Looking to escape high taxes and soaring living costs in Canada? You’re not alone. Over 4 million Canadians now live abroad, drawn to countries offering lower taxes, affordable housing, and a better lifestyle. This guide highlights six destinations – each offering unique tax advantages, residency options, and quality of life benefits.

Key Takeaways:

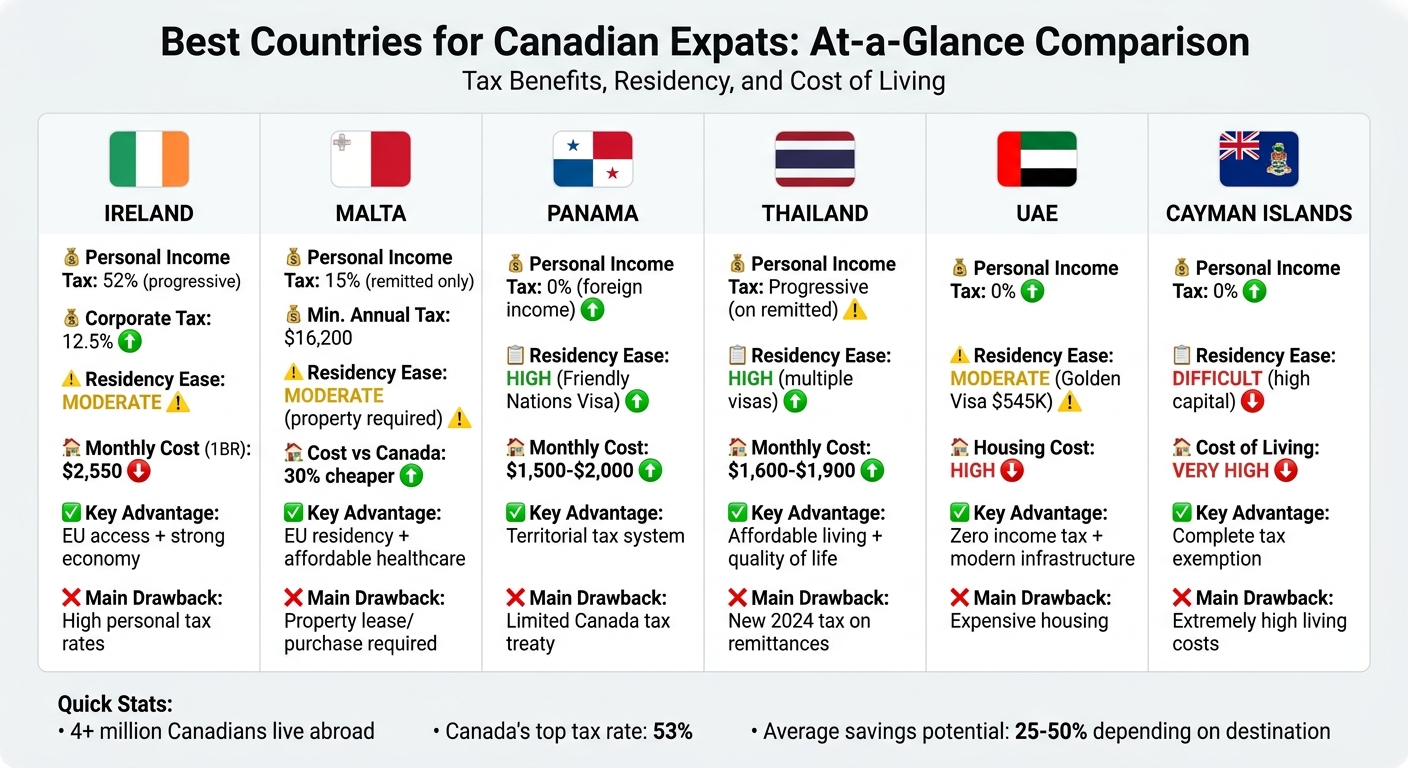

- Ireland: Low corporate tax (12.5%) but high personal income tax and expensive housing.

- Malta: Tax on remitted income only (15%) with affordable living costs and EU access.

- Panama: Zero tax on foreign income, quick residency process, and low living costs.

- Thailand: Low costs, tax-friendly visas, but new rules on foreign income remittances.

- UAE: Zero personal income tax, modern infrastructure, but high housing costs.

- Cayman Islands: Complete tax exemption but extremely high cost of living.

