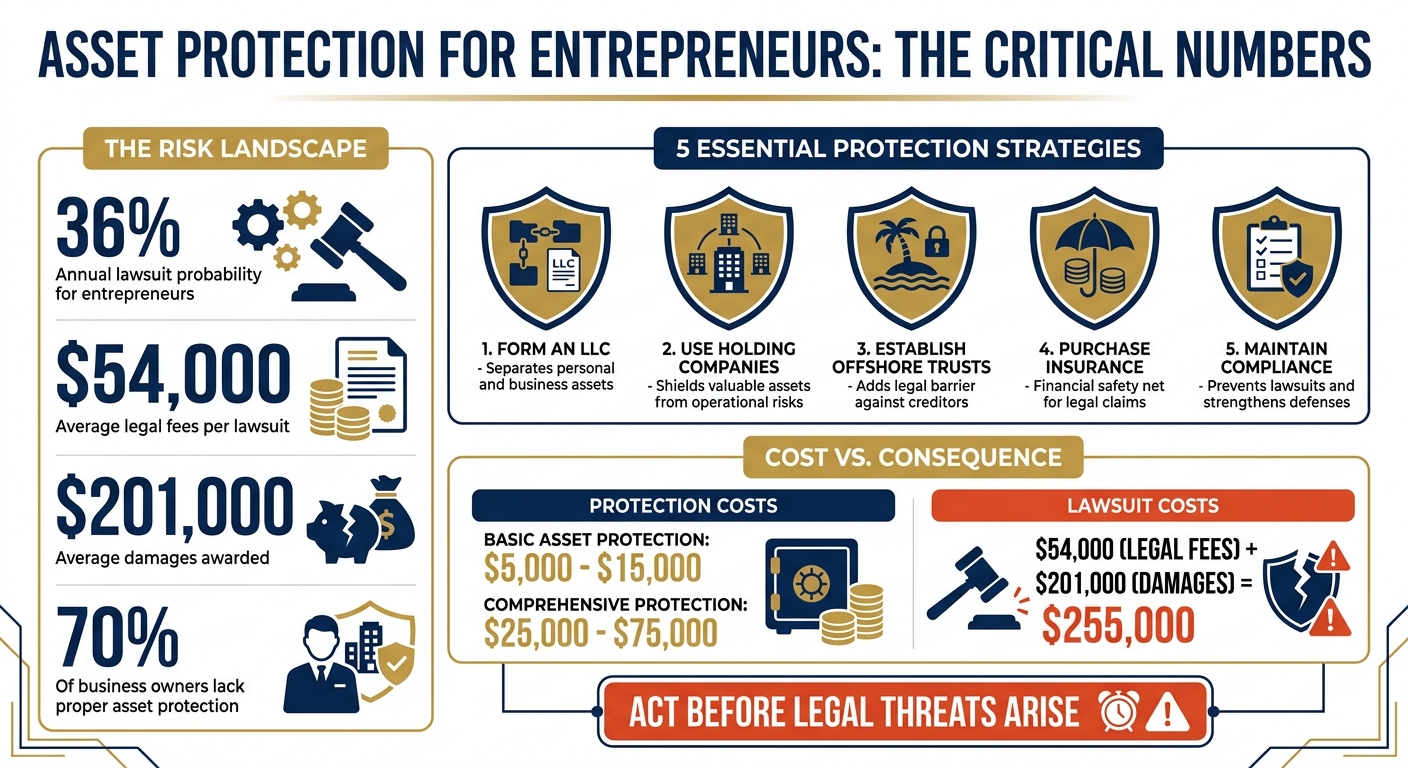

Entrepreneurs face a 36% chance of being sued annually, and lawsuits can cost an average of $54,000 in legal fees and $201,000 in damages. Despite the risks, 70% of business owners lack proper asset protection, leaving personal savings, homes, and retirement funds exposed.

Key strategies to protect your wealth include:

- Forming an LLC: Separates personal and business assets.

