Think living the digital nomad life means escaping taxes? Think again. The idea of being "tax resident nowhere" is a myth that can lead to costly mistakes. Even if you move frequently and avoid spending 183 days in one country, you may still face tax obligations. Here’s why:

- Understanding Tax Residency Isn’t Just About Days: Many countries consider factors like bank accounts, rental agreements, or family ties – not just time spent there.

- U.S. Citizens Have No Escape: The U.S. taxes its citizens on worldwide income, no matter where they live.

- Double Taxation Risks: Without proper planning, you might owe taxes in multiple countries.

- Common Nomad Mistakes: Missing tax filings, failing to track location data, or not separating personal and business finances can trigger penalties.

The good news? You can reduce your tax burden legally by setting up residency in low-tax countries, leveraging tools like the Foreign Earned Income Exclusion, or structuring your income through U.S. LLCs or S-Corps. But it takes careful planning and compliance to avoid pitfalls.

Your freedom to work globally doesn’t mean freedom from taxes. Stay informed, stay compliant, and plan ahead to avoid financial headaches.

How Tax Residency Rules Work and How Countries Enforce Them

Tax residency rules differ widely between countries and often overlap, which can create challenges for nomads trying to navigate multiple systems. To avoid costly tax issues, it’s essential to understand how governments determine tax residency and enforce these rules. Let’s explore some of the key methods countries use, starting with the often-misunderstood 183-day rule.

The 183-Day Rule Explained

The 183-day rule is one of the most well-known standards for establishing tax residency, but it’s frequently misunderstood. The basic premise is simple: if you spend more than 183 days in a country, you’re likely considered a tax resident. Countries like the UK, Spain, Portugal, Russia, and the UAE follow this rule.

However, the 183-day rule is rarely the sole determinant of tax residency. In some cases, it’s not even part of a country’s domestic law. For instance:

- In the Netherlands, tax residency is assessed based on "durable ties" and where your life is primarily centered, not just the number of days you spend there.

- France uses a concept called "foyer", meaning that maintaining a household in the country can establish tax residency, regardless of how many days you’re physically present.

The UK’s Statutory Residence Test is even stricter. If you have four specific ties to the UK, you could become a tax resident in as few as 16 days. Switzerland, on the other hand, considers you a resident after 30 days if you’re working or 90 days if you’re not. In Germany, tax residency kicks in after six months of physical presence, whether those months fall within the same calendar year or span two years.

In short, staying under 183 days in every country doesn’t guarantee you’ll avoid tax residency. Many jurisdictions look at additional factors beyond just the number of days spent there.

Tiebreaker Rules in Tax Treaties

When two countries both claim you as a tax resident, tax treaties can help resolve the conflict. Most treaties follow the OECD Model Tax Convention, which uses a hierarchical tiebreaker test to decide which country has primary taxing rights.

Here’s how the tiebreaker process usually works:

- Permanent Home: The country where you maintain a dwelling for continuous use.

- Center of Vital Interests: The place where your strongest personal and economic ties – like family, social connections, and business activities – are located.

- Habitual Abode: The country where you spend the most time.

- Nationality: Your country of citizenship.

- Mutual Agreement: If none of the above resolve the issue, tax authorities from both countries negotiate a resolution.

These criteria determine which country gets the primary right to tax you. However, tax treaties only come into play if both countries claim you as a resident under their domestic laws. If only one country considers you a resident, no treaty conflict exists, and the treaty doesn’t apply. As dual.tax explains:

"The tie-breaker cascade only applies when both countries claim you as resident. If only one country’s domestic law makes you resident, there is no conflict to resolve – the treaty doesn’t override a country that doesn’t claim you".

Even if a treaty establishes your residency in one country, the other country may still tax certain types of income, such as rental income, employment income, or dividends. Many treaties cap dividend withholding taxes at 15%.

US Citizenship-Based Taxation

For most people, tax treaties help resolve residency disputes. But if you’re a U.S. citizen or Green Card holder, the situation is different. The United States taxes its citizens based on citizenship rather than residency, meaning you owe U.S. taxes on your worldwide income no matter where you live.

Most U.S. tax treaties include a "saving clause", which allows the U.S. to tax its citizens as if the treaty didn’t exist. This means treaty tiebreaker rules that might protect a French or German citizen from dual taxation don’t apply to Americans. The U.S. retains the right to tax its citizens regardless of where they reside.