Quick Comparison

| Country | Income Tax | Residency Ease | Cost of Living | Key Advantage | Main Drawback |

|---|---|---|---|---|---|

| Ireland | High | Moderate | Expensive | Strong economy | High personal tax rates |

| Malta | 15% remitted | Moderate (property req.) | Moderate (30% cheaper) | EU residency | Property lease/purchase req. |

| Panama | 0% foreign | High (Friendly Visa) | Low to moderate | Territorial tax system | Limited Canada tax treaty |

| Thailand | Progressive | High (multiple visas) | Low | Affordable living | New tax on remittances |

| UAE | 0% | Moderate (Golden Visa) | High | Zero personal tax | Expensive housing |

| Cayman Islands | 0% | Difficult (high reqs.) | Very high | Complete tax exemption | Very high living costs |

Each destination caters to different priorities – tax relief, affordability, or lifestyle. Whether you’re a retiree, remote worker, or entrepreneur, this guide will help you weigh your options.

1. Ireland

Ireland draws Canadian expats with its low corporate tax rate and English-speaking environment. With a corporate tax rate of 12.5% compared to Canada’s 26.5%, it’s especially appealing to entrepreneurs and business owners. On the personal income tax side, Ireland’s top rate is 52%, slightly below Canada’s 53%.

Tax Benefits

Ireland’s corporate tax rate offers significant savings for businesses. For instance, an individual earning €100,000 annually in Ireland faces an effective tax rate of 35.2%, compared to 22.0% in Canada. Social security contributions are also lower in Ireland at 4%, versus Canada’s 7.59%. The Canada-Ireland double taxation treaty further simplifies financial planning by capping dividend taxes at 15% (or 5% for companies holding at least 10% of voting power) and limiting taxes on interest and royalties to 10%.

For Canadians planning to move, the Departure Tax is a key consideration. This tax treats most property as sold at fair market value upon leaving Canada. While your RRSP can remain tax-deferred, withdrawals as a non-resident are subject to a 25% withholding tax, which can drop to 15% for periodic payments under the treaty. On the other hand, Ireland may not recognize the tax-free growth of a TFSA, potentially taxing its annual gains.

Next, let’s explore Ireland’s residency options for expats.

Residency Options

Ireland offers various residency pathways for Canadians. The Critical Skills Employment Permit targets highly skilled professionals, particularly in tech and healthcare, and requires a minimum monthly income of €3,409. Retirees or individuals with independent means can apply for the Stamp 0 visa, which mandates a verified passive income of at least €50,000 per year. Entrepreneurs, meanwhile, can consider the Start-up Entrepreneur Programme (STEP) to launch high-potential startups. Tax residency in Ireland is typically established by spending 183 days or more in the country during a tax year. These options, combined with Ireland’s tax advantages, create a compelling relocation package.

Cost of Living

While Ireland’s tax benefits and residency options are enticing, the cost of living is an important factor to weigh. Ireland generally has higher living costs than many Canadian cities, though this varies by location. In Dublin, monthly expenses for a single person average around €3,043, with one-bedroom apartments renting for about €2,500. Other cities, like Cork and Galway, are more affordable, with monthly costs around €2,595 and €2,514, respectively – roughly 15–20% less than Dublin. However, Dublin’s housing market presents challenges, with vacancy rates below 1%. Even high earners, such as doctors (earning around €7,000 per month) and software engineers (approximately €5,600 per month), may find it difficult to secure housing.

Lifestyle and Infrastructure

Ireland’s appeal extends beyond taxes and housing. The country’s high level of English proficiency ensures a smooth cultural transition for Canadian expats. Both Ireland and Canada score 9/10 for safety, though Ireland’s healthcare system is rated slightly lower at 7/10 compared to Canada’s 9/10. Dublin’s thriving tech scene provides strong career opportunities, despite housing challenges. However, Ireland’s 23% VAT – much higher than Canada’s 5% sales tax – can impact everyday expenses.

sbb-itb-39d39a6

2. Malta

Malta is a favorite for Canadian expats, thanks to its remittance-based tax system and Mediterranean charm. Unlike Canada’s global taxation approach, Malta only taxes non-domiciled residents on income earned within the country or foreign income brought into Malta. Any foreign income left outside Malta stays completely tax-free. This setup offers significant savings for Canadians with pensions, investment income, or remote work earnings.

Tax Benefits

Malta’s tax structure is particularly appealing when compared to Canada’s system. Through the Global Residence Programme (GRP) and Malta Retirement Programme (MRP), foreign income remitted to Malta is taxed at a flat 15% rate. For retirees under the MRP, the minimum annual tax is €7,500 (around $8,100) for the main applicant, with an additional €500 (approximately $540) per dependent. GRP participants face a higher minimum annual tax of €15,000 (roughly $16,200).

Non-domiciled residents also enjoy tax-free foreign capital gains, even if those gains are remitted to Maltese accounts. This is a stark contrast to Canada’s approximate 25% tax on investment income. Additionally, the Canada-Malta tax treaty, signed in 1986, ensures no double taxation on pensions like CPP and OAS. Malta also stands out by not imposing wealth, inheritance, or annual property taxes.