- Using Holding Companies: Shields valuable assets from operational risks.

- Establishing Offshore Trusts: Adds a legal barrier to protect assets from U.S. creditors.

- Purchasing Insurance: Acts as a financial safety net for legal claims.

- Maintaining Compliance and Contracts: Prevents lawsuits and strengthens your defenses.

Timing is critical – these measures must be in place before legal threats arise. Acting early can deter lawsuits and safeguard your hard-earned wealth.

Step 1: Set Up a US LLC to Separate Personal and Business Assets

An LLC (Limited Liability Company) acts as its own legal entity, capable of signing contracts, owning property, and taking on liabilities. This setup creates a legal boundary between your personal and business assets, shielding your personal wealth from potential business risks.

Why an LLC Is Ideal for Asset Protection

LLCs provide two main layers of protection. First, if your business encounters legal trouble or debt, creditors can only go after the company’s assets – this is called inside-out protection. On the flip side, if you’re personally sued, a charging order typically prevents creditors from seizing your business assets – this is known as outside-in protection.

Beyond protection, LLCs are popular for their tax advantages. Profits and losses pass directly to your personal tax return, simplifying the tax process. This combination of liability protection and tax efficiency makes LLCs a favorite among entrepreneurs.

However, for this protection to hold up, you must treat your LLC like a legitimate business. Use separate bank accounts and credit cards for business transactions, and always sign contracts in the LLC’s name. Proper funding is also key – if your LLC is underfunded, courts might disregard its legal separation and hold you personally liable.

"The corporate veil is your strongest defense, but it’s only as strong as your daily financial habits. Treating your business entity as a separate legal person is not optional – it’s the entire basis of its protective power."

– Commons Capital

Picking the Right State for Your LLC

For most small businesses (roughly 95%), forming an LLC in the state where you operate is the simplest and most practical choice. For example, if your business has an office, employees, or inventory in California, it’s logical to establish the LLC there. Trying to save money by registering in a state like Wyoming while operating in California may backfire – you’ll likely need to register as a "foreign LLC" in California, doubling your filing fees, annual reports, and other costs.

That said, some states offer specific benefits depending on your business needs:

- Wyoming: Known for strong privacy protections and affordable fees ($60 annually), it’s a great choice for online businesses or holding companies.

- Delaware: Though it costs about $300 per year, Delaware is a top pick for startups seeking venture capital, thanks to its specialized Court of Chancery for business disputes.

- Nevada: With an annual cost of $350 or more, Nevada offers no state income tax and strong privacy protections.

- New Mexico: After a $50 filing fee, New Mexico requires no annual reports or recurring fees, making it appealing for passive holding companies.

| State | Annual Cost | Best For |

|---|---|---|

| Wyoming | $60 | Online businesses, holding companies, privacy |

| Delaware | $300 | Startups seeking venture capital |

| Nevada | $350+ | High-risk businesses prioritizing anonymity |

| New Mexico | $0 | Passive holdings on a tight budget |

If you’re running an online business without a physical location or setting up a holding company, Wyoming or New Mexico might be the ideal choice. For startups planning to attract investors, Delaware’s legal system offers added advantages. On the other hand, if your business has a physical presence, forming your LLC in your home state is usually the easiest and most cost-effective approach.

Setting up your LLC correctly is the first step toward building a solid foundation for protecting your assets.

sbb-itb-39d39a6

Step 2: Create Multiple Layers of Protection with Holding and Operating Companies

Once your LLC is up and running, the next step is to separate what you own from what you do. This involves setting up two separate entities: a holding company to safeguard your valuable assets and an operating company to handle day-to-day business activities. This structure helps shield your high-value assets from potential business risks. Let’s break down how this works.

How Holding Companies Protect Your Assets

A holding company’s sole purpose is to own assets – things like intellectual property, real estate, or equipment – while staying out of the operational side of your business. Meanwhile, the operating company takes on the daily tasks and risks of running the business. For example, your holding company might own a trademark and license it to your operating company in exchange for a fee. If the operating company gets sued, creditors can only go after that company’s assets, leaving the holding company’s valuable assets untouched.

