Offshore companies can legally reduce taxes by leveraging specific jurisdictions and structures. Here’s how it works:

- Tax-Friendly Jurisdictions: Countries like the Cayman Islands, Singapore, and BVI offer low or zero tax rates on foreign income.

- Company Types: International Business Companies (IBCs) and holding companies and offshore trusts are common setups for tax efficiency and asset management.

- Global Tax Rules: U.S. citizens must comply with FATCA, FBAR, and other strict reporting requirements to avoid penalties.

- Key Benefits: Offshore setups can lower tax burdens, protect assets, and simplify global operations. However, they are cost-effective only for businesses earning over $100,000 annually.

- Compliance Is Critical: Missteps in reporting or structuring can lead to fines and legal issues. Proper planning and transparency are essential.

Offshore structures are effective when paired with the right jurisdiction, proper compliance, and clear business goals. Read on for detailed insights into jurisdictions, costs, and compliance strategies.

Choosing an Offshore Jurisdiction

Selecting an offshore jurisdiction isn’t just about picking a location that sounds appealing – it’s about finding one that matches your tax, legal, and banking needs. A poor choice can lead to challenges like limited banking options, compliance headaches, or a damaged reputation with partners and investors.

Selection Criteria

Start by examining the tax system. Some jurisdictions, like Panama and Hong Kong, use a territorial system, taxing only income earned within their borders. Others, such as the British Virgin Islands (BVI) and Cayman Islands, impose no corporate, income, or capital gains taxes at all on foreign-sourced income.

Double tax treaties are another key factor. For instance, Cyprus has over 60 treaties, while Malta boasts more than 70. These agreements can help reduce withholding taxes on dividends, interest, and royalties. Without such treaties, you could face a hefty 30% withholding tax on cross-border payments.

The banking infrastructure of your chosen jurisdiction is also critical. As one industry expert from Taxus noted:

"A jurisdiction with a poor international reputation may reduce the cost of company formation – but it increases the day-to-day risks for operations, banking, and partnerships."

Jurisdictions with questionable reputations often make it difficult to open bank accounts or work with global payment processors. While forming a company might take just 48 hours, securing a bank account could take up to three months, so it’s vital to research this aspect beforehand.

Lastly, consider the overall cost. This includes not just formation fees but also expenses for local offices (if required), audits, and registered agent services. These factors can add up quickly and should be part of your decision-making process.

Popular Offshore Jurisdictions

Here’s a closer look at some of the most sought-after offshore jurisdictions:

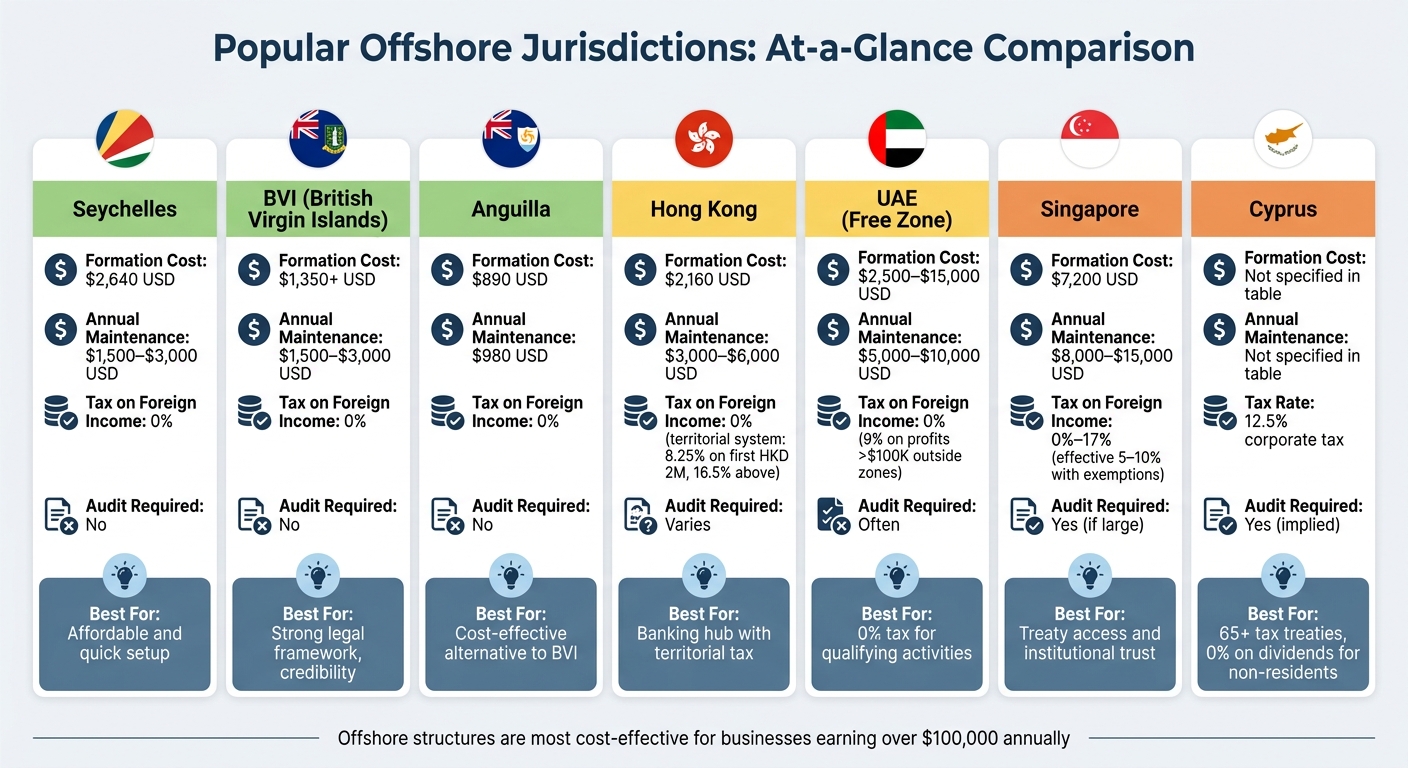

- British Virgin Islands (BVI): Known for its legal framework and asset protection, the BVI exempts foreign income from taxes and doesn’t require a public registry of beneficial owners. Formation fees start at $1,350, with annual maintenance ranging from $1,500 to $3,000.

- Anguilla: Offering similar benefits to the BVI, Anguilla is a more cost-effective option. Registration costs around $890, with annual fees of about $980. It also provides tax exemptions and strong confidentiality protections.

- Hong Kong: Hong Kong uses a two-tiered tax system: 8.25% on the first HKD 2 million (roughly $256,000) of profit and 16.5% on profits beyond that. However, only Hong Kong-sourced income is taxed, leaving foreign income untouched. Its status as a global financial hub makes it ideal for operational companies but less so for those prioritizing privacy.

- Cyprus: With a corporate tax rate of 12.5%, Cyprus offers access to over 65 tax treaties and 0% tax on dividends for non-resident companies. It’s a strong choice for businesses needing treaty access and a foothold in the European market.

- UAE Free Zones: These zones provide a 0% corporate tax rate for qualifying activities, though a 9% corporate tax was introduced in 2023 for profits exceeding $100,000 outside the zones. Formation costs range from $2,500 to $15,000, with annual maintenance between $5,000 and $10,000.

- Singapore: While the corporate tax rate is 17%, effective rates can drop to 5–10% due to various exemptions. Annual costs, typically between $8,000 and $15,000, reflect its reputation as a premium jurisdiction with strong institutional support.

| Jurisdiction | Formation Cost | Annual Maintenance | Key Advantage |

|---|---|---|---|

| Seychelles | $2,640 | $1,500–$3,000 | Affordable and quick setup |

| BVI | $1,350+ | $1,500–$3,000 | Strong legal framework, credibility |

| Anguilla | $890 | $980 | Cost-effective alternative to BVI |

| Hong Kong | $2,160 | $3,000–$6,000 | Banking hub with territorial tax |

| UAE (Free Zone) | $2,500–$15,000 | $5,000–$10,000 | 0% tax for qualifying activities |

| Singapore | $7,200 | $8,000–$15,000 | Treaty access and institutional trust |

Assessing Jurisdiction Risks

When evaluating risks, reputation and compliance status are key. Jurisdictions on FATF grey lists or EU blacklists can face higher withholding taxes and denied tax deductions. For example, Panama improved its reputation by being removed from the EU blacklist on July 9, 2025.