Additionally, U.S. citizens face extra reporting requirements. For example, if your foreign bank accounts total more than $10,000 at any point during the year, you must file an FBAR (FinCEN Form 114).

The only way to escape U.S. citizenship-based taxation is by renouncing your citizenship, a process that comes with significant costs and complexities.

sbb-itb-39d39a6

Common Mistakes Digital Nomads Make

Digital nomads often stumble into tax troubles due to poor planning and simple oversights. Recognizing these common mistakes can help you sidestep unexpected penalties and liabilities.

Banking and CRS Reporting Problems

One of the most frequent missteps involves failing to disclose foreign bank accounts. If you’re a U.S. citizen and your foreign accounts exceed $10,000 at any point during the year, you must report them through the Report of Foreign Bank and Financial Accounts (FBAR). Additionally, the Foreign Account Tax Compliance Act (FATCA) requires you to report foreign financial assets above specific thresholds using Form 8938. Skipping these filings can lead to hefty fines.

Another common issue? Mixing personal and business finances. Using the same bank account or credit card for both personal and business expenses makes it harder to track deductible expenses. This lack of clarity can also raise red flags during audits. For self-employed nomads, this is especially critical since they face a 15.3% self-employment tax on top of their regular income tax. Proper expense tracking is key to reducing your overall tax load.

Missing quarterly estimated tax payments is another frequent error. Unlike traditional employees, who have taxes automatically withheld, self-employed individuals need to calculate and pay estimated taxes four times a year. Missing these deadlines can result in a 20% penalty plus interest.

Perhaps the most overlooked mistake is failing to document your location data. Without a detailed log of where you are each day, it becomes challenging to dispute tax residency claims. States like New York and California, for instance, may continue taxing your income based on factors like an employer’s location or ties such as a driver’s license or property – even if you’re working abroad.

Beyond these reporting missteps, neglecting digital nomad taxes can leave you vulnerable to double taxation.

Double Taxation from Poor Planning

Tax residency rules can be tricky, and poor planning often leads to double taxation. This happens when digital nomads fail to clearly establish tax residency in one specific location. As Lucky Nomads explains:

"The 183-day threshold is one criterion in a multi-factor test, not a binary switch that turns tax residency on or off".

Residual residency is another common trap. If you don’t formally establish a new tax home, your previous country may still consider you a resident. For example, keeping a registered address at your parents’ home, maintaining business registrations, or using a home-country bank account for daily transactions can create “economic links” that tax authorities use to justify residency claims. As Cruz notes:

"Some nomads don’t realize they may owe taxes in both the U.S. and a foreign country if they don’t properly claim treaty benefits or use the foreign earned income exclusion or foreign tax credit".

For U.S. citizens, the situation is even more complicated. The U.S. taxes worldwide income, no matter where you live. Tax treaties won’t exempt you from this obligation. Without claiming the Foreign Earned Income Exclusion (FEIE) or Foreign Tax Credits, you could end up paying full taxes in both the U.S. and your country of residence. In some cases, failing to sever ties with high-tax countries like France could leave you with a tax burden of 30–45%, including social contributions.

To avoid these pitfalls, you need to take deliberate steps. Start by formally cutting ties with your home country – this includes deregistering, canceling local health insurance, ending leases, and filing official departure notifications with tax authorities. At the same time, establish a new tax home by securing a long-term lease, opening a local bank account for daily expenses, and obtaining a local tax identification number. As Lucky Nomads points out:

"Tax residency is not determined by what you declare, but by what you can substantiate".

How to Legally Reduce Your Tax Burden

Now that the potential pitfalls have been outlined, it’s time to focus on actionable steps to legally reduce your tax liability. The cornerstone of this approach is establishing a clear and compliant residency in a jurisdiction that matches your financial and lifestyle needs.

Setting Up Residency in Low-Tax Countries

One effective way to avoid dual tax residency issues is to establish a tax base in a low-tax country. For instance, Paraguay operates on a territorial tax system, meaning only income earned within its borders is taxed, while foreign-sourced income is entirely exempt. Setting up residency typically involves legal fees ranging from $2,000 to $4,000, plus a $5,500 bank deposit.

Cyprus offers another appealing option with its 60-day rule. Unlike the usual 183-day requirement, Cyprus allows tax residency with just 60 days of physical presence, provided you aren’t a tax resident elsewhere and maintain a home or business locally. Non-domiciled residents enjoy 0% tax on foreign income for up to 17 years, making it a great choice for global investors and entrepreneurs.