As Molly Miller, Manager of Customer Service at BizFilings, explains: "The operating entity conducts all business activities and, thus, bears all the risk of loss. The owner’s limited liability for business debts turns out to be no liability at all, because the operating entity contains little or no vulnerable assets."

A real-world example of this strategy comes from Google’s 2015 restructuring into Alphabet Inc., a Delaware-based holding company. Google LLC became a subsidiary focused on its internet products, while high-risk ventures like Waymo (self-driving cars) and Verily (life sciences) were spun off into separate subsidiaries. This setup limits liability between subsidiaries, ensuring that core assets are well-protected.

Why You Should Separate Holding and Operating Entities

By separating holding and operating entities, you create a protective "firewall" between your assets and liabilities. If your operating company faces a lawsuit, the holding company’s assets remain out of reach. This structure significantly reduces the risk of losing your most valuable holdings to legal claims. For instance, your operating company can pay rent or licensing fees to your holding company, systematically transferring cash from the riskier entity to the protected one.

To maintain this protection, it’s crucial to:

- Keep separate bank accounts for each entity.

- Maintain distinct records and document all inter-company transactions.

- Formalize agreements like leases or licenses in writing and at market rates.

- Avoid mixing personal and business funds.

- Preserve each company’s unique identity to prevent courts from "piercing the corporate veil" and exposing your protected assets.

| Entity Type | Primary Function | Asset Exposure |

|---|---|---|

| Operating Company (OpCo) | Handles daily operations, sales, hiring, and contracting | High (exposed to creditors and lawsuits) |

| Holding Company (HoldCo) | Owns equity, IP, real estate, and oversees subsidiaries | Low (avoids risky operations) |

| IP Holding Entity | Manages patents, trademarks, and copyrights | Minimal (shielded from operational risks) |

This layered approach is a powerful way to safeguard your assets.

As Q. R. Mackey, Author of Corporate Defense Strategies, notes: "If everything – your operations, your IP, your assets – is under one LLC, then one lawsuit can take it all. You think you’re protected. You’re not. You’re just organized."

Step 3: Use Offshore Trusts and Companies for Added Protection

Once your domestic asset protection structures are in place, adding an offshore element can significantly strengthen your overall plan. Offshore trusts and companies operate under foreign legal systems that don’t automatically recognize U.S. court orders. This creates a legal barrier, making it much harder – and more expensive – for creditors to access your wealth.

How Offshore Trusts Protect Your Wealth

Offshore trusts work by transferring your assets to an independent trustee in jurisdictions like the Cook Islands or Nevis. These locations have stringent legal protections, requiring creditors to present their claims in local courts under stricter standards. For instance, creditors must prove fraudulent transfers beyond a reasonable doubt, a much higher burden than in U.S. courts.

Take the Cook Islands, for example. Under the International Trusts Act, no properly structured trust (created before any claims arose) has been successfully breached by a U.S. creditor in over 40 years. Creditors are also required to post a litigation bond – ranging from $25,000 to $100,000 – and face a short statute of limitations for challenging transfers, generally one to two years.

As Brian T. Bradley, Esq., Asset Protection Attorney, explains: "If a creditor cannot collect, the structure worked. If they can, the paperwork never mattered."

A well-known case demonstrating this is FTC v. Affordable Media, LLC (The Anderson Case) in 1999. Even though the defendants faced contempt charges and incarceration, the Cook Islands trustee refused to comply with U.S. orders to repatriate the trust’s assets, effectively shielding them.

