Retiring abroad can offer wealthy Americans significant tax savings, lower living costs, and a better quality of life. While U.S. citizens must still report worldwide income to the IRS, choosing a country with favorable tax policies can reduce local tax burdens. Top destinations include Panama, Costa Rica, Malaysia, Greece, and Belize – each offering unique benefits like territorial tax systems, retiree visas, and affordable healthcare. Here’s a quick overview:

- Panama: No tax on foreign income, U.S. dollar-based economy, affordable living, and retiree discounts.

- Costa Rica: Tax-free foreign income, excellent healthcare, and a low $1,000/month income requirement.

- Malaysia: Exempts foreign income, low living costs, and modern amenities.

- Greece: 7% flat tax on foreign income for 15 years, EU access, and a Mediterranean lifestyle.

- Belize: No tax on foreign income, English-speaking, and a low cost of living.

These countries cater to different priorities – tax savings, lifestyle, or cost efficiency. Below is a quick comparison to help you decide.

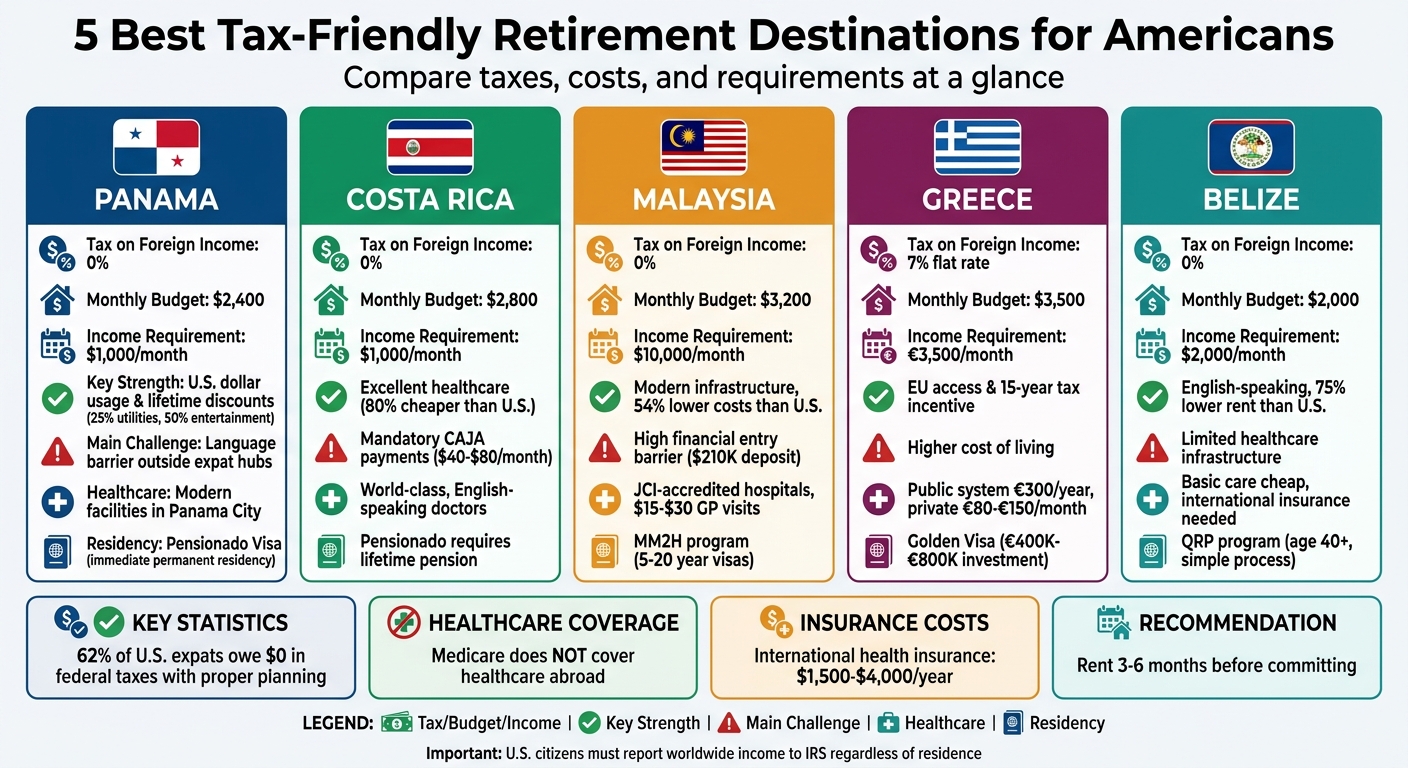

Quick Comparison

| Country | Tax on Foreign Income | Monthly Budget | Income Requirement | Key Strength | Main Limitation |

