In 2026, offshore asset protection is no longer about secrecy – it’s about creating legally sound and transparent structures that meet strict global compliance standards. With over 120 jurisdictions adhering to the Common Reporting Standard (CRS) and upgraded FATCA agreements, tax authorities now have unprecedented access to financial data. Non-compliance risks include hefty penalties, legal challenges, and even criminal charges.

Key takeaways:

- Transparency is critical: Offshore secrecy is obsolete; accurate reporting is mandatory.

- Main tools: Offshore trusts, private interest foundations, and international LLCs are essential for protecting assets, but they must be professionally managed with proper documentation.

- Jurisdiction matters: The Cook Islands, Nevis, and Belize offer strong creditor protections, while U.S. states like Nevada and South Dakota provide domestic options with privacy and legal safeguards.

- Compliance is ongoing: Regular monitoring, due diligence, and updates are necessary to ensure structures remain effective under evolving regulations.

Main International Asset Protection Structures

In 2026, the three main tools for international asset protection are offshore trusts, private interest foundations, and international LLCs. Each serves a specific role in safeguarding assets. However, these structures require professional oversight, detailed documentation, and trustees who genuinely exercise discretion rather than simply following instructions. To meet modern regulatory demands, these structures must establish true independence from the start. Let’s take a closer look at how offshore trusts lead the way in creating strong, compliant asset protection frameworks.

Offshore Trusts: Legal Safeguards and Tax Compliance

Offshore trusts remain a cornerstone of global asset protection strategies. Their strength lies in the legal barriers they create rather than relying on secrecy. For example, jurisdictions like the Cook Islands and Nevis present significant challenges for creditors. U.S. court judgments are not recognized locally, meaning creditors must re-litigate cases under local laws. Additionally, they are required to post a $100,000 litigation bond and meet a high standard of proof for fraudulent transfers.

These trusts are especially valuable for pre-immigration planning, managing assets across family members in different jurisdictions, and avoiding forced heirship laws that dictate inheritance in some civil law countries. However, with the Common Reporting Standard in place, tax authorities in your home country will typically learn about the trust within 12 to 18 months. This makes accurate tax reporting from the very beginning absolutely critical, reinforcing the compliance-first mindset emphasized earlier.

A major pitfall to avoid is retaining excessive control over the trust. As Ipanema Partners explains:

"A trust that provides meaningful protection requires meaningful independence: a professional trustee exercising genuine discretion, a trust protector with defined (not unlimited) powers, and distribution standards that are truly discretionary rather than a rubber stamp."

If you retain powers like revoking the trust, directing investments, or replacing trustees at will, courts may view the trust as a sham, leaving assets vulnerable to creditors.

Private Interest Foundations: Long-Term Wealth Planning

Private interest foundations, while different from trusts, offer a flexible approach to managing wealth over the long term. These entities function as separate legal structures with governance provided by foundation councils. Unlike trusts, which may not be legally recognized in some civil law jurisdictions, foundations are widely accepted and provide perpetual existence – making them ideal for multi-generational succession planning.

Anguilla has become a popular jurisdiction for these foundations due to its strong asset protection laws and compliance with anti–money laundering regulations. Foundations are especially useful when operational flexibility is needed, as they can directly own businesses, manage real estate, and oversee investment portfolios. The foundation council operates similarly to a corporate board, ensuring the structural separation necessary to meet legal requirements.

For U.S. taxpayers, foundations are subject to the same transparency and reporting rules as trusts, including the grantor trust provisions under Internal Revenue Code sections 671–679. While they don’t offer income tax deferral, they do provide strong creditor protection and effective succession planning when properly structured.

International LLCs and Corporations: Asset Diversification

International LLCs add another layer of protection by diversifying asset ownership. These entities offer two levels of security: they shield personal assets from business liabilities (horizontal protection) and protect LLC membership interests from personal creditors (vertical protection). In Nevis, for instance, charging orders against LLC membership interests expire after three years and cannot be renewed, making them an appealing option for asset protection.

A common tactic in 2026 is the bridge structure, where a Nevis LLC holds operating assets or investments, and its membership interest is owned by a Nevis or Cook Islands trust. This layered setup forces creditors to navigate both the LLC and the trust, creating additional hurdles.

