Think your domestic LLC is protecting your assets? It might not be. Many business owners believe forming an LLC in states like Wyoming or Nevada guarantees strong asset protection. However, the reality is often different. Here’s why:

- State Laws Matter: Asset protection is governed by the laws of the state where you live or operate, not where your LLC is formed. For example, California courts will apply California law, even if your LLC is based in Wyoming.

- Single-Member LLCs Are Vulnerable: Courts have repeatedly allowed creditors to seize assets from single-member LLCs, as seen in cases like Olmstead v. FTC.

- Charging Orders Aren’t Foolproof: In some states, creditors can foreclose on LLC interests if charging orders don’t satisfy debts. This is especially true in states like California, Florida, and New Hampshire.

- Bankruptcy Risks: Federal courts often bypass state protections, allowing trustees to liquidate LLC assets in bankruptcy cases.

If you’re serious about protecting your assets, domestic LLCs often fall short. Offshore structures, like those in the Cook Islands or Nevis, offer stronger safeguards by operating outside U.S. jurisdiction. These jurisdictions impose higher legal hurdles for creditors, such as requiring expensive litigation bonds and proving claims beyond a reasonable doubt.

Key takeaway: Domestic LLCs, especially single-member ones, are not a reliable shield against creditors. To protect your wealth, consider offshore asset protection that provide better legal barriers.

How Charging Orders Work in Domestic LLCs

The Legal Mechanics of Charging Orders

When a creditor wins a judgment against you, they can request a charging order on your LLC interest. This court-authorized lien requires the LLC manager to redirect any distributions meant for you directly to the creditor. However, the creditor doesn’t gain management rights or access to the LLC’s records. There’s another catch: under Revenue Ruling 77-137, you’re still responsible for reporting and paying taxes on the LLC’s pass-through income – even if the money goes straight to the creditor. This means you could end up paying taxes on income you don’t actually receive.

Where Domestic Law Falls Short

One major flaw in domestic LLC protection is that courts often apply the state law where the case is heard, rather than the law of the state where the LLC was formed. This can undermine protections that were intended to be exclusive. For example, in March 2026, the U.S. District Court for the Eastern District of California ruled in United States v. Huckaby that California law governs creditor claims against real property located in California. This meant a foreign LLC was subjected to California’s stricter enforcement rules, regardless of its home state’s protections.

"A Wyoming LLC holding a California rental property, owned by a California resident, being sued in a California court provides Wyoming-level protection in Wyoming court filings and California-level protection everywhere that actually matters." – Brian T. Bradley, Esq., National Asset Protection Attorney

In about one-third of U.S. states, if a charging order doesn’t satisfy the debt, courts can take more aggressive measures, such as foreclosing on your LLC membership interest. A notable example is the 2013 South Carolina Supreme Court case, Kriti Ripley, LLC v. Emerald Investments, LLC, where a creditor was allowed to foreclose on a 70% membership interest because future distributions wouldn’t realistically cover the debt. States like Texas and New York take similar approaches. In April 2025, the Fourteenth Court of Appeals in Texas ruled in WC 4th and Colorado, L.P. v. Colorado Third Street, LLC that a receiver could take control of an LLC’s litigation and assets, bypassing Texas’s supposed "exclusive remedy" provision.

These gaps in protection illustrate why domestic LLCs – especially single-member LLCs – often fall short in shielding assets.

Single-Member vs. Multi-Member LLCs: Protection Differences

The level of protection provided by an LLC depends heavily on its structure. Multi-member LLCs offer stronger protections because charging orders are designed to protect other members from being dragged into a creditor’s claim. Single-member LLCs, on the other hand, lack this dynamic. Without additional members, courts often allow creditors to seize the entire membership interest.

A landmark case highlighting this vulnerability is the Florida Supreme Court’s 2010 decision in Olmstead v. FTC. The court ruled that charging orders are not the sole remedy for single-member LLCs, allowing the FTC to seize the entire membership interest to satisfy a judgment. Florida later codified this approach in Section 605.0503(11), explicitly permitting foreclosure of single-member LLC interests when distributions fall short.