Next, let’s look at Malta’s various residency programs tailored to different income levels.

Residency Options

Canadians, classified as "Third Country Nationals", have several pathways to residency in Malta. The Global Residence Programme is aimed at high-income individuals and requires either purchasing property valued at €275,000 (€220,000 in Gozo or South Malta) or renting for at least €9,600 annually (€8,750 in Gozo/South Malta). The administrative fee is €6,000, or €5,500 for properties in less expensive areas. This program also allows four generations of family members to be included in a single application.

For retirees, the Malta Retirement Programme is designed for those whose pensions make up at least 75% of their income. Applicants are required to reside in Malta for an average of 90 days per year. Remote workers earning a gross monthly income of at least €3,500 can apply for the Nomad Residence Permit, which is renewable for up to four years.

Jean-Philippe Chetcuti, Senior Partner at Chetcuti Cauchi Advocates, explains: "The Malta Global Residence Programme 2026 remains Malta’s longest-standing residence and special tax status framework for non-EU, non-EEA, and non-Swiss nationals seeking a lawful European base without mandatory relocation".

Cost of Living

Living costs in Malta are about 15.4% lower than in Canada when rent is included. Rent itself is approximately 17.7% cheaper, with a one-bedroom apartment in the city center costing around €953 (about $1,030) compared to €1,147 (roughly $1,240) in Canada. Utility bills for a typical 915-square-foot apartment are 33.1% lower, and internet service costs 43.1% less. Grocery prices also show noticeable savings – milk is 42% cheaper, while bread costs 51.4% less than Canadian prices.

On the flip side, gasoline is 30.4% more expensive in Malta. Expats should also plan for private health insurance, which is mandatory for most residency permits and must cover EU-related risks. Malta’s VAT rate of 18% is higher than most Canadian provincial sales taxes. For those looking to invest in property, Gozo and South Malta offer more affordable options, making them attractive to budget-conscious expats.

These financial perks are complemented by Malta’s appealing lifestyle, which we’ll explore next.

Lifestyle and Infrastructure

Malta offers more than just tax and residency perks – it provides a high quality of life for expats. With over 300 days of sunshine annually and English as an official language, Canadian expats won’t face language barriers. Residency permits also grant visa-free travel throughout the Schengen Area for up to 90 days within any 180-day period. For families, international primary schools cost around €14,375 (approximately $15,550) annually, about 13% less than Canada’s €16,572 average. Public transportation is another budget-friendly feature, with monthly passes often free or heavily subsidized for residents.

Malta’s compact size and Mediterranean weather make it especially appealing for retirees and remote workers. However, local salaries average 40.6% lower than in Canada, meaning the island is most suitable for those with foreign income or pensions rather than relying on local employment.

3. Panama

Panama attracts Canadian expats with its territorial tax system and the convenience of using the U.S. Dollar. Unlike Canada, which taxes residents on their worldwide income, Panama only taxes income earned within its borders. This means foreign-sourced income – like Canadian pensions, remote work earnings, and investment returns – can generally avoid taxation, offering potential savings compared to Canada’s higher rates, which can exceed 50%.

Tax Benefits

Panama’s territorial system ensures that income earned abroad remains untaxed, provided you officially sever your Canadian tax residency. Once you’re a Panamanian resident, distributions from TFSAs can grow and be withdrawn entirely tax-free. Additionally, under the Canada–Panama tax treaty, Canadian pension payments (such as RRIF withdrawals, CPP, or OAS) are subject to a reduced non-resident withholding tax of 15%, down from the standard 25%.

Locally earned income in Panama follows a tiered tax system: income up to $11,000 is tax-free, income between $11,001 and $50,000 is taxed at 15%, and anything above $50,000 is taxed at 25%. Starting in 2026, multinational entities in Panama will need to demonstrate genuine economic activity – such as employing local staff and maintaining office space – to retain the 0% tax rate on foreign-sourced passive income.

"Panama is not just a retirement destination anymore. It has become a structured jurisdiction for professionals, entrepreneurs, and high-net-worth individuals who want access to a USD economy." – Ipanema Partners

Before leaving Canada, you’ll face a "deemed disposition" tax, where the Canada Revenue Agency treats your assets as sold at fair market value. However, assets like Canadian real estate and registered accounts (e.g., RRSPs and TFSAs) are exempt from this tax. To fully benefit from Panama’s tax system, you’ll need to formally sever ties with Canada by adjusting personal connections such as your primary residence, health insurance, and driver’s license.