Political and legal stability also plays a big role. Look for jurisdictions with independent courts and established company laws. The Cayman Islands and BVI offer tested legal frameworks, while newer jurisdictions may lack this level of reliability.

Additionally, keep an eye on regulatory changes. Initiatives like the OECD’s Base Erosion and Profit Shifting (BEPS) project and the Common Reporting Standard (CRS) have increased transparency requirements, impacting banking and compliance. The U.S. Corporate Transparency Act now requires entities to disclose beneficial owners to FinCEN, effectively ending anonymous shell companies.

To simplify your decision, consider using a weighted decision matrix. For instance, you might prioritize tax efficiency (40%), reputation (25%), confidentiality (15%), legal stability (10%), and speed (10%). This approach can help balance competing priorities and identify the best fit for your needs.

sbb-itb-39d39a6

Offshore Corporate Structures That Work

Once you’ve selected the right jurisdiction, the next step is choosing a corporate structure tailored to your business goals and compliance needs. This section highlights proven setups designed to minimize taxes legally while staying compliant with U.S. regulations.

International Business Companies (IBCs)

An International Business Company (IBC) is designed to operate outside the country where it’s incorporated, avoiding taxes on foreign-sourced income. Jurisdictions like Seychelles and Panama use territorial tax systems, meaning they only tax income earned within their borders.

IBCs are popular for their confidentiality. Many jurisdictions don’t require public disclosure of shareholders or directors. They also offer flexibility – no need for local directors, minimal reporting requirements, and the ability to hold intellectual property or high-value assets.

Setting up an IBC is quick and affordable. For example:

- Seychelles: Formation takes 3–7 days, costing around $2,640, with annual maintenance fees between $1,500 and $3,000.

- Panama: Formation costs are higher, at $3,840, with annual fees ranging from $5,000 to $10,000.

However, U.S. investors need to follow Controlled Foreign Corporation (CFC) rules. If you own over 10% and U.S. shareholders collectively control more than 50%, the IRS may tax specific types of income, such as dividends, royalties, and interest – even if the funds remain offshore. This is known as "Subpart F income." While IBCs can defer taxes on active business income, they don’t eliminate them entirely.

Banking can be a hurdle. Traditional banks often avoid IBCs, so many entrepreneurs turn to Electronic Money Institutions like Wise or Revolut.

Offshore Holding Companies

While IBCs are ideal for active business operations, holding companies are better suited for managing assets and controlling dividend flows. These companies don’t sell products or services directly – they own other businesses. A holding company can reduce withholding taxes on cross-border payments when set up in a jurisdiction with favorable tax treaties.

Here are a few examples of tax-friendly holding company jurisdictions:

- Singapore: No withholding tax on dividends and access to an extensive treaty network.

- The Netherlands: Offers a "participation exemption", meaning dividends from qualifying subsidiaries aren’t taxed.

- Hong Kong: Uses territorial taxation, so foreign-sourced dividends and capital gains are tax-free.

However, many jurisdictions now enforce Economic Substance Requirements (ESR). For example, the British Virgin Islands, Cayman Islands, and Mauritius require holding companies to maintain a physical presence, hire local staff, and make decisions locally. Without meeting these requirements, tax authorities may refuse to recognize the entity.

U.S. taxpayers must also navigate Passive Foreign Investment Company (PFIC) rules. If 75% or more of the holding company’s income is passive (e.g., dividends or interest), or if over 50% of its assets generate passive income, the IRS imposes punitive taxes, including interest charges on distributions. To avoid this, structure the company to hold active business assets or make a "Qualified Electing Fund" (QEF) election.

Compliance is critical. Missing Form 5471 (for U.S. persons with foreign corporations) triggers a $10,000 penalty per year. Failing to file an FBAR (for foreign accounts over $10,000) can result in penalties of up to $10,000 for non-willful violations – or the greater of $100,000 or 50% of the account balance for willful violations.

Combined Structures for Tax Optimization

For advanced tax strategies, combining multiple entities across jurisdictions can be highly effective. A common setup involves three layers:

- Customer-facing entity: Based in a credible jurisdiction for banking and payment processing.