|---|---|---|---|---|---|

| Panama | 0% | $2,400 | $1,000/month | U.S. dollar usage & discounts | Language barrier outside hubs |

| Costa Rica | 0% | $2,800 | $1,000/month | High-quality healthcare | Mandatory healthcare payments |

| Malaysia | 0% | $3,200 | $10,000/month | Low cost, modern infrastructure | High financial entry barrier |

| Greece | 7% flat | $3,500 | €3,500/month | EU access & tax incentives | Higher cost of living |

| Belize | 0% | $2,000 | $2,000/month | English-speaking, low costs | Limited healthcare facilities |

Each destination offers unique benefits, but careful planning is essential to navigate U.S. tax rules, visa requirements, and local costs. Consider your financial situation and lifestyle preferences before making a move.

1. Panama

Panama has become a popular retirement destination for wealthy Americans, thanks to its pure territorial tax system, which only taxes income earned within the country. Any income from outside Panama is 100% exempt from local taxes. This means dividends, capital gains, interest, or profits from foreign sources are not subject to Panamanian taxation. Additionally, there are no wealth, gift, or inheritance taxes.

Tax Benefits

Panama’s territorial tax system can lead to significant savings. For example, earning $100,000 from U.S. investments results in 0% Panamanian tax liability. The country also has a relatively low VAT rate of 7%, much lower than Costa Rica’s 13%. If you do earn local income, it’s taxed progressively: the first $11,000 is exempt, income between $11,001 and $50,000 is taxed at 15%, and anything above $50,000 is taxed at 25%.

"Panama offers one of the most affordable retirement visas ($1,000/month pension) along with 0% tax on foreign income." – EnoughMoney.ai

However, as of March 2026, new economic substance requirements apply to multinational enterprise groups. If you’re earning foreign-source passive income through a Panamanian entity, you’ll need to establish genuine local operations – like hiring staff or leasing office space – to maintain your tax exemptions.

Residency Requirements

Panama provides several residency options tailored to retirees:

- The Pensionado Visa requires a $1,000 monthly lifetime pension and grants immediate permanent residency. It also includes legal discounts: 25% off utility bills, 50% off entertainment, 25% off airline tickets, and 20% off medical consultations and medications. If you invest $100,000 in Panamanian real estate, the required monthly pension drops to $750.

- The Friendly Nations Visa requires a $200,000 investment in real estate or a fixed-term bank deposit. It starts with a two-year provisional residency before applying for permanent status.

- The Qualified Investor Visa offers permanent residency within 30 to 45 days. The current investment requirement is $300,000 in unencumbered real estate, but this will rise to $500,000 after October 15, 2026. Government fees total $10,000, plus $1,000 per dependent.

| Visa Type | Minimum Investment/Income | Residency Status | Processing Duration |

|---|---|---|---|

| Pensionado | $1,000/month lifetime pension | Immediate Permanent | Moderate (months) |

| Friendly Nations | $200,000 (real estate or deposit) | 2-year provisional | Moderate (months) |

| Qualified Investor | $300,000 (real estate, until Oct 2026) | Immediate Permanent | 30–45 days |

Applications must be submitted through a Panamanian attorney while you’re in the country. Legal fees typically range from $1,500 to $4,000, but cutting corners can lead to rejection due to errors in paperwork. You’ll also need an apostilled criminal background check and proof of financial solvency.

Cost of Living

Panama’s affordability is another key draw. Monthly living costs in Panama City typically range from $1,200 to $1,770, while smaller towns like Boquete or David average around $900. The use of the U.S. dollar as the official currency eliminates exchange rate risks, simplifying financial planning for American retirees.