Compliance with Ultimate Beneficial Ownership (UBO) rules is now mandatory. Financial institutions and corporate registries require full disclosure of the individuals who ultimately control or own an entity. This information is also reported to tax authorities under the Common Reporting Standard. As a result, these structures must be defensible based on their legitimate purpose, supported by accurate documentation, and managed independently to meet regulatory scrutiny.

sbb-itb-39d39a6

Jurisdiction Comparison for Asset Protection

Choosing the right jurisdiction for asset protection means evaluating how courts handle creditor claims and ensuring the legal framework is up to the task. A jurisdiction’s effectiveness hinges on its judicial independence, evidentiary standards, and regulatory consistency. In 2026, jurisdictions must also meet evolving compliance standards to withstand legal and regulatory scrutiny.

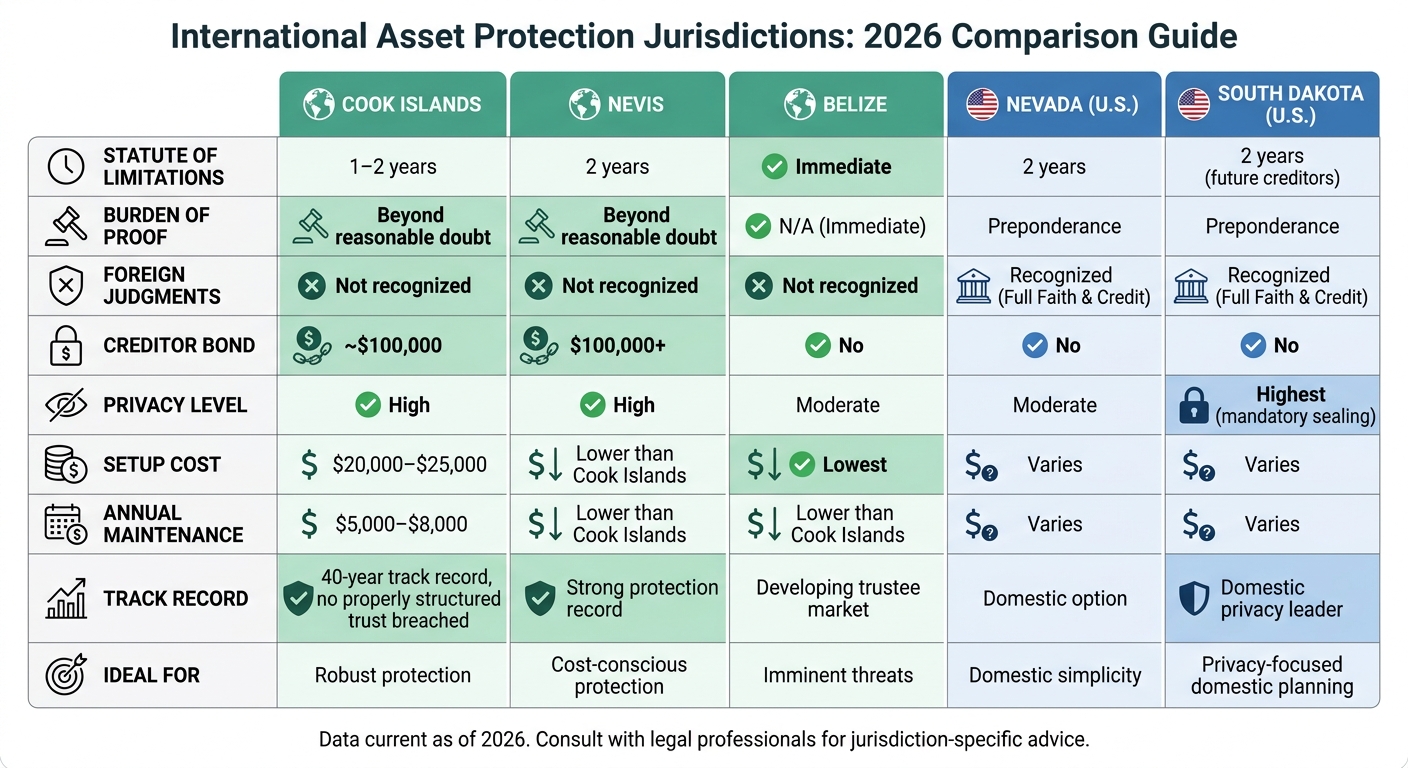

The Cook Islands stand out as a top-tier option. Over a 40-year track record, no properly structured trust has been breached by a U.S. creditor. Creditors face stringent hurdles, including a criminal-level burden of proof, while U.S. court judgments are outright rejected. Nevis offers comparable protections, adding an extra layer of deterrence with a $100,000 litigation bond required before creditors can initiate a case. Meanwhile, Belize provides instant asset protection upon funding by overriding the Statute of Elizabeth, although its trustee market is less developed.