The table below shows how different states handle these situations:

| State | SMLLC Protection | Creditor Remedy |

|---|---|---|

| Wyoming | High | Charging order is the exclusive remedy |

| Delaware | High | Charging order is the exclusive remedy; no foreclosure allowed |

| Florida | Low | Entire membership interest can be foreclosed |

| New Hampshire | Low | Broader remedies beyond charging orders permitted |

| Colorado | Low | Charging orders are not exclusive; other remedies allowed |

Federal bankruptcy courts add another layer of risk. In April 2003, the U.S. Bankruptcy Court for the District of Colorado ruled in In re Albright that when the sole member of an LLC files for Chapter 7 bankruptcy, the trustee can step in as a member. This allows the trustee to manage and liquidate the LLC’s assets. These federal rulings further expose the weaknesses of domestic LLC protections, making offshore options worth considering in certain scenarios. This often involves structuring offshore trusts to create a more robust legal barrier.

sbb-itb-39d39a6

Court Cases Where Domestic LLC Protection Failed

Cases Where Courts Pierced LLC Protections

Several court rulings show how protections offered by domestic LLCs can fail under certain circumstances. For instance, in June 2010, the Florida Supreme Court decided in Olmstead v. FTC that the Federal Trade Commission could seize all "right, title, and interest" in Shaun Olmstead and Julie Connell’s single-member LLCs. This was to satisfy a $10 million judgment tied to an advance fee credit card scam. The court determined that Florida’s LLC Act did not explicitly limit creditor remedies to charging orders, allowing for broader actions like levy and sale.

"The statutory charging order provision does not preclude application of the creditor’s remedy of execution on an interest in a single-member LLC." – Justice Canady, Florida Supreme Court

In another case, Earthgrains Baking Co. v. Sycamore, decided in March 2022, the 10th Circuit Court of Appeals took a strict stance. Leland Sycamore’s Nevada LLC had refused to make distributions for four years after a charging order was issued. In response, the court appointed a receiver and ordered the liquidation of LLC assets to cover a $4,674,958 judgment and $1,091,336.40 in attorney’s fees. The court justified its actions by considering "actual and imputed distributions" made to other members.

Similarly, the California Court of Appeal allowed "outside reverse veil piercing" in Curci Investments, LLC v. Baldwin. In this case, real estate developer James Baldwin distributed nearly $180 million through his LLC over six years but halted distributions for five years after a $7.2 million judgment. The court found that Baldwin had used the LLC as a personal bank account to dodge creditor claims, effectively nullifying the protection offered by charging orders.

"Since the individual defendant… retained complete control to decide if and when LLC distributions would be made, the charging order was an illusory remedy." – Paul Porvaznik, Business Litigator

How Courts Often Side with Creditors

Courts have also demonstrated a willingness to extend creditor remedies by adopting creative legal approaches that challenge traditional LLC protections. In Sky Cable v. Coley, the Fourth Circuit applied a "reverse veil-piercing" doctrine to enforce a $2.3 million judgment against three Delaware LLCs controlled by one defendant. The court found that the defendant commingled funds, failed to maintain proper accounting records, and used LLC funds for personal expenses like taxes and mortgages.

"Piercing is not the type of remedy that the [charging statute] was designed to prohibit… piercing challenges the legitimacy of the LLC entity itself." – Fourth Circuit Court of Appeals

Another example is Devoll v. Demonbreun, decided by the Texas Court of Appeals in August 2016. In this case, creditor Rebecca Demonbreun was allowed to block the sale of real estate held within an LLC to satisfy a $114,000 judgment against Norris Devoll. The court bypassed Texas’s exclusive charging order remedy by permitting equitable remedies against the LLC’s underlying assets. Legal expert Jay Adkisson highlighted the broader implications of such rulings:

"So called charging order protection has been eviscerated in a way that most creditor rights’ attorneys could only have dreamed about." – Jay Adkisson, Legal Commentator