You can also import up to $10,000 in household goods and one new car duty-free every two years. However, opening a bank account can be tricky. Most banks require a temporary Cedula (ID card) and often reject non-residents or U.S. citizens due to FATCA compliance costs. Be prepared with at least two bank reference letters from your home country and professional references from your Panamanian attorney.

Quality of Life

Panama offers modern infrastructure, particularly in Panama City, which boasts advanced healthcare facilities, international schools, and a vibrant expat community. Its aviation hub, Tocumen International Airport, provides excellent connectivity across the Americas.

For asset protection, Panama offers options like the Private Interest Foundation (PIF), which shields assets from foreign judgments and bypasses probate. Many retirees pair this with a Sociedad Anónima (SA) for business operations.

Important Note: U.S. citizens remain subject to citizenship-based taxation, meaning they must report worldwide income to the IRS. While Panama doesn’t tax foreign income, this offers no foreign tax credits to offset U.S. tax obligations. Additionally, Panama generally doesn’t allow dual citizenship. Naturalization after five years requires renouncing U.S. citizenship, a step most retirees avoid.

sbb-itb-39d39a6

2. Costa Rica

Costa Rica offers an appealing package of tax incentives and residency options, making it a favorite among retirees looking for a tax-friendly destination. The country operates on a territorial tax system, meaning foreign-sourced income – like U.S. pensions, Social Security benefits, dividends, and investment returns – is completely exempt from local taxes. Additionally, there are no wealth or inheritance taxes.

Tax Benefits

Under Law 9996, retirees in the Pensionado, Rentista, and Inversionista categories enjoy several tax perks for 10 years after approval. These include a one-time full tax exemption on household goods imports and the ability to bring in up to two personal vehicles (land, air, or sea) without import duties. If you buy real estate during this period, you’ll also get a 20% discount on property transfer taxes.

Property taxes are incredibly low, just 0.25% of the registered value – much lower than in most U.S. states. For luxury properties valued above approximately ₡148 million in construction, rates range from 0.25% to 0.55%.

Other key taxes include a 13% VAT and a 15% capital gains tax, although assets held before July 1, 2019, may qualify for exemptions under certain conditions. Importantly, the income you declare for residency purposes is exempt from Costa Rican income tax.

Residency Requirements

Costa Rica provides three main residency pathways tailored for retirees:

- Pensionado: Requires a lifetime monthly pension of at least $1,000.

- Rentista: Requires proof of stable monthly income of $2,500 for at least two years.

- Inversionista: Requires an investment of $150,000 in real estate, shares, or productive projects (down from $200,000).

| Residency Category | Financial Requirement | Key Tax Benefit |

|---|---|---|

| Pensionado | $1,000/month lifetime pension | Income tax exemption on pension; additional benefits |

| Rentista | $2,500/month for 2 years | Exemptions on imports and foreign income |

| Inversionista | $150,000 investment | 20% property transfer tax discount; additional benefits |

To apply, you’ll need apostilled documents (e.g., birth certificates, criminal records) translated into Spanish and submitted to the Dirección General de Migración y Extranjería. Once approved, you must register fingerprints and join the Costa Rican social security system (CCSS). The process can take several months, and hiring an immigration lawyer can help avoid common pitfalls, such as incomplete documentation or missteps in choosing the right residency category.

"The biggest problems in residency cases usually come from incomplete documentation, expired certificates, weak legal strategy, or selecting the wrong category from the beginning." – Sergio Monge, Attorney at AG Legal

To qualify for Law 9996 benefits, applications must be submitted within the first five years of the law’s enactment.

Cost of Living

A retired couple can live comfortably in Costa Rica on $2,000 to $4,000 per month, depending on lifestyle. The average monthly budget for a comfortable lifestyle is around $2,800. Healthcare is a major savings area, with medical procedures costing up to 80% less than in the United States. Legal residents contribute 7% to 11% of their reported income to the public CAJA healthcare system, typically costing $40 to $80 per month. Many retirees also opt for private insurance, which ranges from $100 to $200 per month for faster access to English-speaking specialists.