These tax advantages make Panama an attractive option for those looking to reduce their tax burden.

Residency Options

Canadians can choose among three primary routes to secure Panamanian residency:

- Friendly Nations Visa (FNV): Requires a $200,000 investment in real estate or a three-year fixed-term bank deposit. Government fees are approximately $1,050 for a single applicant. This visa grants provisional residency for two years, after which permanent status can be obtained.

- Qualified Investor Visa (QIV): Offers a faster option, granting permanent residency within 30 to 45 working days for a $300,000 real estate investment. However, starting October 15, 2026, the minimum investment will rise to $500,000.

- Pensionado Visa: Tailored for retirees, this visa requires a guaranteed lifetime pension of at least $1,000 per month. If you purchase Panamanian real estate worth at least $100,000, the pension requirement drops to $750 per month. Holders of this visa also enjoy discounts such as 25% off utility bills, 50% off cinema and concert tickets, and 20% off medical consultations.

Applicants must visit Panama City twice – once for biometric registration and again to collect their residency card. A fingerprint-based RCMP criminal record check (authenticated and apostilled by Global Affairs Canada) is required, and it’s only valid for 3–6 months, so timing is crucial. Opening a Panamanian bank account often requires original reference letters from Canadian banks and proof of income or wealth. An immigration attorney’s introduction can simplify this process.

Cost of Living

Panama offers a blend of favorable tax policies and a lower cost of living, making it appealing to expats focused on financial efficiency. Overall, living costs in Panama are estimated to be 25% to 34% lower than in Canada. For example:

- A one-bedroom apartment in Panama City averages $1,310 per month.

- Utilities for a 915-square-foot apartment cost about $151, compared to $205 in Canada.

- Dining out is also cheaper – a meal for two at a mid-range restaurant costs around $71.70 compared to $100 in Canada.

Healthcare is another area where Panama shines. Private consultations with specialists typically cost $15 to $20, while local HMO plans for expats aged 50 to 59 are around $94 per month. Panama City also boasts a strong private hospital network, including four JCI-accredited facilities, one of which is affiliated with Johns Hopkins Medicine. A couple can live comfortably in Panama on a monthly budget of $2,000 to $3,000.

Lifestyle and Infrastructure

Panama combines affordability with quality living. Using the U.S. Dollar eliminates currency exchange risks for Canadians holding USD assets. In 2026, Panama was ranked #1 out of 53 countries for expat satisfaction. The climate varies across the country: while Panama City and coastal areas often require air conditioning year-round, highland towns like Boquete enjoy a cooler, spring-like climate, which can help reduce utility bills.

New construction properties may qualify for property tax exemptions of up to 20 years. Foreigners have the same property ownership rights as locals, except for land within 6.2 miles (10 km) of international borders. It’s important to avoid "Right of Possession" (ROP) land, which lacks legal protections and doesn’t qualify for residency visas. Always hire an independent Panamanian attorney to verify property titles through the Public Registry, rather than relying solely on a seller’s attorney.

Spending more than 183 days a year in Panama qualifies you as a Panamanian tax resident, allowing you to obtain a Tax Residency Certificate for the CRA. Legal fees for residency applications typically range from $2,000 to $4,000.

4. Thailand

Thailand is an attractive destination for Canadian expats looking for both tax benefits and an enhanced lifestyle. In the 2025 InterNations Expat Insider survey, Thailand ranked fourth as a preferred location for expatriates. Unlike Canada’s global income taxation system, Thailand uses a tax residency rule: you become a tax resident after spending 180 days or more in the country. This creates opportunities for Canadians to take advantage of Thailand’s tax-friendly policies.

Tax Benefits

Starting January 1, 2024, Thailand began taxing remitted foreign-sourced income for tax residents. However, the Long-Term Resident (LTR) visa offers a way around this. For "Wealthy Global Citizens" and "Wealthy Pensioners", foreign-sourced income remains exempt, while highly skilled professionals are taxed at a flat 17% rate – much lower than Thailand’s progressive rates, which go up to 35%.

Thailand also has a Double Taxation Agreement (DTA) with Canada. This allows Canadians to claim foreign tax credits to avoid being taxed twice on income already taxed in Canada. To take advantage of the DTA, expats need a Certificate of Residence from the CRA and accurate records of taxes paid abroad. Additionally, capital gains from shares listed on the Stock Exchange of Thailand are tax-free, and dividend income generally has a 10% withholding tax.

"The LTR visa is a financial instrument designed for tax optimization, whereas the Privilege visa is a premium product focused on convenience and lifestyle." – Forbes & Partners Editorial Team

These policies make Thailand especially appealing for Canadians with significant foreign income. For instance, a Canadian software developer earning $90,000 CAD annually could see about 50% more purchasing power by relocating to Thailand.