For domestic solutions, Nevada leads with a two-year statute of limitations and no exceptions for claims like alimony or child support, treating all creditors equally. South Dakota, on the other hand, offers unmatched privacy with laws requiring automatic and perpetual sealing of trust litigation records. Despite these strengths, domestic trusts face vulnerabilities under the Full Faith and Credit Clause, making them unable to dismiss judgments from other states – something offshore jurisdictions can avoid.

Regulatory standing also plays a vital role, particularly with shifts in compliance lists like those maintained by the Financial Action Task Force (FATF). Jurisdictions on the FATF grey list face increased scrutiny from banks, which can complicate financial operations. In June 2025, for instance, Monaco and the Virgin Islands (UK) were added to the grey list, while Panama and the UAE were removed after improving their anti-money laundering measures. Staying informed about these changes is crucial – being tied to a flagged jurisdiction can lead to financial institutions taking de-risking measures.

Jurisdiction Comparison Table

| Feature | Cook Islands | Nevis | Belize | Nevada (U.S.) | South Dakota (U.S.) |

|---|---|---|---|---|---|

| Statute of Limitations | 1–2 years | 2 years | Immediate | 2 years | 2 years (future creditors) |

| Burden of Proof | Beyond reasonable doubt | Beyond reasonable doubt | N/A (Immediate) | Preponderance | Preponderance |

| Foreign Judgments | Not recognized | Not recognized | Not recognized | Recognized (Full Faith & Credit) | Recognized (Full Faith & Credit) |

| Creditor Bond | ~$100,000 | $100,000+ | No | No | No |

| Privacy Level | High | High | Moderate | Moderate | Highest (mandatory sealing) |

| Setup Cost | $20,000–$25,000 | Lower than Cook Islands | Lowest | Varies | Varies |

| Annual Maintenance | $5,000–$8,000 | Lower than Cook Islands | Lower than Cook Islands | Varies | Varies |

| Ideal For | Robust protection | Cost-conscious protection | Imminent threats | Domestic simplicity | Privacy-focused domestic planning |

Building and Maintaining Compliant Asset Structures

Creating a strong asset protection framework in 2026 is about more than just picking the right jurisdiction. It requires a design that can handle regulatory scrutiny while staying flexible enough for operational needs. Every aspect – from ownership to tax reporting – must work seamlessly across jurisdictions.

Layered Structures for Enhanced Protection

The most effective asset structures spread protection across three areas: legal, financial, and personal compliance. This approach minimizes risks by avoiding single points of failure.

A practical way to achieve this is by dividing business functions into separate entities. For instance, one entity might own the assets, another could manage daily operations, and a third might handle expenses. This modular setup ensures that legal issues in one area don’t jeopardize the entire structure.

The "Financial Cascade" is a good example of this layered strategy. Here’s how it works:

- Keep 10% of liquidity in fintech accounts for operational needs.

- Place 70% in Tier-1 banks located in neutral jurisdictions.

- Allocate 20% to alternatives like stablecoins for emergencies.

This distribution helps maintain access to funds even if sudden banking restrictions arise. For maximum security, consider combining an offshore trust with an offshore LLC that holds a bank account outside the U.S.. This setup can make it harder for courts to enforce repatriation orders, relying on what’s known as the "impossibility defense".

"An offshore account alone does not fully protect assets from creditors. A U.S. court can order the account holder to repatriate the money… Full protection requires pairing the account with an offshore trust." – Alper Law

However, even the best structure won’t hold up without diligent compliance and ongoing oversight.

Conducting Thorough Due Diligence

Due diligence starts with ensuring that your chosen jurisdiction and service providers meet standards of genuine economic activity. This includes establishing a real physical presence, such as an office with local staff. Regulators are increasingly looking for proof that entities are operational and not just shell companies.

Carefully vet service providers. Offshore banks, for example, should have no ties to the U.S., such as branches, subsidiaries, or FDIC insurance. Any U.S. presence could expose your assets to domestic legal actions. For trustees and directors, work with reputable providers known for their regulatory track records and transparent fees.