Real estate prices vary widely. Rural homes start at about $65,000, while apartments near Central Pacific beaches begin around $70,000. Higher-end homes in areas like Guanacaste start at $115,000. For dining out, local meals (casados) cost between $5 and $8.

Quality of Life

Costa Rica offers more than just financial perks – it’s a haven for retirees seeking a relaxed and enriching lifestyle. Ranked as the third-best country to retire in 2026 by the Global Retirement Index, it boasts year-round temperatures of 70°F to 80°F in the Central Valley, eliminating the need for costly air conditioning. The Nicoya Peninsula, one of the world’s five Blue Zones, is known for its high concentration of centenarians, making it a draw for health-conscious individuals.

Over 30 municipalities, including Escazú and Santa Ana, are part of the WHO Age-Friendly Cities program, ensuring senior-friendly public spaces. Additionally, Costa Rica’s reliance on 99% renewable energy appeals to retirees with environmental priorities.

Important Note: While Costa Rica’s tax system is favorable, U.S. citizens must still report global income to the IRS. Consulting a tax professional can help you navigate potential U.S. tax benefits like the Foreign Earned Income Exclusion. For those considering long-term relocation, Costa Rica allows foreigners to apply for citizenship after seven years of residency, provided they spend at least six months per year in the country and pass a Spanish language test.

3. Malaysia

Malaysia is unique in Southeast Asia for maintaining its 1984 bilateral tax treaty with the United States, which provides protections not found elsewhere in the region. As Mike Wallace, CEO of Greenback Expat Tax Services, puts it: "It’s like living in the future at 1990s prices". The country combines modern amenities with affordability, making it an attractive destination for retirees.

Tax Benefits

Malaysia’s territorial tax system exempts U.S. pensions, Social Security benefits, dividends, and investment returns from taxation. There are no taxes on inheritance, estates, or gifts, and capital gains on stocks, bonds, and securities are tax-free. Even the interest earned on the Malaysia My Second Home (MM2H) program’s required fixed deposits is tax-exempt.

"Only income earned in Malaysia is taxed by the Malaysian government. Retirees will not pay Malaysian tax on capital gains, interest, dividends, pensions, or social security from outside Malaysia."

- Jean-François Harvey, Founder, Harvey Law Group

For those with more complex financial interests, the Labuan International Business and Financial Centre offers appealing options: a 3% tax rate on trading activities or a flat annual tax of RM 20,000. However, real estate sales are subject to Real Property Gains Tax (RPGT) – 30% if sold within the first five years, dropping to 10% after six years.

Residency Requirements

The MM2H program is the main pathway for retirees seeking long-term residency in Malaysia. This program offers renewable visas ranging from 5 to 20 years, depending on the tier chosen. Since its inception in 2002, over 30,000 applications have been approved. The Silver tier, for example, requires a fixed deposit of RM 1,000,000 (about $210,000), a monthly offshore income of RM 40,000 (around $8,000), and liquidity of RM 1,500,000. Higher tiers, such as Gold and Platinum, demand larger deposits but provide longer visa durations – 15 and 20 years, respectively.

| MM2H Tier | Fixed Deposit | Visa Validity | Monthly Income Required |

|---|---|---|---|

| Silver | RM 1,000,000 (~$210,000) | 5 Years (Renewable) | RM 40,000 (~$8,000) |

| Gold | RM 2,000,000 (~$450,000) | 15 Years | RM 40,000 (~$8,000) |

| Platinum | RM 5,000,000 (~$1.1M) | 20 Years | RM 40,000 (~$8,000) |

To maintain MM2H status, retirees must spend at least 90 days per year in Malaysia. After the first year, part of the fixed deposit can be used for property purchases, healthcare, or education. However, foreigners must meet minimum property purchase thresholds, which average RM 1,000,000 (approximately $210,000) but vary by state.

For U.S. citizens, banking in Malaysia can be tricky. Many local banks, like Maybank and Public Bank, avoid opening accounts for Americans due to the compliance costs associated with FATCA. Instead, international private banks such as HSBC Premier or Standard Chartered are often used, though they require minimum balances ranging from $100,000 to $1,000,000. Opting for the Gold or Platinum MM2H tiers may also help establish a strong "bona fide residence" for IRS purposes.