Residency Options

Thailand offers various visa options to suit the needs of Canadian expats:

- Destination Thailand Visa (DTV): This 5-year, multiple-entry visa is ideal for remote workers, freelancers, and individuals involved in cultural activities. It costs 10,000 THB (about $350 CAD) and allows stays of up to 180 days per entry, extendable to 360 days. Applicants must show a personal account balance of 500,000 THB (joint accounts are not accepted).

"For Canadian remote workers earning CAD 60,000+, the DTV is the least friction pathway to long-term stay." – Nic Bunpamee, Immigration Consultant, Issa Compass

- Long-Term Resident (LTR) Visa: This 10-year visa is tailored for high-net-worth individuals, wealthy retirees, and highly skilled professionals. With a government fee of 85,000 THB (around $3,270 CAD), it replaces the 180-day rule with an annual reporting requirement.

- Retirement Visa (Non-OA/O): Available to Canadians aged 50 and older, this visa requires either 800,000 THB in a Thai bank account or a monthly pension of 65,000 THB (approximately $2,500 CAD). Funds must remain untouched for two months before applying and three months after approval. Annual renewals are required, but entering Thailand on a tourist visa and converting to a Non-Immigrant O visa can bypass the need for costly health insurance.

Same-sex spouses now qualify for dependent visas under both the O and LTR visa pathways, thanks to the 2025 Marriage Equality Act. Additionally, Canadian expats can receive CPP and OAS payments directly into Thai or Canadian bank accounts without facing Canadian tax penalties.

Cost of Living

Thailand offers a much lower cost of living compared to Canada. Excluding rent, expenses are 41.4% lower, and including rent, they are 46.6% lower. Rent is where the savings are most noticeable – Thai rental prices are approximately 59.2% cheaper than in Canada. For example, a one-bedroom apartment in central Bangkok typically costs $400–$700 USD, compared to $2,000–$3,500 CAD in major Canadian cities.

Other savings include:

- Utilities: Monthly costs for a 915-square-foot apartment average $113.40 CAD in Thailand, compared to $205.80 CAD in Canada (44.9% lower).

- Internet: High-speed internet (60 Mbps or higher) costs around $24.40 CAD per month, compared to $84.90 CAD in Canada.

- Transportation: Public transit is 67.7% cheaper, with one-way tickets costing about $1.10 CAD.

A comfortable monthly budget for a single person in Bangkok ranges from $1,200 to $1,800 USD. Dining out is also far more affordable – a meal at an inexpensive restaurant costs about $4.30 CAD, compared to $25.00 CAD in Canada, translating to an 82.9% savings. However, imported goods like cheese may cost up to 60.5% more than in Canada.

Healthcare

Thailand provides excellent value in healthcare. Private specialist consultations range from $30 to $60 USD, and many medical procedures cost 50% to 75% less than in Western countries. For instance, heart bypass surgery costs around $13,000 USD in Thailand, compared to $113,000 USD in the United States. However, medical inflation reached 15.2% in 2024, significantly outpacing the general consumer price index.

Lifestyle and Infrastructure

Thailand’s modern infrastructure adds to its appeal for expats. The country ranks 13th globally in fixed broadband speeds, with an average of 237 Mbps. Fast fiber internet is widely available in popular digital nomad hubs like Chiang Mai. Bangkok’s growing rail system, including new Yellow and Pink lines, improves mobility, while electric vehicle registrations surpassed 126,000 in 2025, capturing 18%–20% of the market.

"Thailand has moved from passively accommodating long-term foreigners through grey-area loopholes to actively choosing which foreigners it wants." – Ryan Turner, Journalist

While foreigners cannot own land, they can buy condominiums under the 49% foreign ownership quota or secure long-term leaseholds. However, expats should be aware of seasonal air quality issues, especially during the "burning seasons" in Northern Thailand and periods of high PM2.5 levels in Bangkok. Climate conditions also vary – Bangkok and coastal areas often require year-round air conditioning, while northern regions enjoy cooler weather.

To stay tax-compliant, expats are advised to keep separate accounts for "Pre-2024 Savings" and "New Income" to provide clear evidence for tax authorities. Most expats must complete a 90-day check-in (now largely digital via the IMMO-Online portal), though LTR visa holders are exempt.

5. United Arab Emirates

The United Arab Emirates is a top choice for Canadian expats looking for a tax-friendly environment. With a 0% personal income tax rate, the UAE stands in stark contrast to Canada’s progressive tax system, where high earners can see nearly half their income go to taxes. This zero-tax policy makes the UAE especially appealing for Canadians aiming to keep more of their earnings.