Documentation is another critical piece. Keep detailed records of every asset transfer, including the business purpose and timing, to defend against claims of fraudulent conveyance. Courts can void suspicious transfers, so having proper documentation is essential.

Tax reporting must also align perfectly. With over 1.5 million Americans holding foreign accounts and more than 110 countries participating in FATCA reporting, discrepancies can trigger audits or penalties. U.S. taxpayers must comply with FBAR and Form 8938 requirements, and professional fees for these filings typically range from $3,000 to $5,500 annually.

Ongoing Monitoring and Compliance Updates

Once your structure is in place, regular monitoring is crucial to keep pace with changing regulations. A static structure can quickly become a liability. As Sveta Zheremiash, Corporate Architect at FORMA FLAGA, notes:

"International structures that have not been reviewed in the past two to three years may be generating risk precisely where their owners expect protection".

Regulations evolve quickly, and what worked in 2024 may not hold up in 2026. Annual reviews should cover several areas. First, ensure your tax residency is properly documented. Under OECD standards, simply having a passport stamp isn’t enough – you need to spend more than 183 days per year in the new jurisdiction. Second, keep an eye on family mobility, as relocations for work or education can unintentionally change your tax status.

New regulatory changes also require attention. For instance, the Crypto-Asset Reporting Framework (CARF), set to begin in 2027, will tighten rules on digital asset transparency. Similarly, stricter beneficial ownership reporting standards mean all documentation must be consistent across entities.

Banking relationships should also be reviewed regularly. Offshore bank fees typically fall between $500 and $2,500 annually, with wire transfer fees ranging from $25 to $75. Banks periodically reassess client relationships, so keeping your economic substance documentation up to date is essential for maintaining compliance.

The ideal time for planning is 12 to 24 months before major life events like a relocation, business sale, or inheritance. Adjustments made after the fact can be costly. Regular monitoring helps you stay ahead, preserving flexibility and minimizing risks.

Conclusion

The days of offshore secrecy are long gone. By 2026, effective asset protection hinges on creating transparent, compliant structures that can withstand rigorous regulatory scrutiny. With over 110 countries and more than 300,000 institutions reporting U.S. account information under FATCA, and increasing regulations surrounding digital assets, the push for transparency is stronger than ever.

"Wealth preservation is not about secrecy. It is about intelligent, transparent structure." – PCC Wealth

This shift from secrecy to compliance isn’t just a change in mindset – it’s a practical necessity. Tax compliance plays a critical role in asset protection by eliminating vulnerabilities that could be exploited by creditors or government agencies. A well-structured offshore framework, built on jurisdictional separation and a sound legal foundation, offers far greater resilience than any attempt to obscure assets.

Planning ahead is key. Asset protection strategies should be mapped out 12 to 24 months before significant life or financial changes. If your structures haven’t been reviewed in the past two to three years, they could be creating risks instead of mitigating them. Regular stress testing, coordinated professional advice, and meticulous documentation are vital to maintaining a robust asset protection plan.

In today’s regulatory landscape, compliance isn’t just a box to check – it’s the foundation of enduring asset protection. The structures that stand the test of time are those built with transparency, economic substance, and enforceable legal frameworks at their core. Beyond safeguarding your assets, these compliant strategies ensure your legacy remains secure for future generations.

FAQs

How do I stay compliant with CRS and FATCA when using offshore structures?

To meet the requirements of CRS and FATCA, it’s essential to follow their rules for reporting and transparency. This means fully disclosing all offshore accounts and assets to the relevant tax authorities. Ensure you keep thorough documentation and submit accurate reports on time. Partnering with experienced tax advisors can help you navigate these regulations, meet deadlines, and avoid errors. Non-compliance can result in penalties, so it’s crucial to ensure your offshore arrangements comply with these standards in 2026.

What level of control can I keep without weakening an offshore trust or foundation?

You can retain considerable control over an offshore trust or foundation by taking actions like appointing or removing trustees, directing investment decisions, and defining beneficiaries. However, for this control to work without jeopardizing the trust’s structure, it’s crucial to design these controls in a way that aligns with legal and regulatory standards while maintaining the effectiveness of the asset protection strategy.

When should I set up an asset protection structure to avoid fraudulent transfer issues?

Establishing an asset protection structure ahead of time – before any creditor claims or legal disputes emerge – is crucial. Once a claim is threatened or filed, any transfers you make could be examined for fraud if they seem designed to block creditors. By planning proactively, you can stay within legal boundaries and minimize potential risks.