Protecting your assets during a divorce can be challenging, especially if you rely solely on domestic strategies like prenuptial agreements or U.S.-based trusts. Courts in the U.S. often have broad authority to invalidate these protections, leaving your wealth exposed. Offshore structures, such as trusts and LLCs in jurisdictions like the Cook Islands or Nevis, offer a stronger alternative. These jurisdictions operate under legal systems that don’t recognize U.S. court orders, making it significantly harder for ex-spouses to access your assets.

Key Takeaways:

- Domestic trusts and prenups often fail: U.S. courts can override them, especially in divorce cases.

- Offshore asset protection trusts (OAPTs): These are governed by foreign laws, making U.S. judgments unenforceable.

- Offshore LLCs: Provide control over assets while shielding them from divorce settlements.

- Top jurisdictions: Cook Islands, Nevis, and Belize offer strong asset protection with strict legal barriers.

- Timing matters: These structures must be set up before any legal disputes arise to avoid claims of fraudulent transfers.

Offshore strategies require careful planning, compliance with tax laws, and early implementation to ensure they hold up under scrutiny. By combining trusts and LLCs, you can create a layered defense that’s far more resilient than U.S.-based options.

Why U.S. Asset Protection Fails in Divorce Cases

Domestic asset protection strategies often fall short in divorce cases. Family courts wield extensive equitable powers to evaluate and divide assets based on fairness, regardless of the legal structures protecting them. Judges can bypass formalities, prioritizing what they consider just over strict adherence to trust or corporate laws.

One major factor is jurisdiction. U.S. courts retain personal jurisdiction over residents, granting judges the authority to demand asset disclosures, repatriate funds, or impose penalties – even when assets are held in domestic trusts or LLCs. Attorney Brian T. Bradley explains:

"A spouse is not a creditor. They are a co-owner of marital property. Family courts therefore operate with broader authority than creditor courts".

This broad authority leaves prenuptial agreements and domestic trusts vulnerable during divorce proceedings.

How Courts Override Prenuptial Agreements

Prenuptial agreements are frequently scrutinized and can be invalidated for several reasons. Courts examine both how the agreement was signed (procedural fairness) and whether its terms are oppressive (substantive fairness). Agreements presented shortly before a wedding are especially vulnerable to claims of coercion or undue influence [8, 9]. Failure to provide "fair, reasonable, and full disclosure" of assets, income, and debts is another common reason courts void prenups.

California law adds further restrictions, requiring that spousal support waivers are enforceable only if the waiving party had independent legal counsel at the time of signing. The case In re Marriage of Pendleton & Fireman demonstrated how prenups could be challenged for unconscionability at the time of enforcement. For example, a spouse leaving their career to raise children might render an agreement that once seemed fair unenforceable. Federal law also complicates matters, as ERISA prevents prenups from overriding certain retirement benefits unless a Qualified Domestic Relations Order (QDRO) is in place.

As one family law resource puts it:

"A prenup that cuts corners is a prenup that fails when it matters most" – Family Law Matters.

While prenups face these hurdles, domestic trusts are also far from foolproof in divorce cases.

Why Domestic Trusts Don’t Protect Assets in Divorce

Domestic Asset Protection Trusts (DAPTs) face significant challenges in divorce. Many states classify former spouses as "exception creditors", meaning they can access trust assets despite the trust’s protections. The Full Faith and Credit Clause further undermines DAPTs by allowing courts to apply the laws of the settlor’s home state, rather than the trust’s home state, if the two differ.

For instance, in In re Huber (2013), the U.S. Bankruptcy Court for the Western District of Washington invalidated an Alaska DAPT created by a Washington resident, applying Washington law instead of Alaska’s protective statutes. Similarly, under Bankruptcy Code §548(e), transfers to self-settled trusts can be voided if made within 10 years of filing bankruptcy with the intent to hinder creditors. In Battley v. Mortensen (2011), a federal court in Alaska voided an Alaska DAPT under these provisions.