Tax Benefits

The UAE’s tax system is straightforward – there’s no personal income tax on salaries, wages, or investment income. However, leaving Canada’s tax system isn’t as simple as relocating. Canadians must formally sever primary ties, such as selling or renting out their Canadian home, and secondary ties, like closing Canadian bank accounts or canceling health coverage. Without these steps, Canadian tax obligations may continue to apply.

"Under the UAE-Canada tax treaty, only UAE nationals are recognised as tax residents of the UAE for treaty purposes." – TLP Advisors

This treaty clause means Canadian expats can’t use standard tie-breaker rules to claim UAE residency. Instead, they must prove their non-residency under Canadian law. To strengthen their case, expats should apply for a Tax Residency Certificate from UAE authorities after spending at least 183 days in the country [46,48]. For entrepreneurs, the UAE’s new 9% corporate tax is still far lower than Canada’s rates. Ensuring that the "Place of Effective Management" for their business is clearly in the UAE can help avoid unexpected tax issues.

Once the tax advantages are clear, the next step is to explore residency options.

Residency Options

The UAE offers a variety of visa pathways tailored to different needs, with 26 visa options compared to Canada’s 15. Canadian citizens can enter the UAE on a 90-day visa-on-arrival, free of charge, for tourism [52,53]. For employment, the Standard Work Visa is the most common, lasting 2 to 3 years and sponsored by a UAE employer.

For more flexibility, the Green Visa provides a 5-year self-sponsored option for freelancers, skilled workers, and self-employed individuals who meet minimum income requirements. High-net-worth individuals and professionals may qualify for the Golden Visa, offering 5 or 10 years of residency in exchange for a minimum investment of about $545,000 (AED 2 million).

Remote workers can take advantage of the Virtual Work Visa, which costs roughly $500 and allows them to live in the UAE while working for an overseas employer. This visa is processed in just 5 to 7 days, with a minimum monthly income requirement of $3,253 [47,49]. Canadians aged 55 and older can also apply for the Retirement Visa, a 5-year residency option for those meeting specific financial criteria.

All residency applicants must pass a medical fitness test, including screenings for HIV and tuberculosis, and secure mandatory health insurance. Basic health plans start at around $120 annually, with new requirements in Dubai and Abu Dhabi taking effect in 2025 [50,51,52]. Once residency is granted, Canadians can easily exchange their driver’s license for a UAE equivalent without taking a road test.

Now that visas and tax benefits are covered, let’s look at the cost of living in the UAE.

Cost of Living

Living costs in the UAE can vary depending on lifestyle and location. Overall, expenses are about 5.2% higher than in Canada when rent is included, though day-to-day costs (excluding rent) are approximately 7.2% lower. Housing is the biggest expense. A one-bedroom apartment in a city center averages $2,383.50 per month, compared to $1,838.90 in Canada – a 29.6% difference. For a three-bedroom apartment, the gap widens to $4,729.60 in the UAE versus $2,950.60 in Canada, a 60.3% increase. Opting for areas outside city centers, like Sharjah, can cut housing costs to around $1,650 per month compared to $3,093 in central Dubai.

Other costs are more budget-friendly. Gasoline is about $1.10 per liter, roughly 30% cheaper than in Canada. Public transit passes cost $78 per month versus Canada’s $105. Food is also more affordable – chicken fillets and meals at inexpensive restaurants are 28.2% and 37.6% cheaper, respectively. On the other hand, utilities and internet services are pricier, with basic bills about 26.2% higher and internet costs over 70% more than in Canada.

Higher salaries in the UAE help balance these costs. For example, software engineers earn an average of $6,720 per month compared to $5,120 in Canada, while AI engineers make $7,560 versus $5,760.

Lifestyle and Infrastructure

The UAE combines modern infrastructure with a high standard of living. It boasts a safety rating of 9/10 and a quality of life score of 8/10. Over 40,000 Canadians currently live in the UAE, with many choosing Dubai as their home. The UAE Dirham is pegged to the US Dollar, adding an extra layer of financial stability.

Residents enjoy a 4.5-day work week, and international schools are widely available, with annual fees ranging from $13,000 to $25,500. While the UAE’s healthcare quality index is slightly lower than Canada’s (78 versus 88), mandatory health insurance requires an annual coverage limit of at least $57,025 [47,48].

Practical tools like Wise can simplify currency conversions between Canadian dollars and AED, making relocation expenses easier to manage. Additionally, family sponsorship is possible under the "3000 Dirham rule", which requires a minimum salary of AED 3,000 (about $1,012) with company-provided housing, or AED 4,000 without [47,51].

