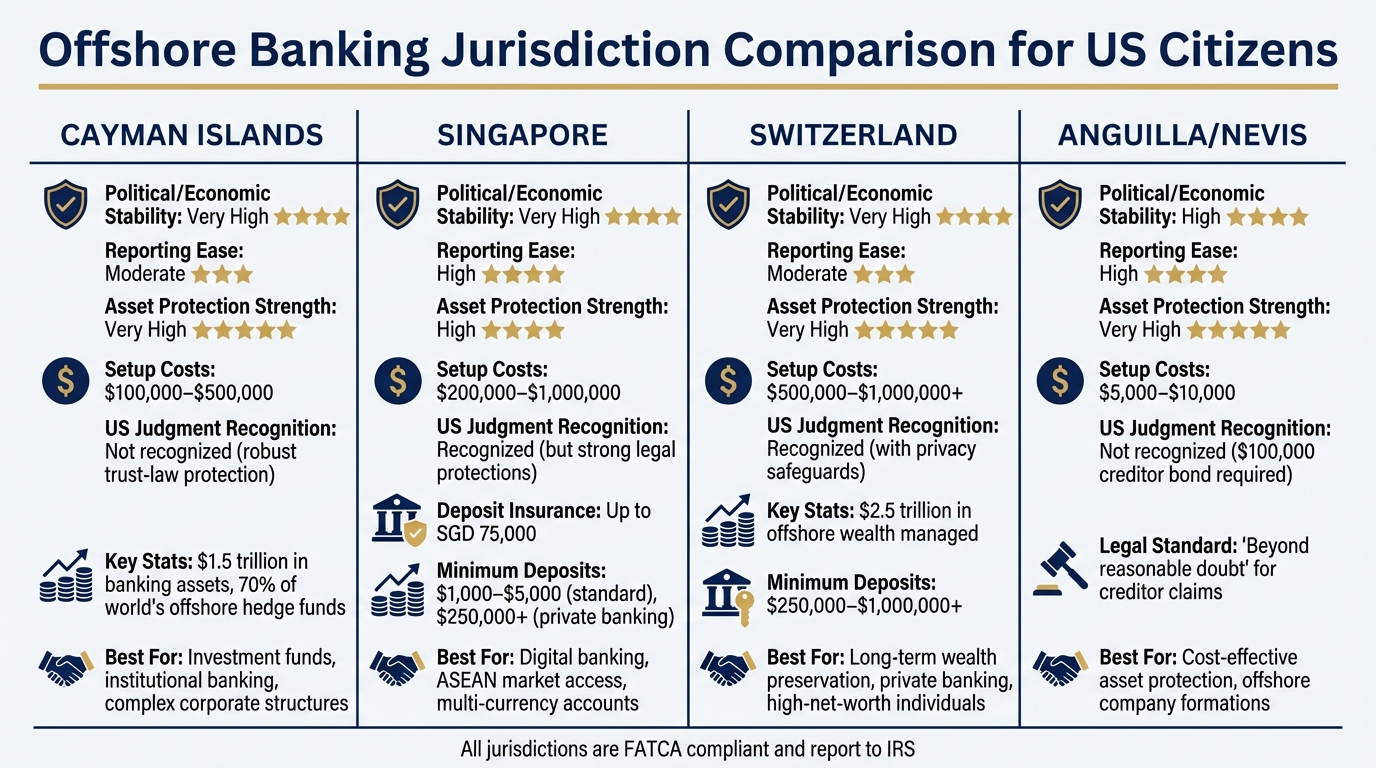

Offshore Banking Jurisdiction Comparison

When considering offshore banking, it’s crucial to align your choice of jurisdiction with your financial goals – whether that’s asset protection, digital convenience, or long-term security. Each jurisdiction has unique strengths and challenges, particularly in terms of regulatory environment, setup costs, and how U.S. judgments are enforced. Understanding these distinctions is key to making an informed decision.