Federal tax enforcement further complicates DAPTs. In United States v. Huckaby (2026), a federal court ruled that a Nevada DAPT failed to shield California real property from an IRS lien, showing how federal law and property location can override state trust statutes.

Commingling marital funds with trust assets creates additional risks. If marital funds are used for trust expenses or joint assets are added to a pre-marital trust, courts may declare the trust "transmuted" into marital property. The high-profile divorce of billionaire Tony Pritzker in 2024 highlighted these challenges. Despite holding a $150–$200 million estate through trusts and LLCs, disputes arose over residential rights tied to beneficiary status.

Courts can also force compliance regardless of trust structures. In Harnack v. Fanady (2026), the Illinois Appellate Court upheld the incarceration of Steve Fanady for contempt after he spent over a decade avoiding a divorce judgment by transferring assets offshore. The court stated:

"A party cannot avoid court orders by deliberately placing assets out of reach through foreign trust structures… he also cannot avoid his obligations to his former spouse by structuring his assets in an offshore trust with the express goal of ‘making himself uncollectable’".

As summarized by Asset Protection Planners:

"Case law reveals significant weaknesses in domestic trusts. Results-oriented judges frequently pierce them, leaving assets exposed. In fact, more domestic trusts fail to protect assets in divorce cases than succeed".

These legal gaps and jurisdictional challenges underscore why many turn to offshore structures as a more secure alternative. Understanding why offshore asset protection provides superior security is the first step in safeguarding wealth.

sbb-itb-39d39a6

Offshore Asset Protection Trusts (OAPTs)

Offshore Asset Protection Trusts (OAPTs) operate under foreign legal systems that don’t recognize U.S. court orders. By setting up an OAPT in jurisdictions like the Cook Islands or Nevis, you effectively transfer legal ownership of your assets to a trust governed by the laws of a sovereign nation. This separation makes it nearly impossible for U.S. courts to enforce their rulings. These trusts are particularly useful in divorce cases, where courts may attempt to divide marital assets.

Unlike the 21 U.S. states that allow Domestic Asset Protection Trusts (DAPTs), offshore jurisdictions aren’t subject to the Full Faith and Credit Clause. For example, a divorce decree issued in California holds no weight in the Cook Islands. An ex-spouse can’t simply present a U.S. court order to claim assets – they would need to re-litigate the case under the local laws of the offshore jurisdiction. This process often requires a hefty litigation bond, typically ranging from $50,000 to $100,000, just to file a case.

How Offshore Trusts Work

An OAPT shifts legal ownership of your assets to a foreign trustee in a jurisdiction known for its protective laws. Usually, a licensed institutional trustee in these offshore locations manages the assets according to the terms of the trust deed. While you, as the settlor, can be named as a discretionary beneficiary, you no longer directly own the assets.

The trust deed includes protective mechanisms like anti-duress clauses, flight clauses, and the involvement of a Trust Protector.

- Anti-duress clauses: These prevent distributions if the trustee believes you’re acting under court pressure, supporting an "impossibility defense" in legal proceedings.

- Flight clauses: Allow the trustee to relocate the trust to another jurisdiction if legal threats arise.

- Trust Protector: This independent advisor has the authority to replace trustees, veto distributions, or even move the trust’s domicile to a safer location if necessary.

These features make offshore trusts a powerful tool for shielding assets from legal claims.

Legal Benefits of Offshore Trusts

Offshore trusts present significant hurdles for creditors, requiring stricter proof standards and offering shorter timeframes to challenge transfers. These protections are particularly effective against claims related to asset division and alimony in family court cases.

In the Cook Islands, creditors must prove fraudulent transfer beyond a reasonable doubt – the same standard used in criminal cases – unlike the lower preponderance of evidence standard in U.S. civil courts. Additionally, while U.S. fraudulent transfer claims can remain valid for several years, the Cook Islands generally limits the challenge period to one or two years from the transfer date. In Nevis, any charging orders against LLC interests held by the trust expire after three years and cannot be renewed.