For freelancers and consultants, Georgia provides a compelling tax structure. By registering under the "Individual Entrepreneur" status, you pay just 1% tax on gross revenue up to 500,000 GEL (about $180,000). This straightforward system eliminates the need for complex deductions and simplifies tax planning.

To make your residency legitimate, take steps to create "substance." This includes signing a long-term lease, opening a local bank account, obtaining a Tax Identification Number (TIN), and filing at least one tax return – even if it shows no income. These actions help establish an audit trail, proving that you’ve genuinely relocated.

Using the Foreign Earned Income Exclusion (FEIE)

For U.S. citizens, the Foreign Earned Income Exclusion (FEIE) is a powerful tool. By 2026, you can exclude up to $132,900 of foreign-earned income from U.S. federal income tax. This applies to wages, salaries, and professional fees, but not to passive income like dividends or capital gains.

To qualify, you must meet either the Physical Presence Test or the Bona Fide Residence Test:

- The Physical Presence Test requires you to spend at least 330 full days outside the U.S. during a 12-month period.

- The Bona Fide Residence Test involves establishing legal residence in a foreign country for an uninterrupted tax year.

Take Rachel, for example. She’s a U.S. citizen working remotely for a U.S. startup, earning $120,000 annually. By spending over 330 days outside the U.S. in 2025/2026, she qualified for the FEIE under the Physical Presence Test. After filing Form 2555, she excluded her entire salary, resulting in $0 U.S. federal income tax.

Important caveat: While the FEIE reduces federal income tax, it doesn’t eliminate the 15.3% self-employment tax on net earnings. For instance, a self-employed individual earning $130,000 abroad might owe around $19,890 in self-employment tax.

Additionally, you can claim the Foreign Housing Exclusion to deduct housing costs (like rent and utilities) exceeding a base amount of approximately $17,290. This is particularly helpful if you’re living in high-cost cities abroad.

Keep a meticulous travel log to document every day spent inside and outside the U.S. This is critical for proving eligibility during an audit. Also, avoid maintaining a "tax abode" in the U.S., as the IRS may disqualify your FEIE claim if you keep strong ties to the U.S. while living abroad.

Using Private US LLCs for Tax Benefits

For digital nomads earning more than $50,000–$60,000 annually, forming a U.S. LLC and electing S Corporation (S-Corp) status can help reduce the 15.3% self-employment tax. This strategy works by splitting your income into two parts: a "reasonable salary" subject to self-employment tax and distributions that are not.

Take James, a marketing consultant earning $100,000 while living in Thailand. By forming a U.S. S-Corp and paying himself a $50,000 salary, he reduced his self-employment tax to about $7,650, saving over $7,500 compared to operating as a sole proprietor.

An S-Corp also offers legal protection by separating personal assets from business liabilities. However, the IRS requires you to pay yourself a "reasonable salary" for the work you perform. Lowballing this figure to avoid taxes may trigger scrutiny.

Key note: Single-member LLCs are taxed as sole proprietorships by default, so the FEIE won’t reduce your self-employment tax unless you actively elect S-Corp status.

If you’re working in one of the 30+ countries with a U.S. totalization agreement (e.g., the UK, Germany, or France), you can obtain a Certificate of Coverage to avoid paying double social security taxes. This can save you thousands annually.

Offshore Company Formation for International Income

For those with international income, offshore companies can provide tax efficiency and ensure compliance with local laws. For example, forming a company in Anguilla or similar jurisdictions can help streamline income management while offering privacy.

However, U.S. citizens face strict reporting rules. If you control a foreign corporation, you must file Form 5471 for Controlled Foreign Corporations (CFCs). Certain passive income types may be subject to Subpart F or GILTI (Global Intangible Low-Taxed Income) taxes, even if profits aren’t distributed.

A major risk is creating a Permanent Establishment (PE) in the country where you’re working. For instance, managing your offshore company from a home office in Portugal or Thailand could lead local authorities to claim your company has a "taxable presence", triggering corporate taxes and VAT obligations. As of November 2025, the OECD introduced a 50% working-time benchmark to determine if remote work creates a "fixed place of business", meaning spending over half your working time in one country could unintentionally create a PE.