Why Offshore Structures Provide Better Asset Protection

Benefits of Offshore Jurisdictions

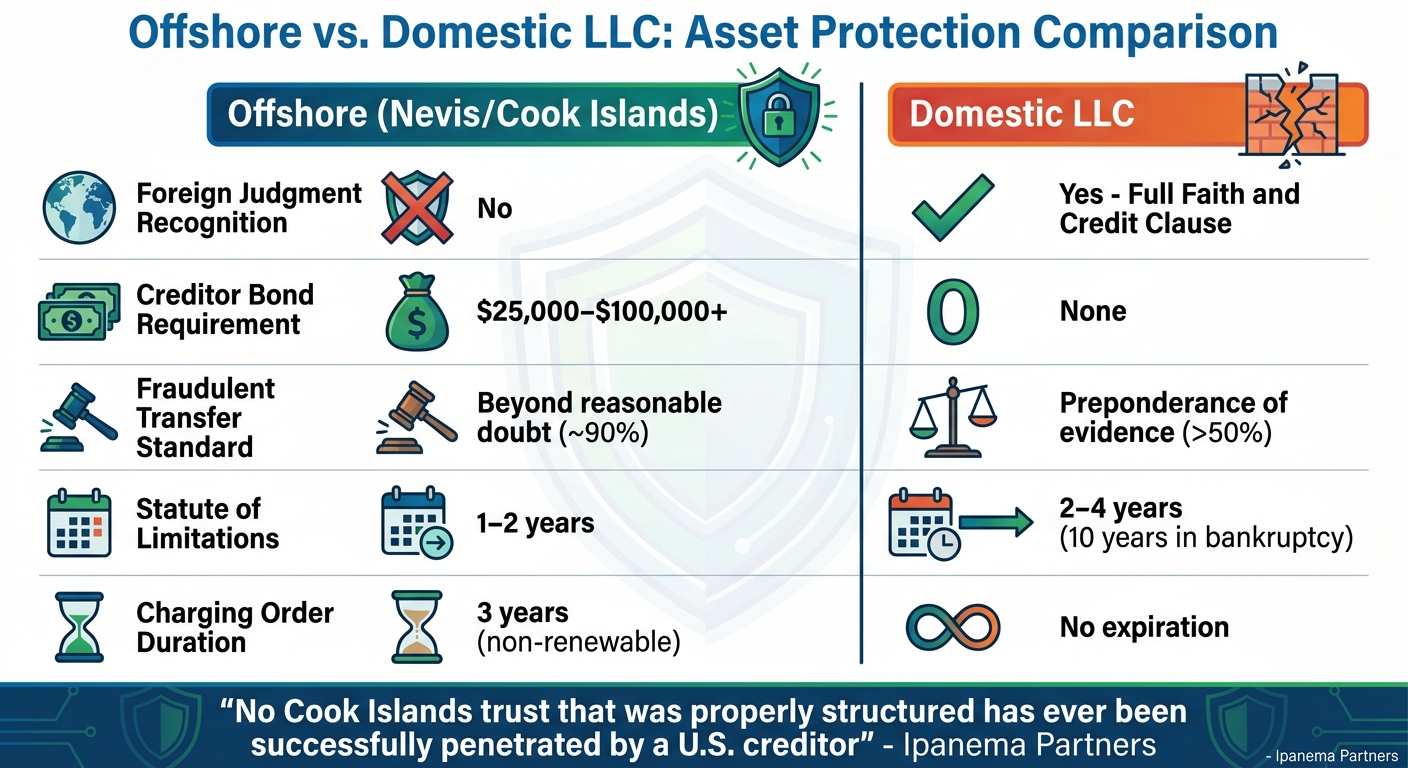

Offshore jurisdictions offer stronger safeguards against creditor claims compared to domestic LLCs. While domestic LLCs can be vulnerable under U.S. law – especially when creditors bypass charging order protections – offshore jurisdictions like Nevis and the Cook Islands operate outside the U.S. legal system. This independence means U.S. court judgments hold no weight in these countries. For instance, if a creditor secures a $10 million judgment in California, they cannot enforce it in Nevis. Instead, they must start a new lawsuit under local laws, effectively resetting the legal process. This creates substantial roadblocks for creditors.

The hurdles don’t stop there. Offshore jurisdictions impose strict procedural requirements. Creditors must post a litigation bond – ranging from $25,000 to $100,000 – just to file a case. If they lose, the bond is forfeited. Additionally, the burden of proof is much higher. Creditors must demonstrate fraudulent intent "beyond a reasonable doubt", a standard far tougher than the "preponderance of the evidence" threshold used in U.S. civil courts.