Timing is critical. The trust must be established and assets transferred before any legal threats arise. Transfers made after a claim can be voided as fraudulent. Additionally, you must relinquish control to an independent foreign trustee – retaining practical control undermines the protection.

| Jurisdiction | Statute of Limitations | Foreign Judgments | Burden of Proof | Bond Required |

|---|---|---|---|---|

| Cook Islands | 2 years | Not recognized | Beyond reasonable doubt | $50,000 |

| Nevis | 2 years | Not recognized | Beyond reasonable doubt | $25,000 |

| Belize | 3 years | Not recognized | Clear and convincing standard | None |

A common strategy involves layering an offshore trust with an offshore LLC. In this setup, the trust owns the LLC, providing an additional layer of protection, while you maintain managerial control over the LLC for day-to-day operations.

While offshore trusts protect asset ownership, offshore companies offer flexibility for global operations. These companies allow you to manage assets under foreign jurisdictions while maintaining privacy and operational efficiency.

Forming an Offshore Company in Anguilla

Adding an offshore company in Anguilla can further diversify your asset protection strategy. Anguilla’s legal framework supports both asset protection and operational flexibility. The Anguilla Business Company (ABC) stands out because it can operate both locally and internationally, unlike traditional International Business Companies, which are restricted to offshore activities.

The tax advantages are significant. Anguilla imposes no corporate, income, estate, capital gains, or business taxes on entities that don’t conduct business locally. This can also benefit eligible U.S. expatriates.

Privacy is another key benefit. The names of shareholders and directors are not part of public records, ensuring a high level of anonymity. Additionally, there are no currency restrictions, and both the U.S. dollar and the Eastern Caribbean Dollar are widely accepted.

Anguilla’s incorporation process is impressively fast. Thanks to its modern computerized registry, companies can often be set up within 24 hours. Only one shareholder and one director are required, and they can be the same person, regardless of nationality.

According to Anguilla-Beaches.com: "Anguilla has one of the most modern registries in the world, with a fully computerized database that is accessible on line by the local agents."

The costs for setting up an Anguilla company range from $2,000 to $5,000 initially, with annual fees between $1,000 and $3,000. Offshore trust formation is more expensive, typically costing $8,000 to $30,000. For instance, Cook Islands trusts usually cost $15,000 to $30,000, while Nevis trusts range from $10,000 to $25,000.

To incorporate in Anguilla, you’ll need a local agent licensed under the Company Management Ordinance. You’re also required to maintain proper accounting records at your registered office – failure to do so is a criminal offense. U.S. citizens and residents must report all global income to the IRS and comply with FATCA and FBAR requirements.

Step 4: Add Insurance Coverage as a Backup Layer

Even with LLCs, holding companies, and offshore structures in place, and understanding why offshore asset protection is effective, insurance is a critical safety net to protect your assets. It acts as a financial buffer, absorbing legal claims and managing everyday risks that could otherwise drain your resources. Insurance is the layer that helps prevent litigation from compromising the wealth you’ve worked so hard to build.

"Planning for protection is a multilayered process… But liability insurance is always the first line of defense" – Derek Thain, Vice President of Fidelity’s Advanced Planning team.

To strengthen your asset protection plan, consider these essential insurance policies.

Key Insurance Policies to Consider

- General Liability Insurance: Covers common risks like property damage or bodily injury on your business premises. For example, it can handle claims from slip-and-fall accidents.

- Professional Liability Insurance: Also known as Errors & Omissions insurance, this protects service-based businesses from claims related to professional mistakes, missed deadlines, or inadequate performance.

- Umbrella Liability Coverage: Extends coverage once your primary policies (like homeowners or auto insurance) hit their limits. For high-net-worth individuals, securing $5 million to $10 million in umbrella coverage typically costs between $3,000 and $8,000 annually. This extra layer can serve as a deterrent to frivolous lawsuits.

- Directors and Officers (D&O) Insurance: Protects personal assets from costs tied to regulatory investigations, shareholder disputes, or employment-related claims.

- Employment Practices Liability Insurance (EPLI): Covers claims involving wrongful termination, harassment, or discrimination.

- Product Liability Insurance: Essential for businesses that manufacture or sell physical products, this defends against claims of defects or safety concerns.