- Operational entity: Located in a tax-efficient jurisdiction for profit accumulation.

- Holding entity: Used for asset protection and intellectual property ownership.

For instance, you could use a Singapore holding company to oversee a Seychelles IBC. Singapore offers treaty benefits and institutional credibility, while Seychelles provides 0% tax on foreign income and privacy. By making a Check-the-Box (CTB) election with the IRS, the Seychelles entity can be treated as a "disregarded entity" or partnership. This avoids Subpart F inclusion by classifying income based on active business operations instead of passive dividends.

Another effective approach is the Trust-Owned LLC Model. Here, an International LLC serves as the operating company and is wholly owned by an Offshore Trust, often in the Cook Islands or Nevis. Profits flow to the trust, shielding the owner from legal risks because they technically own no domestic assets. As Steven James from OCBF Consulting explains:

"An International LLC acts as the operating company for your business and is wholly owned by the Offshore Trust. This means that all profits filter back to the trust… this is a very secure and private asset protection structure."

The Cook Islands is renowned for asset protection, as it doesn’t recognize foreign court judgments. Setup costs are around $10,000, with ongoing trustee fees. Nevis offers a similar structure for about $9,000, though it faces more frequent legal challenges from the U.S..

Start with Electronic Money Institutions like Wise or Revolut to handle banking, then transition to traditional banks once you establish a transaction history. Remember, a 0% tax rate isn’t helpful if you can’t open a bank account or process payments.

Generally, offshore structures are most cost-effective for businesses generating over $100,000 in annual revenue.

Setup Process and Compliance Requirements

Setting up an offshore structure and staying compliant is essential to enjoy its tax benefits and asset protection. One critical step is verifying banking options before moving forward. As OCBF Consulting aptly states:

"Without banking facilities your offshore company is dead on arrival".

A 0% tax rate won’t help if you can’t access or move your funds.

Formation Steps

The setup process follows a defined order. First, confirm whether banks or Electronic Money Institutions (EMIs) will work with your chosen jurisdiction and business type. For instance, if you’re a U.S. individual forming a Nevis LLC, check if platforms like Wise or Revolut – or your preferred international bank – will open an account for that entity. Many banks steer clear of high-risk industries like crypto due to compliance concerns.

Once banking feasibility is ensured, reserve a company name that meets the jurisdiction’s requirements (e.g., including “Ltd,” “LLC,” or “Inc”) and confirm its uniqueness. Then, prepare the necessary documents, which typically include passport copies, recent proof of address (e.g., utility bills), and a business description. Your registered agent will submit these to the government registry, a process that usually takes 1 to 14 days.

After incorporation, apply for U.S. tax identification numbers. If foreign partners are involved, they’ll need an ITIN to complete Form SS-4 for a FEIN. For banking, use a three-step approach: start with EMIs like Wise or Revolut for immediate functionality (1–7 days), then transition to international banks after building 3–6 months of transaction history. Private banking is an option for those with liquid assets exceeding $1,000,000.

Once the entity is operational, staying compliant is critical to avoid legal or financial penalties.

Ongoing Compliance and Reporting

After incorporation, U.S. persons face specific reporting obligations. If foreign accounts exceed $10,000, file an FBAR. Similarly, Form 5471 is required for foreign corporation ownership, and Form 8938 applies when foreign assets exceed certain thresholds. If you’ve missed filings in previous years, the IRS offers offshore submission programs like the Streamlined Filing Compliance Procedures to help avoid penalties. As the IRS explains:

"Non-willful conduct is conduct that is due to negligence, inadvertence, or mistake or conduct that is the result of a good faith misunderstanding of the requirements of the law".

Local compliance varies by jurisdiction and may include maintaining records or undergoing financial audits. Some jurisdictions, like the British Virgin Islands, Cayman Islands, and Mauritius, enforce Economic Substance Requirements. This means your company must have a physical presence, employ local staff, and make key decisions locally. Additionally, under the Corporate Transparency Act, certain foreign entities must disclose beneficial ownership to FinCEN via the Beneficial Ownership Information (BOI) Registry.