"The Cook Islands… track record speaks for itself: no Cook Islands trust that was properly structured, adequately funded, and established before a legal claim arose has ever been successfully penetrated by a U.S. creditor." – Ipanema Partners

Another advantage lies in the statute of limitations. In the U.S., bankruptcy law allows creditors to challenge fraudulent transfers to domestic trusts up to 10 years after the transfer. Offshore jurisdictions like Nevis and the Cook Islands, however, limit this window to just 1 to 2 years. Moreover, charging orders in Nevis expire after three years and cannot be renewed, unlike domestic charging orders, which can last indefinitely.

| Feature | Offshore (Nevis/Cook Islands) | Domestic LLC |

|---|---|---|

| Foreign Judgment Recognition | No | Yes (Full Faith and Credit Clause) |

| Creditor Bond Requirement | $25,000–$100,000+ | None |

| Fraudulent Transfer Standard | Beyond reasonable doubt (~90%) | Preponderance of evidence (>50%) |

| Statute of Limitations | 1–2 years | 2–4 years (10 years in bankruptcy) |

| Charging Order Duration | 3 years (non-renewable) | No expiration |

These features highlight why offshore jurisdictions are a preferred choice for those seeking stronger asset protection.

How Offshore LLCs and Trusts Work

The benefits of offshore jurisdictions are amplified when combined with offshore LLCs and trusts. An offshore LLC functions similarly to a domestic LLC but is shielded from U.S. legal interference. For example, a Nevis LLC provides charging order protection that expires after three years, requires creditors to post a litigation bond, and demands proof of fraud beyond a reasonable doubt – all within a two-year timeframe.

An offshore trust takes asset protection to the next level. Typically, the trust owns the LLC, and an independent foreign trustee controls distributions. This setup creates what’s called the "impossibility defense" – if a U.S. court orders asset repatriation, the account holder can legitimately claim they lack control because the trustee operates independently of U.S. jurisdiction.

"If you had the ability to bring those assets back at will, a judge could order you to bring them back. The clients need to be comfortable with the fact that the assets are there for their benefit, but they can’t control them." – Asher Rubinstein, Partner, Gallet Dreyer & Berkey, LLP

Offshore trusts often include "duress provisions" that automatically strip the settlor of any remaining powers if a U.S. court attempts to force asset repatriation. Some also feature "flight clauses", enabling the trustee to move the trust to a different jurisdiction if a creditor successfully files suit in the original location.

The Cook Islands, in particular, has a proven track record. Over the past 40 years, no properly established trust – funded before a legal claim arose – has been successfully breached by a U.S. creditor. This long-standing reliability makes offshore trusts and LLCs a robust option for safeguarding assets.

How to Set Up Offshore Asset Protection

Offshore asset protection strategies are designed to address the weaknesses of domestic LLCs, offering a more reliable way to safeguard assets. Global Wealth Protection provides tailored offshore solutions to help protect high-net-worth individuals from creditor claims.

Services from Global Wealth Protection

Global Wealth Protection focuses on creating offshore structures in jurisdictions like the Cook Islands, Nevis, and Belize – countries that don’t recognize U.S. court judgments. This means creditors must re-litigate any claims under the local laws of these jurisdictions, which can be a significant hurdle.

One of their key offerings is the Bridge Trust®, which operates as a domestic grantor trust under IRC §§671-677. This trust remains domestic until a legal threat arises. If an "Event of Duress" occurs, such as a court judgment or repatriation order, the trust automatically shifts its administration offshore to the Cook Islands. At that point, an independent foreign trustee takes control, and the impossibility defense can be invoked, asserting that you no longer have authority to repatriate the assets. Additionally, this structure avoids complex IRS filings like Forms 3520 and 3520-A during its domestic phase, simplifying compliance.

For added protection, Global Wealth Protection may recommend combining a Cook Islands trust with a Nevis LLC. This forces creditors to navigate multiple legal systems, each with its own litigation bond requirements – approximately $50,000 in the Cook Islands and $100,000 in Nevis. The firm also handles compliance with regulations like FBAR, FATCA, and the Corporate Transparency Act (CTA) filings.

With these services in place, here’s how you can set up an offshore asset protection structure.

Steps to Create an Offshore LLC or Trust

The process begins with selecting the right jurisdiction. Global Wealth Protection helps you choose based on your needs. For instance:

- Cook Islands: Known for its 40-year history of favorable case law, it requires creditors to prove fraudulent intent "beyond a reasonable doubt", a standard typically reserved for criminal cases. Fraudulent transfer claims are also limited to one to two years.

- Nevis: Offers strong LLC protections.