Cost of Living

Malaysia’s low cost of living is another major draw for retirees. A couple can live comfortably on $1,500–$2,200 per month, while a more upscale lifestyle in Kuala Lumpur costs around $3,200 monthly. Living costs in Malaysia are about 54% lower than in the United States, with rent alone being approximately 80% cheaper. For example, a 2-bedroom condo in Penang rents for $400–$700, while in Kuala Lumpur, similar units range from $500 to $900.

Healthcare is also affordable and of high quality. A general practitioner visit costs $15–$30, while specialist consultations range from $25 to $60. Major procedures, such as knee replacements, are priced between $4,000 and $7,000 – far less than the $30,000 to $50,000 typical in the U.S.. Many retirees opt for catastrophic-only international insurance while paying out-of-pocket for routine care due to the low costs.

Housing is another area where retirees can save significantly. A 1,000–1,200 sq ft home in Kuala Lumpur costs $220,000–$250,000, a fraction of what similar properties cost in New York. Dining is equally affordable, with meals at local hawker stalls costing $1–$3 and mid-range restaurant meals ranging from $5 to $15. High-speed internet (100 Mbps) is available for about $30 per month.

Quality of Life

Malaysia offers a high standard of living with modern infrastructure, including metro systems, shopping malls, and JCI-accredited private hospitals staffed by doctors trained in the U.K., U.S., or Australia. English is widely spoken, making daily life, legal matters, and healthcare access much easier.

The tropical climate keeps temperatures between 80°F and 92°F year-round, though the high humidity makes air conditioning essential. With over 15 national public holidays annually, Malaysia provides plenty of opportunities for leisure. Cities like Penang and Kuala Lumpur have also become hubs for medical tourism, offering excellent care at reasonable prices.

For retirees, Malaysia’s combination of tax advantages, affordable living, and quality infrastructure makes it a standout choice.

Important note: The current exemption for foreign income brought into Malaysia is valid until December 31, 2036. Before committing to purchasing property, it’s recommended to rent for 3 to 6 months in your preferred area.

4. Greece

Greece stands out as a prime destination for affluent American retirees, thanks to two tailored tax regimes designed to appeal to high-net-worth individuals. In 2025, the country welcomed 1,200 millionaires, securing its spot as the 8th most popular global choice for wealthy retirees. Much like Panama and Costa Rica, Greece combines attractive tax policies with the allure of a Mediterranean lifestyle.

Tax Benefits

Greece offers two streamlined tax options for retirees:

- 7% Pensioner Flat Tax: This program applies a flat 7% tax rate to all foreign-sourced income – covering pensions, dividends, interest, and rental income – for a period of 15 years. To qualify, retirees must have been non-residents for five of the previous six years and submit their application by March 31 of the relevant tax year.

- Non-Dom Investor Regime: This option imposes a flat annual tax of €100,000 on all worldwide foreign income, regardless of the total amount earned. According to Marc Cantavella, Manager at The Global Wealth:

"Greece has maintained its original €100,000 level, making it now three times cheaper than Italy".

Eligibility for this regime requires a €500,000 investment in Greek real estate, businesses, or securities. However, this requirement can be waived if the retiree already holds a Golden Visa. Additional family members can be included for €20,000 each per year.

Both programs last for 15 years. Under the Non-Dom regime, foreign assets are exempt from Greek inheritance and gift taxes. Retirees planning to work or start a business in Greece can also enjoy a 50% exemption on Greek-sourced income for up to seven years.

| Tax Regime | Eligibility Requirement | Duration | Tax on Foreign Income |

|---|---|---|---|

| 7% Pensioner Flat Tax | Non-resident for 5 of the past 6 years | 15 years | 7% flat rate |

| Non-Dom Regime | Non-resident for 7 of the past 8 years + €500K investment | 15 years | €100K flat annual fee |

Next, let’s look at the residency options that make these tax benefits accessible.