Attorney Brian T. Bradley highlights the true test of these structures:

"The key question is never whether a structure looks impressive in an estate planning binder. The real question is whether it survives when a creditor’s attorney, a federal bankruptcy trustee, or a family-court judge attempts to enforce a judgment."

Ipanema Partners further emphasizes the strength of these trusts:

"No Cook Islands trust that was properly structured, adequately funded, and established before a legal claim arose has ever been successfully penetrated by a U.S. creditor."

Even in extreme cases, such as FTC v. Affordable Media (1999), where U.S. courts jailed settlors for contempt, Cook Islands trustees refused to comply with repatriation orders, ensuring the assets remained protected.

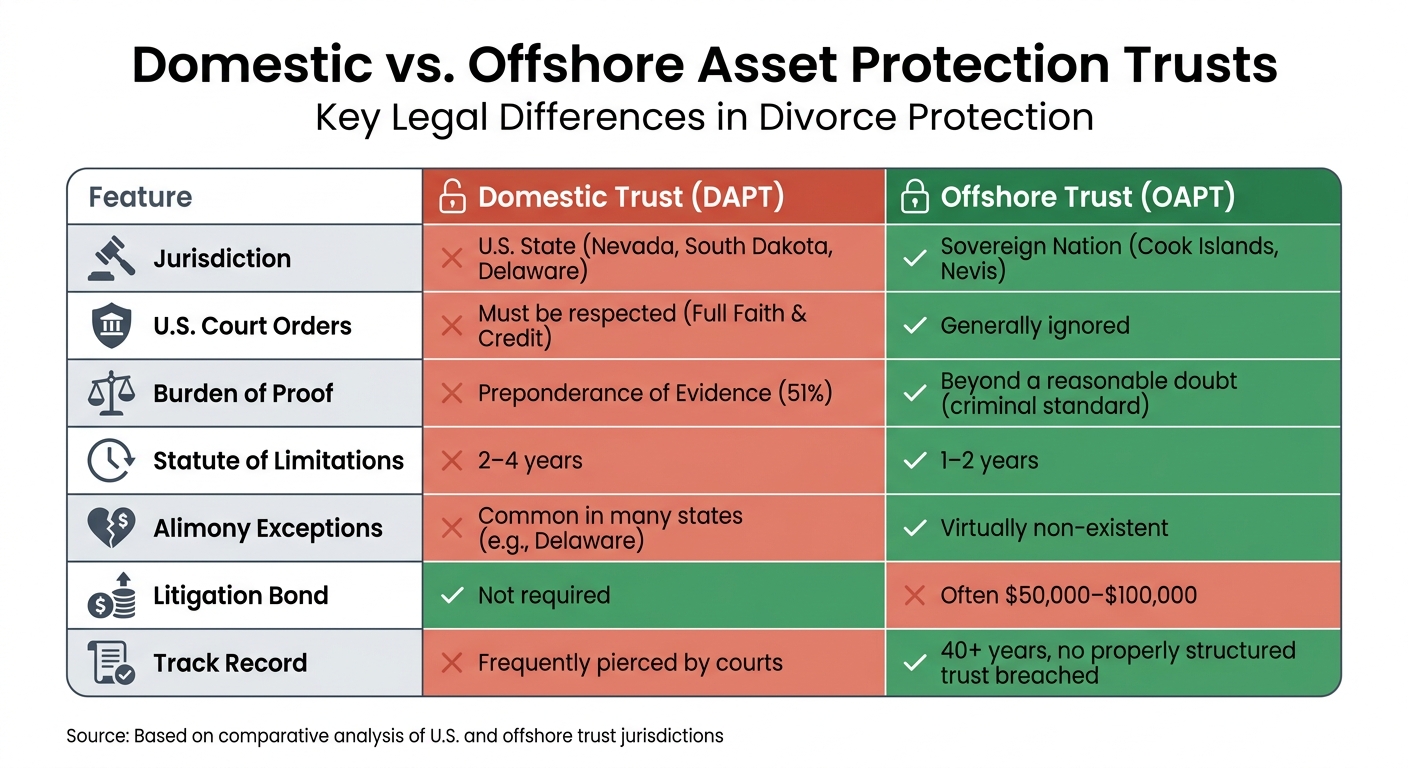

| Feature | Domestic Trust (DAPT) | Offshore Trust (OAPT) |

|---|---|---|

| Jurisdiction | U.S. State (Nevada, South Dakota, Delaware) | Sovereign Nation (Cook Islands, Nevis) |