6. Cayman Islands

The Cayman Islands provide a zero-tax environment for Canadian expats, blending financial perks with an appealing lifestyle. Compared to Canada’s top income tax rate of 53%, the Cayman Islands impose 0% tax on personal income, capital gains, corporate earnings, inheritance, dividends, and wealth. There’s also no VAT or sales tax to worry about.

Tax Benefits

The tax system here is refreshingly simple, with no direct taxes. However, due to the lack of tax treaties with Canada, government payments like CPP and OAS are subject to a 25% withholding tax. The government generates revenue through indirect means, such as a 22% duty on most imported goods and a 7.5% stamp duty on real estate transactions. For example, an expat earning $100,000 keeps the entire amount, unlike in Canada, where a significant portion would go to taxes.

"Where you live now, you work for the government until March 18. In Cayman, every dollar is yours from day one." – ListCayman

Let’s take a closer look at the options available for obtaining residency in the Cayman Islands.

Residency Options

Canadian expats can choose from several residency options in the Cayman Islands. The Residency Certificate for Persons of Independent Means requires an investment of CI$1 million (with at least CI$500,000 in real estate), proof of an annual income of CI$120,000, and a CI$20,000 grant fee. This 25-year certificate requires residents to spend 30 days per year on the islands but does not allow employment.

For those seeking more flexibility, the Certificate of Permanent Residence demands a CI$2 million investment in developed real estate and a CI$100,000 grant fee. This option permits employment (with government approval) and requires just one day of presence per year. After 15 years, residents can apply for British Overseas Territories Citizenship.

Entrepreneurs and remote workers might prefer the Special Economic Zone (SEZ), which offers an expedited setup process in just five days for about US$15,000 annually. Regardless of the pathway, all residents must have health insurance, with premiums ranging from CI$200 to over CI$800 per month.

While the tax benefits are clear, it’s crucial to weigh the cost of living and lifestyle factors before making the move.

Cost of Living

The Cayman Islands are known for higher living costs compared to Canada. Renting a one-bedroom apartment typically costs between US$2,000 and US$3,500 per month, while a three-bedroom family home ranges from US$4,500 to US$8,000. Utilities add another US$300 to US$600 monthly. Groceries are significantly more expensive – often 50% to 100% higher than in the U.S. – with a couple’s monthly food budget running from US$800 to US$1,200.

Healthcare is another major expense. A general practitioner visit costs around US$100 to US$200, and health insurance premiums range from US$300 to US$800 per month per person. For families with children, private school tuition falls between US$10,000 and US$25,000 annually. Gasoline prices are approximately US$1.60 per liter. While initial relocation costs are steep – averaging around US$25,000 – expats often recoup these expenses within 32 months thanks to the lack of direct taxes. The Cayman Islands Dollar (KYD) is pegged to the U.S. Dollar at a fixed rate of 1.00 KYD = 1.20 USD.

Lifestyle and Infrastructure

The Cayman Islands boast political stability and a legal system based on English Common Law. As a global financial hub, the islands host over 100 licensed banks and manage 75% of the world’s offshore hedge funds, making it the fifth-largest financial center worldwide. The population of around 80,000 includes residents from over 135 nationalities.

Modern infrastructure supports a high standard of living. Internet speeds average 80 Mbps, and healthcare facilities, such as Doctors Hospital, are top-notch. The islands are also considered relatively safe, with a safety rating of 7.2 out of 10. Public schooling is reserved for Caymanians, so expats typically enroll their children in private international schools offering U.K. or U.S. curricula.

"The best doctors here are as good as anywhere in the world." – Andrew Hallam, Author and Expat Expert

Comparison of Advantages and Disadvantages

Taking a closer look at the country profiles, this comparison highlights the main pros and cons of each destination. Every location comes with its own set of trade-offs, whether in tax savings, ease of residency, cost of living, or overall lifestyle.

Here’s a breakdown of key factors across six countries:

| Country | Personal Income Tax | Ease of Residency | Affordability | Key Advantage | Key Drawback |

|---|---|---|---|---|---|

| Ireland | Progressive (high rates) | Moderate (EU/business focus) | High (about $2,550/month for a 1BR in Dublin) | EU access and a strong economy | High taxes and steep housing costs |

| Malta | 15% on remitted income (min. ~$16,200 annual tax) | Moderate (property requirement) | Moderate (around 30% cheaper than Canada) | EU residency and affordable healthcare | Mandatory property lease or purchase |

| Panama | 0% on foreign income | High (Friendly Nations Visa) | Low to moderate ($1,500–$2,000/month) | Territorial tax system and quick residency process | Limited tax treaty with Canada |

| Thailand | Progressive on remitted income | High (retirement and digital nomad visas) | Low ($1,600–$1,900/month) | Affordable living paired with high quality of life | New 2024 tax rule on remittances |

| UAE | 0% personal income tax | Moderate (Golden Visa requires ~$545,000 property) | High (expensive housing and private health insurance) | Zero income tax and modern infrastructure | Premium living costs |

| Cayman Islands | 0% on all income | Difficult (high capital requirements) | Very high | Complete tax exemption | Extremely high cost of living |