Residency Requirements

American retirees often secure residency in Greece through the Golden Visa program. This five-year renewable permit requires no minimum physical stay and grants full mobility across the Schengen Area. As of September 1, 2024, investment thresholds have been adjusted, ranging from €250,000 to €800,000 depending on location. Prime areas like Athens, Thessaloniki, Mykonos, and Santorini require a minimum investment of €800,000, while other regions require €400,000. The investment must be made in a single transaction to qualify.

Alternatively, the Financially Independent Person (FIP) permit is income-based, requiring a stable monthly income of at least $3,780 (approximately €3,500), with an additional 20% for a spouse and 15% for each child. While simpler, this permit prohibits local employment, unlike the Golden Visa, which offers more flexibility. Both options require private health insurance, typically costing between $65 and $270 per month (about €60–€250).

Before applying for residency, retirees need a Greek tax identification number (AFM) to handle banking, property transactions, and official filings. While residency doesn’t require year-round living in Greece, obtaining citizenship demands seven years of actual residence, physical presence, and proficiency in Greek.

Cost of Living

Greece offers a Mediterranean lifestyle upgrade at a fraction of the cost of living in the U.S. A monthly budget of about $3,500 can cover frequent island trips, private healthcare, and regular dining out – far more affordable than comparable living standards in major U.S. cities.

Dining out is a treat without breaking the bank. Meals at local tavernas range from $8.60 to $16.15 (€8–€15), and a bottle of local wine costs just $3.25 to $5.40 (€3–€5). Weekend getaways to Greece’s 227 inhabited islands are also affordable, with round-trip ferry tickets typically priced between $30 and $60.

Healthcare is another highlight. Access to the public system costs pensioners around $325 annually (roughly €300), while private insurance, which ensures faster access to English-speaking doctors, ranges from $86 to $162 per month (€80–€150). Many retirees pair private insurance for specialized care with the public system for routine needs.

Quality of Life

Greece blends ancient history with modern comforts. The country boasts over 200 archaeological museums, and 79% of users rate private healthcare staff as highly skilled. English is widely spoken in expat communities and by private medical professionals, making daily life and healthcare access easier for Americans.

With over 250 sunny days a year, Greece’s Mediterranean climate is a major draw. The traditional Greek diet – rich in olive oil, fresh vegetables, and seafood – is linked to health and longevity. The island of Ikaria, a "Blue Zone", is famous for its residents who frequently live past 100 years. For retirees seeking both financial advantages and an enriching lifestyle, Greece offers an unparalleled combination.

Important note: Wealthy retirees with annual foreign income exceeding $1.6 million (€1.5 million) should consider the Article 5A flat tax regime, which caps Greek tax liability at €100,000. U.S. expats are encouraged to coordinate their Greek tax residency with U.S. tax credits and treaty protections to avoid double taxation on worldwide income.

5. Belize

Switching gears from European sophistication to the laid-back vibe of Central America, Belize stands out as an attractive retirement destination. This English-speaking country combines ease of communication with a territorial tax system that exempts most foreign income – like pensions, dividends, interest, and capital gains – from local taxes. Additionally, Belize has no capital gains or inheritance taxes.

Tax Benefits

At the heart of Belize’s appeal is the Qualified Retirement Program (QRP). This program exempts retirees from all Belizean taxes on income earned outside the country. To qualify, you need to be at least 40 years old and show a monthly foreign income of at least US$2,000 (or US$24,000 annually). On top of this, the first BZD 29,000 of any income earned in Belize is also tax-free.

QRP participants enjoy some fantastic perks, including duty-free imports during their first year. This covers household goods, personal effects, a vehicle (renewable every three years), and even a boat or light aircraft. However, to keep your QRP status, you’ll need to spend at least 30 consecutive days in Belize every year.

One downside is Belize’s lack of a tax treaty or Social Security totalization agreement with the U.S., which can mean double Social Security contributions for self-employed expats. That said, the 2026 Foreign Earned Income Exclusion (FEIE) of up to US$132,900 could help reduce U.S. tax obligations. Belize’s currency, pegged to the U.S. dollar at a 2:1 ratio, further simplifies financial planning.