| U.S. Court Orders | Must be respected (Full Faith & Credit) | Generally ignored |

| Burden of Proof | Preponderance of Evidence (51%) | Beyond a reasonable doubt (criminal standard) |

| Statute of Limitations | 2–4 years | 1–2 years |

| Alimony Exceptions | Common in many states (e.g., Delaware) | Virtually non-existent |

| Litigation Bond | Not required | Often $50,000–$100,000 |

For an offshore trust to be effective, it’s essential that you genuinely relinquish control. You can’t name yourself as trustee or retain unilateral power to fire the trustee. U.S. courts would interpret such actions as evidence that you still own the assets, undermining the trust’s protections.

Using Offshore LLCs to Protect Assets from Divorce

Offshore LLCs provide a practical way to safeguard your assets during divorce proceedings, combining asset separation with operational flexibility. Unlike offshore trusts, which rely on foreign trustees, offshore LLCs allow you to retain control while shielding your holdings from family court rulings. Since the LLC legally owns the assets, they are typically excluded from calculations for alimony or marital property settlements.

The main advantage lies in the jurisdictional immunity these LLCs offer. U.S. courts cannot force a foreign LLC to release funds or dissolve. Additionally, the structure of these entities relies on charging orders and separation of responsibilities, creating a robust barrier that makes it extremely difficult for an ex-spouse to access the assets without navigating the legal system of the offshore jurisdiction.

How Offshore LLCs Protect Your Assets

When you transfer assets into an offshore LLC, you create a legal boundary between yourself and the assets. The LLC takes ownership of properties, investment accounts, or business interests, leaving only your personal assets subject to divorce settlements.

Certain jurisdictions, like the Cook Islands and Nevis, offer powerful protections through charging order exclusivity. If a court issues a judgment, the creditor (such as an ex-spouse) is limited to a claim on potential distributions from the LLC. They cannot seize assets, force a sale, or interfere in the LLC’s operations. In Nevis, these charging orders automatically expire after three years.

Privacy is another key benefit. Jurisdictions such as the Cook Islands limit public disclosure to the company name and registered agent, making it harder for opposing legal teams to identify your protected assets. Moreover, many offshore LLCs include anti-duress provisions. If a court demands the repatriation of funds, the LLC manager – often an independent foreign trustee – can refuse on the grounds of duress. This creates an "impossibility defense", as U.S. courts lack authority over foreign managers.

Attorney Blake Harris emphasizes the strength of this jurisdictional barrier:

"Foreign jurisdictions don’t recognize U.S. court judgments, so to target your offshore LLC, a creditor would need to navigate the local legal system and face extensive costs."

To challenge the LLC, your ex-spouse must prove fraudulent intent beyond a reasonable doubt – a higher standard than the civil requirement of a preponderance of evidence. Additionally, the Cook Islands allows only one year to contest a transfer, while Nevis permits up to two years.

Best Jurisdictions for Offshore LLCs

Choosing the right jurisdiction is essential for maximizing the protection offered by your offshore LLC.

Cook Islands: Known for its strong legal framework, the Cook Islands has over 40 years of case law supporting its asset protection strategies. No properly structured trust or LLC from this jurisdiction has ever been successfully challenged by a U.S. creditor when set up before a legal claim. Fraudulent transfer claims require proof beyond a reasonable doubt, and foreign judgments are not recognized .