These policies, combined with your business structures and offshore strategies, create a comprehensive asset protection plan for the entrepreneur.

Choosing the Right Insurance Coverage

The amount of liability coverage you carry should at least match your net worth. For example, if your assets are worth $5 million, aim for a minimum of $5 million in coverage to protect your personal finances. But don’t stop there – evaluate your actual exposure. Businesses serving high-profile clients, like those in the Fortune 500, often face greater risks than those serving smaller companies.

It’s also important to ensure your policies work together seamlessly. Umbrella insurance only works if your underlying policies – such as auto, home, or business insurance – meet specific minimum requirements. Make sure every property, entity, and vehicle you own is listed on the umbrella policy to avoid gaps in coverage.

Review exclusions carefully. Standard liability policies typically don’t cover intentional wrongdoing or certain high-risk activities. Also, remember that general liability insurance doesn’t cover professional malpractice. For professionals like doctors, lawyers, or accountants, specialized insurance is the first line of defense.

Timing is key – secure your coverage before any potential liability or claims arise. Once a threat is identified, it may be too late to obtain protection. Work with an independent insurance agent who can compare policies from multiple carriers and tailor coverage to your specific needs. Reassess your insurance annually or whenever significant changes occur, such as acquiring new property or starting a new business venture.

Step 5: Reduce Legal Risks with Proper Contracts and Compliance

Once your LLCs, holding companies, offshore trusts, and insurance are in place, the next critical layer of asset protection comes down to solid contracts and ongoing compliance. These elements act as the glue holding your entire strategy together, ensuring your structures can withstand legal challenges.

Here’s a sobering statistic: contract disputes make up about 60% of the 20 million civil cases filed annually in the U.S., with small businesses facing a median cost of $91,000 per case. The good news? Clear contracts and consistent legal upkeep can help you avoid becoming part of that statistic.

"A poorly written contract can become a loophole for disputes – while a well-crafted one can be a shield."

- SnoValley Chamber of Commerce

Without strong contracts and compliance practices, even the most elaborate asset protection setup can falter in court.

Writing Contracts That Minimize Legal Exposure

Well-drafted contracts can make all the difference in avoiding disputes. Legal experts recommend following the "Four C’s" for every agreement:

- Clarity: Use language that’s easy to understand.

- Certainty: Be precise in the terms and conditions.

- Consensus: Ensure both parties fully agree.

- Consciousness: Acknowledge the binding nature of the agreement.

Here’s what to include in your contracts to keep them airtight:

- Clearly identify all parties: Leave no doubt about who’s responsible for what.

- Define work scope and deliverables: Spell out deadlines, payment terms, and expectations to avoid misunderstandings.

- Specify payment details: Include schedules, accepted methods, and penalties for late payments. Vague terms often lead to disputes.

- Dispute resolution clauses: Require mediation or arbitration before filing lawsuits. This can save you thousands in legal fees.

- Termination terms: Clearly outline how and when the agreement can end.

For partnerships or subcontractor relationships, add:

- Indemnification clauses: Limit liability between parties.

- Limitation of liability provisions: Cap your financial exposure.

- Ownership terms for intellectual property: Specify who retains rights to created work.

Confidentiality clauses and NDAs are also essential for protecting sensitive information, such as trade secrets and proprietary processes. Poor contract management can erode contract value by an average of 8.6%, with human error causing 92% of mistakes.

"A $2,000 contract review can prevent a $91,000 lawsuit."

- Beancount.io

To streamline your operations, standardize key agreements like Sales Contracts, Service Agreements, Employment Agreements, and NDAs. While templates are useful, always have an attorney review contracts for high-value deals or unique situations. These well-structured agreements form the bedrock of your compliance efforts.

Maintaining Compliance with Laws and Regulations

Once your contracts are in place, maintaining compliance ensures your protections stay intact. Compliance isn’t a one-and-done task – it requires consistent attention to federal, state, and local regulations.