Residency Requirements

The process to join the QRP is refreshingly simple. It usually takes 1–2 months and doesn’t require language tests, interviews, or prior residency. As one source puts it:

"The Qualified Retirement Program (QRP) is typically the easiest and most cost-effective way to retire in Belize as an American".

The costs are straightforward: a US$1,000 QRP fee, a US$150 processing fee, and a US$200 certificate issuance fee, plus an annual renewal fee of US$50. Dependents add about US$1,100 each. After a year of legal residency, you can apply for permanent residency, and citizenship is an option after five years of permanent residence. Another route is temporary residency, which can be secured with a US$250,000 (500,000 BZD) investment. While QRP retirees typically don’t work locally, they can work online for foreign clients or manage offshore businesses.

Cost of Living

Belize offers outstanding affordability, with living costs about 31% lower than in the U.S., and rents averaging 75% less. A couple can live comfortably on US$1,500 to US$2,000 per month in many areas. For perspective, rent in Boston, MA, can be as much as 670% higher than in Belize City.

Housing costs depend on location. In central areas, a one-bedroom apartment averages US$481 per month, while three-bedroom units cost around US$784. In Belize City, you can find one-bedroom apartments for about US$300, and on Ambergris Caye, rents range from US$400 to US$2,000, depending on luxury. Property taxes are incredibly low, with a four-bedroom home incurring just US$100 to US$200 annually.

Dining and utilities are also budget-friendly. A mid-range meal for two costs around US$28 in Belize City and US$60 on Ambergris Caye. Basic utilities average US$88 per month, and gas is approximately US$7 per gallon. While day-to-day healthcare is inexpensive – hernia surgery costs under US$2,500 – retirees are advised to maintain international health insurance with medical evacuation coverage for serious conditions.

Quality of Life

Belize’s status as the only English-speaking country in Central America eliminates language barriers for expats. This makes navigating healthcare, banking, and legal matters much easier.

However, infrastructure can be inconsistent in some areas, with unreliable power and water supplies. Many residents invest in backup generators and water storage solutions. Safety is another consideration, as the U.S. State Department has a Level 2 travel advisory for Belize, recommending increased caution due to crime in certain areas, particularly parts of Belize City.

Belize also offers strong financial privacy. Bank account details can only be disclosed with a court order tied to criminal investigations. As Investopedia notes:

"Belize is a tax haven in the purest sense. Incorporating offshore companies is totally legal and is fairly simple in Belize".

These benefits make Belize a compelling option for retirees focused on wealth preservation. However, U.S. citizens must continue filing Form 1040 and reporting worldwide income to the IRS, along with filing an FBAR (FinCEN Form 114) if foreign account balances exceed US$10,000, to avoid hefty penalties.

Advantages and Disadvantages

Every destination comes with its own perks and challenges, making it vital to weigh the options carefully. For example, Panama stands out with its use of the U.S. dollar and attractive expat benefits through the Pensionado program, which offers lifetime discounts on various services. Costa Rica has a low monthly income requirement of $1,000, though retirees must make modest healthcare contributions ranging from $40 to $80 per month.

Malaysia, on the other hand, sets the bar higher, requiring retirees over 50 to have $10,000 in monthly offshore income and at least $400,000 in liquid assets to qualify for residency. Greece offers a straightforward 7% flat tax on foreign income for up to 15 years, as Reid Kopald, Tax Manager at Taxes for Expats, explains:

"Greece continues to offer one of the simplest paths for predictable tax planning… a 7% flat tax on all foreign source income for up to 15 years".

However, Greece’s cost of living is higher, with retirees needing approximately $3,500 per month and a minimum income requirement of €3,500.

Belize is the most budget-friendly option, with a monthly cost of around $2,000. It also offers the advantage of being fully English-speaking. However, its healthcare infrastructure is limited, making international health insurance a necessity.