Nevis: Offering similar protections at a lower cost, Nevis stands out for its simpler administration. One of its unique features is the automatic three-year expiration of charging orders, which cannot be renewed. Creditors must also post a litigation bond before filing claims. The setup costs for a Nevis LLC typically range from $10,000 to $35,000, with annual maintenance fees between $5,000 and $10,000.

Belize: Belize takes a different approach by eliminating the statute of limitations for fraudulent transfer claims, protecting assets as soon as they are transferred. A U.S. Bankruptcy Court noted:

"Belize is a popular trust jurisdiction precisely because it allows the types of fraudulent transfers that are unenforceable in America".

Attorney Brian T. Bradley highlights the strengths of these jurisdictions:

"Nevis offers nearly identical statutory advantages at a lower cost and with easier administrative management, while the Cook Islands delivers unmatched historical precedent and courtroom-tested resilience."

Each of these jurisdictions aligns with the U.S. Internal Revenue Code, ensuring compliance with tax laws while maintaining asset protection. Offshore LLCs are tax-neutral, meaning they don’t change your U.S. tax obligations but must still be reported using forms like FBAR and Form 8858.

| Feature | Cook Islands | Nevis | Belize |

|---|---|---|---|

| Primary Strength | 40+ years of case law | Cost-effective; 3-year charging order limit | Immediate protection; no statute of limitations |

| Litigation Bond | ~$100,000 | Required | Varies |

| Burden of Proof | Beyond a reasonable doubt | Beyond a reasonable doubt | High statutory barrier |

| Foreign Judgments | Not recognized | Not recognized | Not recognized |

| Setup Cost Range | $25,000–$40,000 | $10,000–$35,000 | Not specified |

| Annual Maintenance | $5,000–$10,000 | $5,000–$10,000 | Not specified |

Timing is critical – these structures must be established before any divorce filing or foreseeable legal challenges to avoid fraudulent transfer claims.

Combining Offshore Trusts and LLCs for Maximum Protection

Pairing an offshore trust with an offshore LLC creates a layered defense system, offering strong legal safeguards. The LLC provides operational control and charging order protection, while the trust addresses risks like court-ordered asset transfers.

Here’s how it works: the setup separates ownership from control. You can act as the manager of the offshore LLC, overseeing daily operations, while the offshore trust serves as the sole owner. This structure acts as a legal shield. While U.S. judges can issue orders against you personally, foreign trustees are bound by the laws of their own jurisdiction, which often prevent compliance with U.S. court orders.

For example, if a family court demands that you repatriate assets during a divorce, anti-duress provisions in this combined structure ensure an additional layer of protection. This strengthens the separation between jurisdictions, making it harder for domestic courts to enforce such orders.

Attorney Brian T. Bradley highlights the importance of this approach:

"The layers are not redundant. They solve different legal problems."

How the Trust-LLC Structure Works

This structure offers dual protection: horizontal protection shields against business liabilities, while vertical protection guards personal assets from creditors, like an ex-spouse. To maximize its effectiveness, the trust should be irrevocable, and the trustee must have full discretion over distributions. If you retain the power to access funds directly, a judge could order you to exercise that power.

In some cases, an Asset Management Limited Partnership (AMLP) adds another layer of security. Here, the trust holds partnership interests while an offshore general partner manages operations. Alternatively, a "Bridge Trust" model starts as a foreign trust but operates domestically until a triggering event, like a divorce filing, shifts control fully offshore.

Real-World Examples of Multi-Entity Protection

The effectiveness of this strategy has been demonstrated in notable court cases. In FTC v. Affordable Media, LLC (1999), United States v. Grant (2011), and SEC v. Solow (2008), U.S. courts issued repatriation orders and held individuals in contempt. Yet, foreign trustees consistently refused to comply due to anti-duress clauses, maintaining jurisdictional separation.

These examples underscore the strength of combining a trust and LLC for asset protection, particularly during divorce proceedings. However, timing is critical – this structure must be established well in advance of any legal threats, and control must genuinely be handed over to an independent foreign trustee.