Consult a tax expert familiar with both U.S. and local regulations before setting up an offshore company. Mistakes in this area can be costly, as Forbes Finance Council warns:

"The mistakes founders make abroad tend to be structural, difficult to unwind, and more expensive than a missed deadline".

For many digital nomads, combining a low-tax residency (like Paraguay or Georgia) with a U.S. LLC or S-Corp strikes the best balance between simplicity, tax savings, and compliance – without the added complexity of offshore structures.

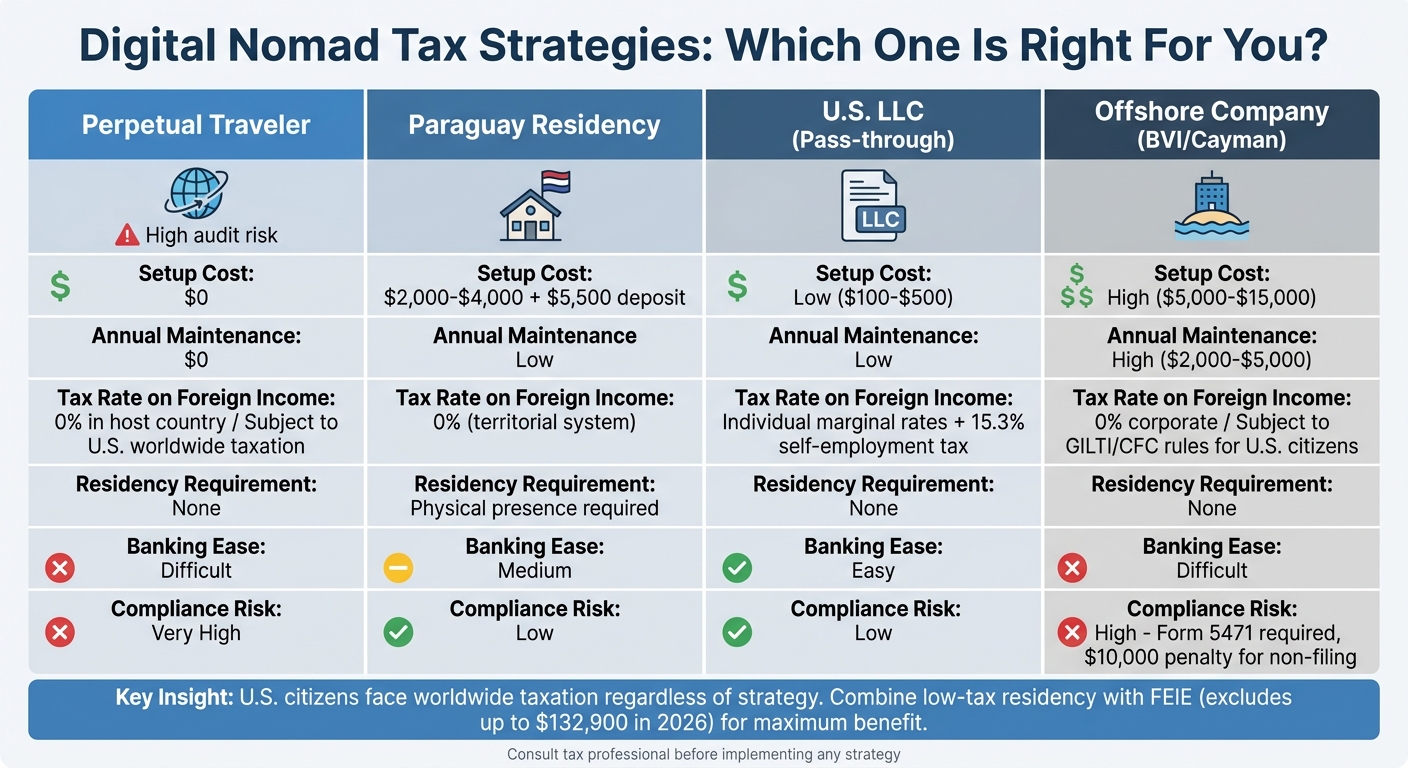

Comparison Table: Nomad Tax Strategies

Strategy Comparison: Key Metrics

When it comes to picking the right tax strategy, factors like your income, travel habits, and how much complexity you’re willing to deal with all come into play. Here’s a quick look at how the main options stack up:

| Strategy | Setup Cost | Annual Maintenance | Tax Rate on Foreign Income | Residency Requirement | Banking Ease |

|---|---|---|---|---|---|

| Perpetual Traveler | None | None | 0% (in host country) / subject to U.S. worldwide | None | Difficult |

| Paraguay Residency | Moderate | Low | 0% (territorial) | Requires physical presence | Medium |

| U.S. LLC (Pass-through) | Low | Low | Taxed at individual marginal rates | None | Easy |

| Offshore Company (BVI/Cayman) | High | High | 0% (corporate) / prone to U.S. tax implications (GILTI/CFC) | None | Difficult |