Here’s a quick breakdown of key factors across these destinations:

| Country | Tax on Foreign Pension | Monthly Budget | Income Requirement | Key Strength | Main Limitation |

|---|---|---|---|---|---|

| Panama | 0% | $2,400 | $1,000/month | U.S. dollar usage & lifetime discounts | Language barrier outside expat hubs |

| Costa Rica | 0% | $2,800 | $1,000/month | High-quality healthcare | Mandatory CAJA contributions |

| Malaysia | 0% (passive) | $3,200 | $10,000/month | Modern infrastructure & English usage | High financial entry requirements |

| Greece | 7% flat | $3,500 | €3,500/month | EU access & 15-year tax incentive | Higher cost of living |

| Belize | 0% | $2,000 | $2,000/month | English-speaking & Caribbean lifestyle | Limited healthcare facilities |

Beyond these direct comparisons, currency stability plays a big role. Greece and Malaysia, for instance, face potential euro and ringgit volatility, which can reduce purchasing power by 10–20% during unstable economic periods. Panama avoids this risk entirely, thanks to its reliance on the U.S. dollar.

Finally, U.S. retirees often benefit from careful tax planning. According to IRS Taxpayer Advocate data, 62% of expats owe $0 in U.S. taxes, a figure that rises even more for retirees who structure their income effectively.

Conclusion

Choosing the ideal retirement destination depends on what matters most to you. If avoiding taxes and sticking with the U.S. dollar are top priorities, Panama stands out with its 0% tax on foreign income. For those drawn to a Mediterranean way of life and straightforward tax policies, Greece offers a 7% flat tax for 15 years. On the other hand, Costa Rica combines excellent healthcare, stunning natural surroundings, and territorial taxation – a great mix for retirees who prioritize quality living alongside financial perks.

Each country’s tax benefits, from Panama’s dollar-based economy to Greece’s flat-tax system, show how important it is to align your financial goals with your retirement plans. Thoughtful tax strategies can lead to substantial federal tax savings for U.S. expats, but these savings depend on understanding the interaction between U.S. citizenship-based taxation and your destination’s tax rules. As Reid Kopald, EA and Tax Manager at Taxes for Expats, explains:

"Choosing among the best tax-friendly countries to retire takes more than comparing headline tax rates. For Americans, the real question is how local taxes, US filing rules, healthcare, and visa options work together in practice".

To make the most of these opportunities, planning is key. Spend 3–6 months in your chosen country to experience its climate, culture, and daily life firsthand. Consult with an international tax advisor at least three years before your move to navigate exit taxes, pension treaties, and income structuring for optimal results. Since Medicare doesn’t cover healthcare abroad, plan to spend between $1,500 and $4,000 annually on private international health insurance for a healthy retiree.

The perfect retirement spot is out there for your financial and lifestyle needs. With careful preparation, expert advice, and realistic expectations, you can enjoy the rewards – and meet the challenges – of retiring abroad.

FAQs

Will I still owe U.S. taxes if I retire abroad?

As a U.S. citizen, you’re required to file income tax returns and pay U.S. taxes no matter where you retire – even if you’re living overseas. However, there’s some good news: certain countries have tax treaties or systems in place that might help lower your overall tax liability.

It’s worth researching these agreements and options as part of your retirement planning if you’re considering living abroad. They could make a big difference in how much you owe.

Which visa option is easiest for Americans to retire overseas?

Retiring abroad can be a dream for many Americans, and the simplest way to make it a reality is often through a retirement or long-term residence visa. These visas are tailored specifically for retirees and come with relatively straightforward requirements. Countries like Panama, Costa Rica, and Thailand are popular choices because of their retiree-friendly programs.

For instance, Panama’s Pensionado visa is widely recognized for its ease of access and benefits. Similarly, Costa Rica offers its own Pensionado program, which is equally appealing to retirees. Generally, these programs require proof of a stable income, health insurance coverage, and a clean background check – making the process manageable for most applicants.

How do I choose between low taxes and good healthcare?

Choosing between low taxes and quality healthcare is all about what matters most to you and your specific situation. Some countries, like Panama or Costa Rica, attract retirees with enticing tax breaks. However, the quality of healthcare in these destinations can differ significantly.

The key is to weigh a country’s healthcare system against its tax advantages. Are you willing to trade lower taxes for potentially less comprehensive medical care? Or do you prioritize top-notch healthcare, even if it means paying higher taxes?

To make the best decision, consider consulting a financial advisor. They can help create a retirement plan that aligns with your personal priorities and financial goals.