Best Jurisdictions for Divorce-Resistant Offshore Structures

Offshore jurisdictions differ in how effectively they protect assets during divorce, depending on their legal systems, procedural hurdles, and resistance to foreign court orders.

Three jurisdictions frequently stand out for their divorce-resistant asset protection: the Cook Islands, Nevis, and Belize.

Choosing the right jurisdiction is a critical step in ensuring your offshore structure can withstand divorce-related challenges, building on the layered protection strategies outlined earlier.

Jurisdiction Comparison Table

| Feature | Cook Islands | Nevis | Belize |

|---|---|---|---|

| Statute of Limitations | 1–2 years | 2 years | None (immediate protection) |

| Burden of Proof | Beyond reasonable doubt | Beyond reasonable doubt | N/A |

| Foreign Judgments Enforced | No | No | No |

| Bond Requirement | No | ~$100,000 | No |

| Litigation Track Record | Extensive (40+ years) | Moderate | Minimal |

| Setup Cost Range | $20,000–$25,000 | Moderate | Lowest |

| Annual Maintenance | $5,000–$8,000 | Similar to Cook Islands | Lower than Cook Islands |

| Ideal For | High-stakes protection | Cost-conscious protection | Immediate legal threat |

The Cook Islands is widely regarded as the top choice for offshore asset protection. Since 1984, no properly structured Cook Islands trust has ever been breached by a U.S. creditor. This jurisdiction’s legal framework requires creditors to prove fraudulent transfer beyond a reasonable doubt, a standard typically reserved for criminal cases. This makes it extraordinarily difficult for an ex-spouse to succeed in a civil dispute.

Nevis offers strong protections at a more moderate cost. One of its key features is the $100,000 cash bond requirement. Before filing a lawsuit against your trust, an ex-spouse must post this significant amount, creating both a financial and procedural barrier. Additionally, charging orders on LLC interests in Nevis expire after three years and cannot be renewed, further deterring litigation.

Belize stands out for providing immediate protection, as it has no statute of limitations for fraudulent transfer claims. This makes it a practical choice for those facing urgent legal threats. While Belize’s case law isn’t as established as the Cook Islands’, it remains a cost-effective and fast option for those working within tighter budgets.

What to Consider When Choosing a Jurisdiction

The right jurisdiction can make or break your offshore structure’s effectiveness. A key factor is the non-recognition of foreign judgments. Each of these jurisdictions refuses to enforce U.S. divorce decrees, forcing an ex-spouse to re-litigate the case offshore. This requires hiring local legal representation and navigating unfamiliar legal systems, adding significant challenges for the opposing party.

Trustee quality is another critical element. As attorney Gideon Alper explains:

"A well-managed, experienced trustee in a slightly less favorable jurisdiction will outperform a poorly managed trustee in the strongest statutory environment."

The Cook Islands, for example, has around nine licensed trustee companies regulated by its Financial Supervisory Commission, ensuring a deep pool of experienced professionals.

Political stability and regulatory consistency also matter. The Cook Islands and Nevis have decades of established legal frameworks, whereas Belize’s protections are newer and less tested. If you’re preparing for aggressive litigation from a resourceful ex-spouse, the Cook Islands’ long-standing reputation and reliability may justify the higher setup cost of $20,000 to $25,000.

Lastly, timing and cost are crucial. Offshore structures should be established before divorce becomes "foreseeable" to avoid fraudulent transfer claims. For those acting proactively with significant assets, the Cook Islands offers unmatched protection. On the other hand, if immediate protection or affordability is your priority, Belize is a faster and more budget-friendly option.

Setting Up Offshore Structures with Global Wealth Protection

Step-by-Step Setup Process

Global Wealth Protection uses its Bridge Trust® framework to establish offshore structures that remain tax-simple until a legal issue activates full offshore enforcement. The process kicks off with a consultation to evaluate your circumstances and determine whether pre-litigation planning is appropriate. If you choose to move forward, the trust is drafted under foreign law – most commonly the Cook Islands International Trusts Act 1984 – but operates as a domestic grantor trust for U.S. tax purposes in its initial phase. This setup allows you to bypass foreign reporting forms, such as Form 3520 or Form 3520-A, until the trust transitions to the offshore phase due to legal action.