Jurisdiction Comparison Table

| Jurisdiction | Setup Cost | Annual Maintenance | Tax on Foreign Income | Audit Required | Best For |

|---|---|---|---|---|---|

| Anguilla | $890 | $980 | 0% | No | Low-cost IBC with privacy |

| Seychelles | $595 | $850–$1,300 | 0% | No | Privacy, crypto holders |

| BVI | $1,500 | $2,700–$4,900 | 0% | No | Asset protection, holding companies |

| Panama | $3,840 | $5,000–$10,000 | 0% | No | Territorial tax, banking access |

| Singapore | $7,200 | $5,000–$14,200 | 0%–17% | Yes (if large) | Institutional credibility, treaty access |

| UAE (Free Zone) | $2,500–$8,000 | $5,000–$15,500 | 0%–9% | Often | E-commerce, 0% tax on qualifying income |

For an offshore structure to be financially viable, your business should save at least three times the annual maintenance cost in taxes. In many cases, this means generating over $100,000 in annual revenue.

Common Mistakes to Avoid

Even with careful planning, offshore structures can falter if U.S. tax rules are misunderstood or if the legal setup doesn’t align with actual business operations. Missteps often arise from misinterpreting how the IRS views foreign entities, neglecting transfer pricing regulations, or wrongly assuming that incorporating abroad eliminates all U.S. tax responsibilities.

U.S. Tax Rules for Offshore Companies

Owning 10% or more of a foreign corporation that is over 50% U.S.-owned triggers Controlled Foreign Corporation (CFC) status. This means certain types of income – like dividends, interest, and royalties – are taxed immediately, even if the profits remain overseas. Subpart F and Global Intangible Low-Taxed Income (GILTI) rules ensure this income is taxed as soon as it’s earned.

If your offshore entity generates substantial passive income or holds excessive passive assets, it could be classified as a Passive Foreign Investment Company (PFIC). This designation exposes distributions to high interest charges and ordinary income tax rates. Failing to meet filing requirements can be costly: missing Form 5471 can result in a $10,000 penalty, with additional $10,000 increments every 30 days after an IRS notice (up to $50,000 extra). Missing Form 926 triggers penalties of 10% of the transferred value, capped at $100,000. Moreover, the statute of limitations for your entire tax return remains open until these forms are filed.

One way to simplify compliance is through a check-the-box election, which lets you treat a foreign entity as a disregarded entity or partnership. This can bypass some CFC rules and allow income to flow directly to your U.S. tax return. Alternatively, a Section 962 election allows individual shareholders to be taxed at the 21% corporate rate on GILTI income, with access to foreign tax credits.

| Feature | Controlled Foreign Corporation (CFC) | Passive Foreign Investment Company (PFIC) |

|---|---|---|

| Primary Test | Ownership: >50% U.S. owned (by 10% shareholders) | Income/Assets: 75% passive income or 50% passive assets |

| Taxation | Immediate taxation on Subpart F and GILTI income | Taxed on distributions; "excess distributions" incur interest charges |

| Overlap Rule | Takes precedence over PFIC rules for 10% U.S. shareholders | Applies to less-than-10% shareholders in a CFC/PFIC overlap |

| Key Form | Form 5471 | Form 8621 |

Transfer Pricing Compliance

Transfer pricing is another critical area to get right. The IRS requires that transactions between related companies follow the arm’s length principle – essentially, prices should reflect what independent parties would charge under similar circumstances. Under Section 482 of the Internal Revenue Code, the IRS can adjust your income if it suspects profit shifting.

Routing high-margin transactions through offshore entities without real local functions is a red flag. For example, if an offshore company handles sales while all decision-making happens in your New York office, the IRS might reclassify that income as U.S.-sourced. As Ipanema Partners explains:

"The international tax framework now rewards structures where the legal form matches the economic reality."

To defend your profit allocations, document the specific functions, assets, and risks (FAR) managed by your offshore entity. If using a treasury vehicle for lending, ensure the entity has local staff actively managing credit risk and making lending decisions, rather than relying solely on a nominal local director. The IRS expects overseas returns to match the actual work performed there.

Improper transfer pricing can lead to Subpart F income inclusions, especially "foreign base company sales and services income", when a CFC earns profits from related-party transactions involving goods or services outside its country of incorporation. To reduce audit risks, consider the Advance Pricing and Mutual Agreement (APA) program, which allows you to address complex transfer pricing issues with the IRS ahead of time.