Panama stands out for its Friendly Nations Visa, offering quick residency and a territorial tax system that exempts foreign income. Thailand is appealing for its low cost of living and quality of life, though its recent tax rules on remittances require careful financial planning. The UAE and Cayman Islands both boast zero personal income tax, but they come with significant capital requirements and high living expenses. Malta offers a balanced option with moderate costs, EU residency, and affordable healthcare, though its flat tax rate and minimum annual tax might not fit every budget. Ireland, while providing strong economic opportunities and EU access, has limited tax benefits for expats due to its progressive tax system and high housing costs.

Ultimately, your choice depends on your priorities – whether you value tax savings, affordability, or residency benefits the most.

Conclusion

Choosing the right destination for relocation depends entirely on what matters most to you. If your main priority is avoiding personal income tax, places like the UAE and Cayman Islands provide a tax-free haven – though they come with higher living expenses. On the other hand, if you’re looking for a balance between affordability and territorial tax advantages, Panama and Thailand are appealing options. These countries allow you to keep your foreign income untaxed while maintaining a comfortable lifestyle for $1,500 to $2,000 per month. Malta offers a middle ground, combining EU residency benefits with moderate costs and an English-speaking environment. Meanwhile, Ireland remains a solid choice for professionals, offering economic opportunities despite its relatively higher taxes. The key is to match your financial goals with your lifestyle preferences.

Before making the leap, spend at least a month in your chosen country to get a feel for everyday life beyond the tourist spots. Investigate whether tax treaties are in place to reduce CPP and OAS withholding tax from 25% to 15%. Also, prepare essential documents like criminal record checks and proof of financial stability, keeping in mind that authentication and apostille processes can take up to 6 to 12 weeks.

"Choosing a country isn’t just about the lowest tax rate. The sovereign individual who picks Paraguay purely for its 10% flat tax but hates South American culture… is going to be miserable." – Sovereign Nomad

To finalize your new residency, make sure to complete critical steps such as closing your primary Canadian accounts. This includes selling or leasing your residence, canceling provincial health insurance, and surrendering your driver’s license. Inform your Canadian banks about your move to transition your accounts to non-resident status, preventing unexpected closures. Additionally, you might want to convert RRSPs to RRIFs before leaving, as this could lower your withholding tax rate under certain treaties.

Ultimately, relocation is more than just a financial decision – it’s about aligning your move with your personal values, family needs, and long-term goals. With over 4 million Canadians already living abroad, you’ll be joining a growing group of individuals who have successfully combined tax efficiency with an enhanced quality of life.

FAQs

How do I prove I’m no longer a Canadian tax resident after moving abroad?

To demonstrate that you’re no longer a Canadian tax resident, you need to show that you’ve cut primary ties – like owning a home in Canada, having a spouse or common-law partner there, or supporting dependents. You’ll also need to address secondary ties, such as owning property, maintaining social connections, or holding a Canadian driver’s license.

Key steps include:

- Establishing residency in another country

- Canceling your Canadian health coverage

- Filing a final tax return that includes your departure date

It’s a good idea to consult a tax professional to make sure you meet all requirements and have the right documentation in place.

What happens to my RRSP, TFSA, CPP, and OAS when I become a non-resident?

As a non-resident, RRSPs (Registered Retirement Savings Plans) remain untaxed in Canada until you make withdrawals, which are subject to a 25% withholding tax. However, this rate can sometimes be reduced if a tax treaty exists between Canada and your new country of residence.

TFSAs (Tax-Free Savings Accounts), on the other hand, may become taxable depending on the tax laws of the country you move to, as some countries don’t recognize the tax-exempt status of TFSAs.

For government benefits, CPP (Canada Pension Plan) payments will continue regardless of where you live. However, OAS (Old Age Security) payments will stop unless you’ve lived in Canada for at least 20 years after turning 18. Lastly, GIS (Guaranteed Income Supplement) payments end after six months of living abroad.

Which country is best if I earn foreign income remotely and want to minimize taxes legally?

The United Arab Emirates (UAE) stands out as a top choice for earning foreign income remotely while keeping taxes low – legally. With its 0% personal income tax rate, it’s an appealing destination for remote workers and digital nomads. Similarly, other tax-free nations like Monaco and Qatar also offer enticing opportunities for individuals aiming to reduce their tax obligations.