The strategy includes asset layering. Economic interests are held by an Asset Management Limited Partnership, while operational assets – like real estate and business holdings – are managed through state-specific LLCs. This layered structure connects your domestic control with offshore legal protections, reinforcing the broader asset protection strategy.

If a court order in a divorce case demands the repatriation of assets, a Trust Protector can declare an "Event of Duress." At that point, your authority over the trust ends, and a pre-designated foreign Special Successor Trustee takes over, operating under foreign law. This creates an "impossibility defense", making it legally challenging to comply with U.S. court orders. This proactive structure integrates seamlessly with Global Wealth Protection’s asset protection approach for high-net-worth families.

Meeting U.S. and International Compliance Requirements

Once the structure is established, staying compliant is essential. In the initial phase, income flows directly to you as the trust’s settlor and is reported under IRC §§671-677. When the offshore phase is triggered, you must file Form 3520 (Annual Return To Report Transactions With Foreign Trusts) and Form 3520-A (Annual Information Return of Foreign Trust With a U.S. Owner) to meet U.S. tax requirements. These steps ensure compliance during both the domestic and offshore phases, aligning with the setup process.

It’s critical to establish and fund these structures well in advance of any foreseeable divorce. Under Bankruptcy Code §548(e), transfers into self-settled trusts within 10 years of bankruptcy can be voided if there’s evidence of intent to hinder creditors. In divorce cases, courts often scrutinize transfers made after marital discord begins, viewing them as potentially fraudulent if they appear intended to hide assets. This often raises questions regarding the morality of asset protection in legal disputes.

Costs for setting up these structures typically range from $10,000 to $100,000, with annual maintenance and trustee fees between $1,000 and $25,000. Global Wealth Protection offers consultations to help you navigate this process, ensuring your offshore structure is legally sound and capable of withstanding scrutiny in family court.

Avoiding Fraudulent Transfer Claims and Common Mistakes

Offshore asset protection works best when planned ahead and handled carefully, especially during a divorce. Timing and maintaining genuine independence are key to ensuring these structures can withstand legal challenges.

How to Avoid Fraudulent Transfer Claims

Timing is everything when it comes to offshore asset protection. Courts closely examine any transfers made after a legal threat becomes foreseeable – even if no lawsuit has been filed yet. In divorce cases, this means transfers made after marital discord begins are particularly vulnerable to being labeled fraudulent. As Brian T. Bradley, Esq. from Bradley Legal Corp explains:

"Asset protection is not unlawful simply because it makes collection more difficult. It becomes unlawful when it is implemented too late."

U.S. courts recognize two types of fraudulent transfer claims:

- Actual fraud: This involves proving that the transfer was made with the intent to hinder or defraud someone, like your spouse. Courts look for "badges of fraud", such as hurried transfers or moving assets to close relatives.

- Constructive fraud: Unlike actual fraud, this doesn’t require proof of intent. Transfers can be voided if they lack equivalent value and harm your ability to meet financial obligations.

The timeframes for challenging these transfers vary widely. Most U.S. states have a four-year lookback period under the Uniform Voidable Transactions Act. However, under Bankruptcy Code §548(e), trustees can void transfers into self-settled trusts made within 10 years if the intent to hinder creditors is proven. On the other hand, Nevis offers a much shorter two-year limit for such challenges.

To reduce the risk of fraudulent transfer claims, take these steps:

- Set up offshore structures well in advance – ideally years before any legal threats arise.

- Keep enough personal assets outside the structure to cover foreseeable debts and obligations.

- Transfer full control to an independent foreign trustee. Retaining too much control allows U.S. courts to compel repatriation through contempt sanctions.

- Document legitimate reasons for creating the trust, like estate planning or diversifying international holdings, to counter claims of fraudulent intent.

By addressing these risks early, you can build a stronger foundation for your asset protection strategy.