Personal Residency Considerations

Your personal residency status also plays a key role in offshore tax planning. Simply incorporating offshore doesn’t lower your tax burden if you’re a U.S. citizen or green card holder. CFC rules apply regardless of where you live. The U.S. taxes worldwide income, and you must meet reporting requirements for foreign entities.

Many offshore structures fail because they lack genuine economic substance in the host country. Current rules require entities to be "directed and managed" locally, with core income-generating activities, adequate staff, and real physical operations in the jurisdiction. As Ipanema Partners cautions:

"The days of a holding company managed entirely from New York with a single nominee director in place are over."

If your offshore entity is effectively controlled from the U.S. – with strategic decisions made stateside – the IRS may treat it as a U.S. resident for tax purposes, regardless of its incorporation location. To achieve legitimate offshore tax benefits, both the corporate structure and personal tax residency must meet compliance standards. Without genuine local management and operational presence, U.S. tax laws may treat the entity as domestic.

Conclusion

Summary of Strategies

Offshore companies can provide legitimate ways to optimize taxes when they’re set up properly and tied to real economic activities. The trick is aligning your corporate structure with your actual business operations. For instance, International Business Companies are ideal for holding assets or managing intellectual property, while offshore holding companies are better suited for protecting dividends and capital gains. Countries like Singapore and Ireland offer solid institutional reputations and tax rates between 5% and 12.5%, while jurisdictions such as Seychelles and the British Virgin Islands (BVI) provide more privacy and lower costs – but they require careful planning, especially when it comes to banking.

Generally, offshore setups make financial sense for businesses earning more than $100,000 annually, where the tax savings outweigh the costs of setup and upkeep. However, tax authorities now demand more than just incorporation paperwork. You’ll need physical offices, local staff, and proof of decision-making within the jurisdiction. This focus on real economic activity, combined with accurate transfer pricing documentation and U.S. reporting, allows these structures to legally reduce or defer taxes while safeguarding your assets.

Once the structure is in place, the next step is ensuring proper banking arrangements and compliance.

Next Steps

With the groundwork laid out, your priority should be confirming whether banking is feasible in your chosen jurisdiction and meeting U.S. compliance obligations. Always follow the "bank first, company second" approach – confirm that banks in your selected location will work with your entity and citizenship before you pay for incorporation. Keep in mind that setting up both the company and the banking relationship can take several months, so plan accordingly.

For U.S. citizens, compliance is non-negotiable, no matter where you incorporate. Navigating rules like Controlled Foreign Corporation (CFC) regulations, GILTI taxation, and mandatory U.S. reporting can be complex. Consulting with professionals is crucial to ensure you’re meeting all requirements while maximizing tax advantages and protecting your assets. Firms like Global Wealth Protection specialize in guiding entrepreneurs and investors through these processes, tailoring offshore structures to fit your business model, revenue level, and long-term goals. Personalized advice can help you choose the right jurisdiction, entity type, and compliance strategy for your specific needs.

FAQs

Will an offshore company eliminate my U.S. taxes?

U.S. citizens and residents are taxed on their worldwide income, no matter where their company is registered. Simply setting up an offshore company won’t get rid of your U.S. tax obligations. To potentially reduce or avoid U.S. taxes, you’d need to relocate outside the U.S. yourself, all while staying compliant with U.S. tax laws.

Which offshore jurisdiction is best for my business?

When choosing the best offshore jurisdiction, it all comes down to your specific needs – whether that’s reducing taxes, maintaining privacy, simplifying the setup process, or streamlining business operations. Popular choices include the British Virgin Islands, Cayman Islands, Seychelles, Singapore, and even U.S. states like Wyoming and Delaware. These locations offer various perks, such as zero corporate taxes or robust asset protection laws. To make the right decision, focus on a jurisdiction that supports your tax strategy, compliance requirements, and overall business objectives.

What U.S. forms do I need to file for an offshore company?

To report foreign disregarded entities and foreign branches, you’ll need to file IRS Form 8858. If the offshore company functions as a foreign corporation involved in U.S. business activities, you’ll also need to file Form 1120-F. Staying compliant with IRS regulations is crucial to avoid potential penalties.