Jurisdiction Comparison Table

The table below provides a snapshot of four prominent offshore banking jurisdictions. It evaluates factors like Political/Economic Stability, Reporting Ease (compliance with U.S. requirements), Asset Protection Strength, Setup Costs, and U.S. Judgment Recognition (how easily U.S. creditors can enforce claims).

| Jurisdiction | Political/Economic Stability | Reporting Ease | Asset Protection Strength | Setup Costs | U.S. Judgment Recognition |

|---|---|---|---|---|---|

| Cayman Islands | Very High | Moderate | Very High | $100,000–$500,000 | Not recognized due to robust trust-law protection |

| Singapore | Very High | High | High | $200,000–$1,000,000 | Recognized (but strong legal protections) |

| Switzerland | Very High | Moderate | Very High | $500,000–$1,000,000+ | Recognized (with privacy safeguards) |

| Anguilla/Nevis | High | High | Very High | $5,000–$10,000 | Not recognized ($100,000 creditor bond required) |

Analysis of Key Jurisdictions

Cayman Islands

The Cayman Islands manage an impressive $1.5 trillion in banking assets and are home to around 70% of the world’s offshore hedge funds. With high minimum deposit requirements, this jurisdiction is best suited for investment funds and corporate entities rather than individual banking. Its robust trust laws ensure strong asset protection, making it a go-to choice for shielding wealth.

Singapore

Singapore excels in safety and innovation, with banks like DBS, OCBC, and UOB consistently ranked among the safest globally. It’s a hub for cross-border trade and digital banking, with fintech platforms enabling remote account setup. For those seeking a blend of modern banking convenience and strong legal protections, Singapore is an attractive option.

Switzerland

Switzerland remains synonymous with private banking, managing over $2.5 trillion in offshore wealth. Although it adheres to global transparency standards like CRS and FATCA, its privacy laws – such as Article 47, which criminalizes unauthorized information disclosure – still offer significant client confidentiality. Swiss banks require substantial deposits but are unmatched in stability and wealth preservation.

Anguilla and Nevis

For those seeking cost-effective asset protection, Anguilla and Nevis stand out. Nevis, in particular, offers a unique legal advantage: creditors must post a $100,000 bond to initiate claims against a trust and meet the demanding "beyond a reasonable doubt" standard of proof. This jurisdiction is ideal for individuals looking for strong protection with minimal setup costs.

Each jurisdiction offers distinct benefits depending on your financial strategy. While asset protection and compliance with U.S. reporting requirements are essential, selecting the right jurisdiction can help you achieve both effectively.

Annual Reporting Requirements and Deadlines

Staying on top of annual reporting deadlines is essential for keeping offshore accounts in good standing. Two critical forms to file are the FBAR (FinCEN Form 114) and FATCA (IRS Form 8938). These filings are necessary to maintain compliance and steer clear of penalties. Let’s break down the key details.

FBAR Filing Deadlines and Thresholds

The FBAR is due on April 15, covering the prior year’s account activity. If you miss this deadline, there’s an automatic six-month extension to October 15, so no need to file a separate extension request. This form is submitted electronically via FinCEN’s BSA E-Filing System and isn’t part of your tax return.

You must file an FBAR if the combined value of all foreign accounts exceeds $10,000 at any point during the year. This is an aggregate threshold, meaning it applies to the total across all accounts – not to each account individually. For example, if you have three accounts with $4,000 each, their combined $12,000 balance triggers the filing requirement.

For joint accounts, each account holder typically reports the entire account value on their FBAR. However, if spouses own accounts jointly, only one FBAR is needed, provided one spouse files on time and both sign Form 114a. Additionally, all foreign currency amounts must be converted to U.S. dollars using the Treasury Bureau of the Fiscal Service exchange rate from December 31 of the reporting year.