Common Offshore Planning Mistakes

Timing isn’t the only factor that can derail offshore asset protection. Several other common mistakes can leave your strategy exposed:

- Last-minute planning: Waiting until a legal threat is imminent is a recipe for failure. For example, in April 2026, a real estate investor named Michael transferred an $8 million portfolio into a trust just six weeks after facing a $4.2 million judgment. The court ruled the transfers were fraudulent and reversed them all.

- Retaining excessive control: Overstepping as a trustee or protector can backfire. In FTC v. Affordable Media, the defendants were jailed for civil contempt because they kept too much control over their Cook Islands trust. The court decided they could comply with a repatriation order, undermining the trust’s protection.

- Placing U.S. real estate in offshore trusts: This strategy often doesn’t work. In March 2026, the U.S. District Court for the Eastern District of California ruled in United States v. Huckaby that a Nevada Domestic Asset Protection Trust couldn’t shield real property located in California. The court applied California law instead of Nevada’s trust protections.

- Failing to disclose trust interests: Hiding trust assets during divorce or bankruptcy proceedings can lead to severe consequences, including denial of debt discharge or even criminal penalties.

- Ignoring tax obligations: Offshore trusts are not tax shelters. U.S. residents are taxed on worldwide income, and failing to comply with tax laws can result in hefty IRS penalties.

If you want to avoid these mistakes, it’s crucial to plan carefully, document everything, and follow all reporting requirements. Global Wealth Protection offers consultations to help you navigate these complexities and establish compliant, well-timed offshore structures.

Conclusion

Shielding wealth during divorce calls for a carefully planned offshore strategy. As Brian T. Bradley, Esq. wisely notes:

"You don’t rise to the level of your income. You fall to the level of your legal structure. And the legal structure has to exist before the stress arrives."

The strategies highlighted earlier emphasize combining Offshore Asset Protection Trusts with Offshore LLCs in jurisdictions like the Cook Islands or Nevis. These jurisdictions create a strong legal barrier that U.S. family courts struggle to penetrate. Over the past 30 years, properly structured offshore trusts have maintained a 96% success rate. For example, the Cook Islands boasts a 40-year history where no trust established before a claim arose has been breached by a U.S. creditor.

Timing is everything. Setting up these structures after marital issues arise can expose them to fraudulent transfer claims. Many U.S. states have lookback periods of about four years, while federal bankruptcy law extends this to 10 years . In contrast, the Cook Islands limits such claims to just one or two years.

A critical element of success is fully relinquishing control to an independent foreign trustee. Holding onto any form of backdoor control can lead to civil contempt charges and jeopardize the entire structure . Seeking professional advice ensures you avoid these risks and remain compliant with reporting requirements like FBAR, FATCA, and other IRS regulations.

Global Wealth Protection offers private consultations to help you create compliant offshore structures tailored to your needs. Acting early can save significant costs compared to addressing issues after they arise.

FAQs

Can an offshore trust still be treated as marital property?

Offshore trusts can sometimes be classified as marital property, depending on the specific laws of the jurisdiction and the unique circumstances of the case. That said, offshore asset protection strategies are often crafted to strengthen these trusts against claims in family court, making them more difficult to reach during divorce settlements.

How early is “early enough” to avoid a fraudulent transfer claim?

To steer clear of a fraudulent transfer claim, it’s crucial to make transfers before any claims or lawsuits are on the horizon. Courts often invalidate transfers made with the intent to obstruct creditors or those carried out after a claim has been filed or threatened. Taking action early and ensuring there’s no indication of intent to deceive is essential for the transfer to hold up legally.

What IRS forms do I need for an offshore trust or LLC?

U.S. individuals involved with offshore trusts or LLCs are generally required to file Form 3520. This form is used to report transactions with foreign trusts and any ownership interests. Additionally, if you own a foreign trust, you’ll need to file Form 3520-A to comply with IRS reporting rules. Accurate and timely submissions are crucial to avoid potential penalties.