- Belize: Features favorable rules on fraudulent conveyance.

Once the jurisdiction is selected, the firm establishes the trust structure. This includes appointing an independent Trust Protector and a Special Successor Trustee, both based offshore. For a layered approach, they might set up an Asset Management Limited Partnership or Arizona Limited Partnership to hold economic interests. State-specific LLCs can also be created beneath the trust to manage operational liabilities. For example, a California LLC might hold real estate in California, with ownership ultimately tied to the offshore trust.

Timing matters. It’s crucial to establish your structure before any legal threats arise. Transfers made after a legal threat could be reversed as fraudulent conveyances. As attorney Brian T. Bradley emphasizes:

"Structure must exist before the threat arises".

After setup, Global Wealth Protection oversees ongoing compliance, including annual trustee fees, which typically range from $10,000 to $25,000, and required reporting. The initial cost to establish an offshore trust usually falls between $20,000 and $50,000.

To successfully invoke the impossibility defense during legal duress, you must relinquish control to an independent foreign trustee. Courts will closely examine whether you genuinely lack the ability to repatriate assets. The Bridge Trust® is designed to facilitate this process seamlessly, ensuring control shifts when needed.

Conclusion: Moving Beyond Domestic LLC Limitations

Key Takeaways

Domestic LLCs often fall short when it comes to asset protection. Many state laws allow creditors to go beyond charging orders, which are supposed to limit their remedies. In about one-third of U.S. states, courts have even permitted creditors to foreclose on LLC interests. Single-member LLCs are especially at risk. Courts in states like Florida, Colorado, and Maryland have ruled that these entities don’t benefit from charging order protections because there are no additional, "innocent" members to safeguard the assets.

Another critical point: courts usually apply the laws of the state where you live or where your assets are located – not the state where your LLC was formed. Estate planning attorney Eric Ridley puts it bluntly:

"California doesn’t give a damn where you incorporated your LLC. If you’re a California resident conducting business in California… California law applies. Full stop."

Federal bankruptcy courts add another layer of vulnerability by bypassing state-level protections and allowing asset liquidation to settle creditor claims. On the other hand, offshore jurisdictions like the Cook Islands and Nevis offer a stark contrast. These jurisdictions generally don’t recognize U.S. court judgments, requiring creditors to re-litigate their claims under much stricter standards.

Given these risks, taking decisive steps to protect your assets is not optional – it’s essential.

Next Steps for Protecting Your Assets

If you haven’t already, it’s time to rethink your asset protection strategy. Timing is everything. Offshore structures must be established before any legal issues arise. Otherwise, any asset transfers made after a lawsuit is filed may be labeled as fraudulent.

Global Wealth Protection specializes in creating offshore trusts and LLCs in jurisdictions known for their strong asset protection laws. For individuals with significant wealth and liability exposure, these offshore structures present major legal hurdles for creditors, making it far more challenging for them to access your assets.

Setting up offshore protection does require an upfront investment – around $50,000 initially – along with ongoing maintenance costs. While these costs are higher than those for domestic LLCs, the enhanced security they provide is well worth it.

To move beyond the vulnerabilities of domestic LLCs and safeguard your wealth, explore your options with Global Wealth Protection today. A proactive approach now can save you from significant financial risks down the road.

FAQs

When is a charging order not the only remedy?

When state laws allow creditors to take additional steps beyond a charging order – like foreclosing on or dissolving the LLC – this can present significant risks. Such actions are more likely in states that lean toward being favorable to creditors or in particular circumstances, such as bankruptcy cases. These scenarios underscore the fact that domestic LLCs may not always provide the level of asset protection some might expect.

Why are single-member LLCs easier for creditors to attack?

Single-member LLCs face greater risks when it comes to creditor claims. In some states, courts may not fully enforce charging order protections for these entities. As a result, the assets of a single-member LLC can be left unprotected, since these safeguards are often weaker or inconsistently applied in such cases.

When is offshore protection legally “too late” to set up?

Offshore protection often loses its effectiveness once a creditor has already initiated legal action or secured a judgment against you. At that stage, courts are likely to scrutinize or even nullify such arrangements, as they may be viewed as attempts to hide assets or commit fraud. The key is to set up these protections before any legal claims arise. Acting early not only ensures compliance with the law but also helps safeguard your assets more effectively.