Breaking Down the Strategies

- Perpetual Traveler: This strategy has no upfront cost but comes with significant risks. Without a defined tax home, U.S. authorities might question your eligibility for the Foreign Earned Income Exclusion (FEIE). On top of that, opening and maintaining bank accounts can be tricky since most banks require a permanent address.

- U.S. LLC (Pass-through): For those earning below the FEIE threshold, a U.S. LLC can be a cost-effective choice. It simplifies banking and compliance, but you’ll still face the 15.3% self-employment tax unless you’re in a country with a totalization agreement.

- Paraguay Residency: This is a solid option for non-U.S. citizens or anyone looking for a territorial tax system where foreign income is exempt. While the setup costs are moderate, you’ll need to spend time in Paraguay to establish genuine residency.

- Offshore Companies: These can help with tax deferral but come with high setup and maintenance costs. For U.S. citizens, the compliance burden is significant, especially with Form 5471, which can take days to complete and carries a $10,000 penalty for non-filing. Banking can also be a headache due to the perceived risks associated with offshore entities.

Choosing the right strategy means weighing the costs, compliance requirements, and how well each option aligns with your income and lifestyle – all while staying within legal boundaries.

Conclusion

Living a nomadic lifestyle brings unparalleled freedom, but it also comes with the responsibility of managing tax obligations, no matter where you roam. Many digital nomads underestimate how complex it can be to navigate the tax rules of multiple jurisdictions, often leading to unintentional dual tax residency.

Tax authorities rely on various methods to determine your obligations – whether it’s the 183-day rule, the center of vital interests test, or, for U.S. citizens, taxation based on citizenship. Without careful planning, you could end up facing double taxation or even rigorous state audits. For example, New York conducts over 3,500 residency audits every year, reflecting how serious these matters can get. The belief that constant movement exempts you from taxes is a costly misconception that could lead to significant penalties.

To avoid these pitfalls, meticulous planning is key. Establishing a low-tax residency and leveraging tools like the Foreign Earned Income Exclusion (FEIE) – which allows you to exclude almost $130,000 of foreign-earned income in 2026 – can make a significant difference. Setting up a U.S. LLC might also be a smart move, depending on your circumstances. Over time, the difference between well-structured tax planning and neglecting these details can easily amount to six-figure savings.

The nomadic lifestyle is rewarding, but it requires financial discipline and strict compliance with international tax laws. Keep detailed records, separate personal and business finances, and seek advice from professionals with expertise in global tax issues. The aim isn’t to avoid taxes but to organize your finances in a way that ensures you only pay what’s legally required – no more, no less.

Your freedom to live and work anywhere shouldn’t jeopardize your financial stability. With the right strategies, you can embrace the global lifestyle you dream of while staying compliant and minimizing your tax liabilities within the boundaries of the law.

FAQs

What proof do I need to show where I’m a tax resident?

To figure out your tax residency status, you need to provide proof of where your strongest personal and financial connections lie. This could include details like where your family resides, where you earn the majority of your income, or the location of your permanent home. Authorities usually rely on these factors when determining your tax residency.

How can I stop my home state from taxing me while I’m abroad?

To prevent your home state from taxing you while you’re abroad, you need to establish a new domicile in a state with low or no income tax, such as Florida. This involves showing a legitimate change of residence by taking these steps:

- Physically moving to the new state and severing connections with your previous state.

- Proving your intent by updating things like your driver’s license, voter registration, and other official records.

- Maintaining thorough records to back up your move in case of an audit.

When does remote work create a “permanent establishment” for my company?

A permanent establishment can arise when a company maintains a fixed place of business in a foreign country, like an office or another site where significant activities take place. However, remote work by itself doesn’t automatically lead to this unless certain conditions are met under local laws or tax treaties. These conditions typically depend on the type of activities being carried out and whether they happen at a specific, stable location.