"The law requires U.S. persons to report their overseas financial accounts because foreign financial institutions may not be subject to the same reporting requirements as domestic institutions." – IRS

Keep detailed records for at least five years from the FBAR due date. These records should include account names, numbers, the foreign bank’s details, account types, and maximum values during the year. If all data isn’t available by October 15, submit the most complete report possible and amend it later.

FATCA Form 8938 Filing Requirements

FATCA reporting has its own rules and timelines. Form 8938 must be filed with your annual tax return (Form 1040) by April 15. Unlike the FBAR’s flat $10,000 threshold, FATCA thresholds vary depending on your residency and filing status. Check the FATCA section for specifics.

Form 8938 captures a broader range of assets than the FBAR, including foreign stocks, securities, interests in foreign entities, and certain financial instruments held for investment. However, filing Form 8938 doesn’t replace the need to file an FBAR – many individuals must file both.

"FATCA is primarily about transparency, not additional taxation, but ignoring it can still become costly." – Vincenzo Villamena, CPA, Founder and CEO of Online Taxman

Annual Compliance Checklist

To simplify compliance, here’s a quick overview of key tasks, deadlines, and penalties:

| Task | Deadline | Threshold | Penalty for Non-Compliance | Notes |

|---|---|---|---|---|

| FBAR (FinCEN Form 114) | April 15 (auto-extension to Oct 15) | > $10,000 aggregate at any time | Fines; up to 5 years imprisonment | File via FinCEN BSA E-Filing System |

| FATCA (Form 8938) | With tax return (April 15) | Varies ($50,000 – $600,000) | $10,000 initial; up to $50,000 total; 40% tax penalty | See FATCA section for thresholds |

| Income Reporting | With tax return (April 15) | All global income (no minimum) | Interest and accuracy-related penalties | Report all foreign account interest and gains |

| Recordkeeping | Maintain for 5 years | N/A | Potential loss of "reasonable cause" defense | Keep bank statements showing max/year-end balances |

Failure to file Form 8938 can lead to a $10,000 initial penalty, with an additional $10,000 every 30 days after IRS notification, up to a maximum of $50,000. Additionally, any tax understatement linked to undisclosed foreign assets may incur a 40% penalty. Ignoring FBAR rules could result in fines and up to five years in prison.

For those who missed filings due to non-willful conduct, the IRS offers Streamlined Filing Compliance Procedures, which help taxpayers catch up with reduced penalties. When in doubt, it’s safer to over-report borderline assets than to risk leaving out required ones.

Finally, retain copies of all bank statements showing maximum and year-end balances, as the IRS may request proof years later. Opting for foreign institutions that are FATCA-registered and familiar with U.S. clients can also lower the risk of account closures.

Using Global Wealth Protection Services for Offshore Banking

Navigating offshore banking can be tricky, especially with ever-changing FATCA and FBAR regulations. That’s where Global Wealth Protection (GWP) steps in. They specialize in creating IRS-compliant offshore strategies that safeguard assets while keeping U.S. citizens on the right side of tax laws. With 25 years of international expertise and a stellar 4.8/5 rating from 230 reviews, GWP tailors solutions for entrepreneurs and investors alike. Their services integrate seamlessly with the offshore banking strategies outlined earlier.

Offshore Company Formation in Anguilla

Anguilla is a top choice for offshore company formation, known for its privacy protections and tax advantages for U.S. citizens. GWP handles the entire process, including filings, annual reports, document creation, and certification. For those requiring more active asset management, they also offer specialized services like trust administration and private interest foundations designed for high-net-worth individuals.

Another standout service is their ability to connect clients with offshore banks, traditional global institutions, and fintech platforms. This is especially valuable since many foreign banks now turn away American clients due to the high costs of FATCA compliance. By taking the guesswork out of selecting banking partners, GWP ensures clients can access the right institutions without hassle.