- Federal compliance: Stay on top of IRS tax filings, FATCA reporting, and FBAR requirements.

- State compliance: Manage franchise taxes, annual filings, and nexus rules if you operate in multiple states.

- Local compliance: Keep permits and licenses up to date.

One major area of risk is worker classification. Misclassifying employees as independent contractors can lead to penalties and back taxes. The IRS uses a three-factor test to determine classification: behavioral control (who directs the work), financial control (who provides tools and sets pay), and the nature of the relationship (including benefits and job permanence). In 2024, 37% of small businesses faced litigation over employee issues, often due to misclassification.

To stay ahead, review your contracts and employee policies annually. Update shareholder agreements whenever there are major changes, like new investors or mergers. Similarly, review your insurance policies to ensure coverage aligns with current asset values and business entities.

Corporate formalities are just as important. Even single-member LLCs should have written operating agreements to prove the business operates as a separate legal entity. Skipping these steps can leave your personal assets vulnerable.

Plan to allocate 1–3% of your annual revenue toward legal expenses. Preventive measures, like audits and contract reviews, are far cheaper than defending a lawsuit. Regularly update privacy policies to comply with evolving laws like the CCPA. Remember, entrepreneurs face a 36% chance of being sued each year, with the average lawsuit costing $54,000 in legal fees alone.

| Document Type | Review Frequency | Key Update Triggers |

|---|---|---|

| Standard Client Contracts | Annual | Changes in service scope, new liability laws |

| Employee Handbook | Annual | Minimum wage increases, new state leave laws |

| Shareholder Agreement | Event-driven | New investors, partner retirement, funding rounds |

| Privacy Policy | Periodic | Changes in data collection, new privacy regulations |

Treat compliance as an active process. Laws and regulations are constantly changing, and staying proactive protects both your business and personal assets. By combining strong contracts with diligent compliance, you create a system that shields your wealth from legal risks.

How Global Wealth Protection Can Help You Protect Your Assets

Now that you’re familiar with the five key steps to safeguarding your wealth – LLCs, holding companies, offshore trusts, insurance, and compliance – it’s clear that implementing these measures effectively requires expert guidance. That’s where Global Wealth Protection steps in, offering the expertise needed to build and maintain a strong asset protection framework.

Founded by Bobby Casey, a seasoned entrepreneur with over two decades of experience, Global Wealth Protection specializes in crafting custom solutions for entrepreneurs and investors. The firm has helped countless individuals cut their tax liabilities by 50–100% while shielding their wealth from legal risks.

"I’ve helped thousands of entrepreneurs protect their assets from frivolous litigation, cut their taxes by 50-100%, create structures for wealth perpetuation, and properly structure their company for simplicity and tax optimization."

- Bobby Casey, Founder, Global Wealth Protection

The firm’s primary focus is on privacy and asset protection. Whether you’re looking to establish a private US LLC, an offshore company in jurisdictions like Anguilla or Nevis, or a trust for high-net-worth planning, Global Wealth Protection provides tailored, full-service support to meet your needs.

Customized Asset Protection Strategies

Every entrepreneur faces unique risks. A real estate investor managing multiple properties, for example, has different vulnerabilities compared to a tech founder with valuable intellectual property. Global Wealth Protection begins by evaluating your risk profile and reviewing your assets to identify areas of exposure.

From this assessment, they create a multi-layered strategy tailored to your specific situation. For instance, a location-independent entrepreneur might benefit from combining a private US LLC with an offshore company in Anguilla for enhanced privacy. High-net-worth clients – those with $250,000 or more in assets – can explore additional options like offshore trusts or private interest foundations in Anguilla, which offer robust protection and estate planning benefits.

One advanced option involves setting up an offshore LLC owned by an offshore trust. Under normal circumstances, you remain the manager and bank signatory. However, if a lawsuit arises, the trustee can step in to safeguard the assets, ensuring they remain out of reach from creditors. This layered approach provides a strong defense against legal threats.