Private US LLC for Banking Access

To complement offshore structures, forming a private U.S. LLC can provide additional asset protection while maintaining access to domestic services. GWP offers LLC formation in all 50 states, complete with privacy safeguards and asset protection features like registered agent services and consultations.

Founder Bobby Casey has guided thousands of entrepreneurs in reducing their tax liabilities by 50% to 100% through smart business structuring.

"I’ve helped thousands of entrepreneurs protect their assets from frivolous litigation, cut their taxes by 50-100%, create structures for wealth perpetuation, and properly structure their company for simplicity and tax optimization." – Bobby Casey, Founder, Global Wealth Protection

A U.S. LLC can act as the domestic anchor to your offshore strategy, ensuring seamless banking access while your international setup focuses on wealth preservation.

GWP Insiders Membership Benefits

The GWP Insiders program offers ongoing support for compliance, personalized consultations, and strategic guidance on tax planning and jurisdiction selection. Members gain tools to track reporting deadlines and access IRS amnesty programs like the Delinquent FBAR Submission Procedures (DFSP) and Streamlined Filing Compliance Procedures, which help reduce penalties. Unlike risky "quiet disclosures", GWP emphasizes using official programs to avoid audits or criminal investigations.

They also provide the Global Escape Hatch, a step-by-step action plan for asset protection, residency options, and implementation strategies.

"Your offshore protection strategies should help you – not create tax problems. File now through the proper IRS programs. You’ll become compliant and avoid six-figure penalties or criminal prosecution." – Offshore Protection

Conclusion

Following strict compliance guidelines is essential when engaging in offshore banking. For U.S. citizens, offshore banking is entirely legal, provided all IRS and U.S. Treasury reporting obligations are met. Regulations such as FATCA and the CRS require reputable banks to share foreign account information with the IRS.

Choosing the right jurisdiction can enhance both protection and compliance. For example, Switzerland is known for its stability and multi-currency offerings, Singapore boasts a strong regulatory framework and access to Asian markets, and the Cayman Islands remain a hub for investment opportunities. Minimum deposits in these jurisdictions vary widely, from $5,000 at retail international banks to over $250,000 at private institutions. Opening an account also requires standard documentation, as outlined earlier.

Global Wealth Protection offers expert guidance to help you navigate the complexities of compliance and asset protection. Their services cover every step, from forming offshore companies to connecting with compliant banking institutions, ensuring all U.S. reporting requirements are met.

"Transparency is not only legally required but also protects you from unnecessary risks." – WHVP

FAQs

Do I need to file both FBAR and Form 8938?

Yes, U.S. persons are required to file both forms if they meet the criteria. You must submit the FBAR (FinCEN Form 114) if the total value of your foreign accounts exceeds $10,000 at any time during the year. Additionally, file Form 8938 if your specified foreign financial assets surpass $50,000 for single filers or $100,000 for married couples filing jointly. Non-residents have higher thresholds. It’s important to comply with these regulations to avoid potential penalties.

What’s the safest way to fix missed FBAR/FATCA filings?

The best approach to handle missed FBAR and FATCA filings is through the IRS’s offshore disclosure programs. Options like the Delinquent FBAR Submission Procedures or the Streamlined Filing Compliance Procedures provide a way to voluntarily disclose unreported accounts. These programs can help lower penalties, especially if the oversight was non-willful. It’s a smart move to consult a tax or legal advisor who can evaluate your specific situation and guide you in achieving compliance while reducing potential risks.

How do I choose a FATCA-friendly offshore bank that won’t close my account?

To find an offshore bank that works well with FATCA regulations and reduces the chances of account closures, focus on institutions that don’t have U.S. branches or correspondent banking ties. Look for banks with a solid track record in compliance, financial stability, and a history of working with U.S. citizens. It’s a good idea to consult knowledgeable legal or financial advisors to make sure the bank fits your compliance needs and asset protection strategies. Jurisdictions such as the Cook Islands or Cayman Islands are worth considering due to their clear regulations and strong asset protection frameworks.