For those seeking ongoing guidance, the GWP Insiders Membership offers resources on internationalization strategies, jurisdiction selection, and tax minimization. This program ensures your strategies remain effective and up to date as laws and circumstances change.

Full Support from Setup to Ongoing Management

Creating protective structures is just the beginning; maintaining them over time is what ensures they hold up in legal situations. Global Wealth Protection offers end-to-end support, from initial setup to ongoing management, to keep your structures compliant and your corporate veil intact.

"Our plans combine services across legal, accounting, and financial disciplines to deliver a comprehensive wealth preservation strategy."

- Global Wealth Protection LLC

The firm handles all the details, including filings, annual reports, document certifications, registered agent services, and even introductions to offshore banking partners. This comprehensive approach helps avoid the common mistake of neglecting maintenance, which can lead to courts piercing your corporate veil [1,34].

For those ready to take action, Global Wealth Protection offers consultations that provide clear roadmaps for tax reduction and wealth preservation. Whether you’re just starting to explore asset protection or are ready to dive into advanced offshore strategies, the firm integrates legal, accounting, and financial expertise to ensure your plan operates seamlessly. The result? Confidence and peace of mind that your assets are secure.

Conclusion

Protecting your assets isn’t something to put off for another day. The numbers paint a stark picture: entrepreneurs face a 36% chance of being sued in any given year – five times the risk of the average American. And when lawsuits hit small businesses, the median damages can reach around $201,000.

The strategies covered in this guide – LLCs, holding companies, offshore trusts, insurance, and compliance – are designed to work together, creating layers of protection that make lawsuits both legally challenging and financially unappealing. This approach often deters frivolous claims before they even start. But timing is everything. These safeguards need to be in place before any legal threats arise. Once litigation begins, your options narrow, and last-minute asset transfers can be undone.

Despite the risks, 70% of successful entrepreneurs still leave their wealth vulnerable. Don’t let yourself fall into that group. Whether you’re just starting out or managing substantial assets, the best time to act is now – when no threats are looming, and you can strategically plan without pressure.

A proactive protection plan isn’t just about shielding your wealth. It also strengthens your ability to negotiate and keeps your focus on growing your business. With expert help, creating such a plan is straightforward. The cost – ranging from $5,000 to $15,000 for basic strategies or $25,000 to $75,000 for more comprehensive plans – pales in comparison to the average $54,000 in legal fees for a single lawsuit. In short, investing in asset protection now can save you from financial and emotional turmoil later.

Don’t wait. Evaluate your risks, take stock of your assets, and start building a solid defense for your hard-earned wealth. Planning today ensures that what you’ve worked so hard to achieve remains secure tomorrow.

FAQs

When is it too late to set up asset protection?

It’s important to understand that once a lawsuit is filed or legal action is on the horizon, the opportunity to put effective asset protection measures in place has likely passed. The best time to implement these strategies is well in advance, long before any potential legal issues surface. Proactive planning is the key to safeguarding your assets.

How do I avoid “piercing the corporate veil” with my LLCs?

To protect yourself from "piercing the corporate veil", it’s crucial to keep your personal finances and your LLC’s business dealings completely separate. Start by using dedicated bank accounts for your LLC and ensure that all transactions are properly documented. Maintain accurate and thorough records to show clear distinctions between personal and business activities.

Additionally, make sure your LLC has enough funds to meet its obligations and always operate with integrity in all business dealings. These steps help create a clear line between you and your LLC, which can reduce the chances of being held personally responsible for business debts.

Do offshore trusts require me to report anything to the IRS?

Yes, offshore trusts must be reported to the IRS. This involves filing Form 3520, which is used to disclose details about transactions with foreign trusts and any ownership interests in them.

Compliance with U.S. tax laws and reporting requirements isn’t optional – it’s mandatory. Failing to submit the required forms can lead to serious penalties. If you’re involved with a foreign trust, make sure to stay on top of these obligations to avoid unnecessary complications.