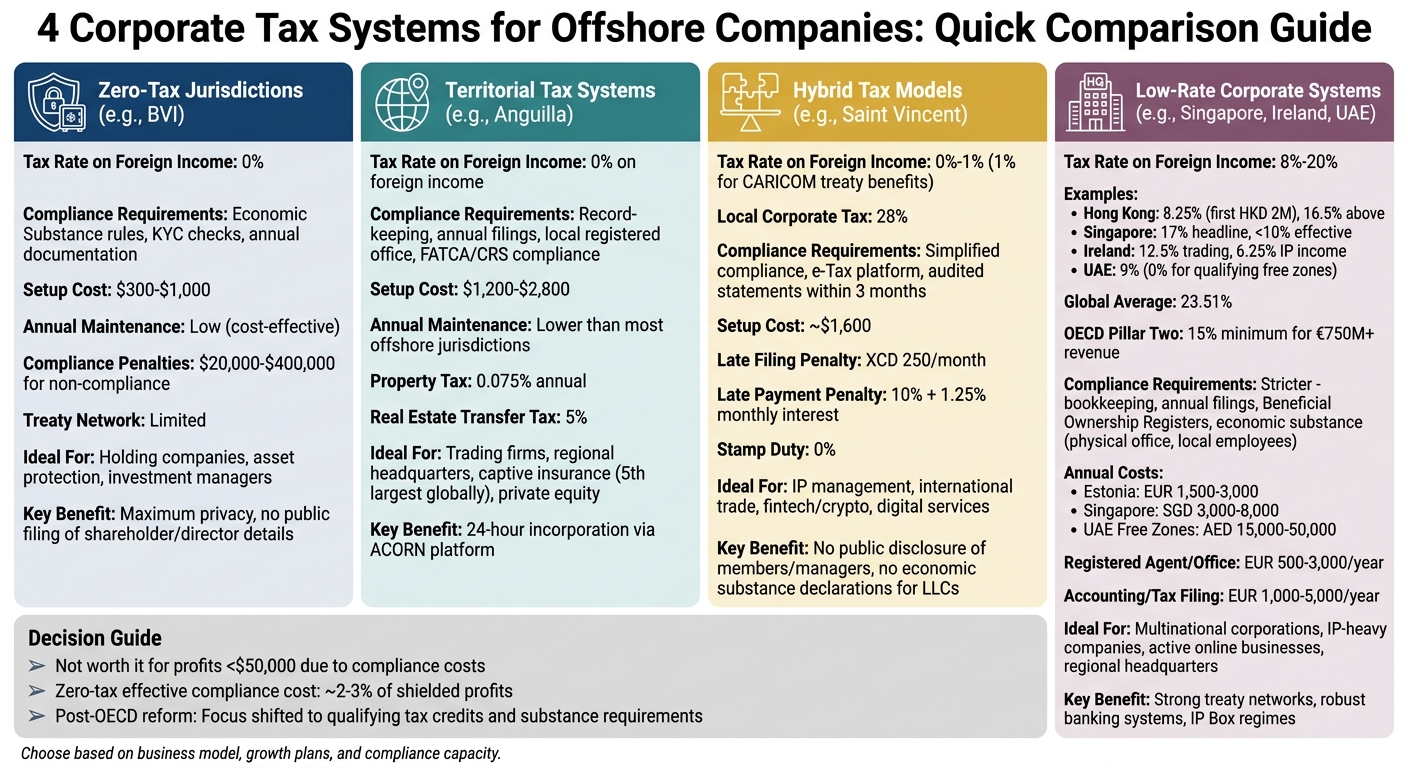

Selecting the right corporate tax system for your offshore company can save you money, reduce compliance headaches, and align with your business goals. This is especially critical when considering asset protection for the entrepreneur. Here are the four main options:

- Zero-Tax Jurisdictions: No corporate income tax on foreign-sourced income (e.g., British Virgin Islands). Best for holding companies and asset protection.

- Territorial Tax Systems: Only tax income earned locally (e.g., Hong Kong, Anguilla). Ideal for businesses with international operations.

- Hybrid Tax Models: Offer partial or full tax exemptions on foreign income (e.g., Saint Vincent). Suited for international trade and intellectual property management.

- Low-Rate Corporate Systems: Competitive tax rates (8%-20%) with access to treaties (e.g., Singapore, Ireland). Great for multinational corporations and IP-heavy businesses.

Quick Comparison:

| Tax System | Tax Rate on Foreign Income | Compliance Requirements | Ideal For |

|---|---|---|---|

| Zero-Tax Jurisdictions | 0% | Economic Substance rules | Holding companies, asset protection |

| Territorial Tax Systems | 0% on foreign income | Record-keeping, annual filings | Trading firms, regional headquarters |

| Hybrid Tax Models | 0%-1% | Simplified compliance | IP management, international trade |

| Low-Rate Systems | 8%-20% | Stricter compliance, substance | Multinationals, IP-heavy businesses |

Each system has pros and cons, so the best choice depends on your business model, growth plans, and compliance capacity. The article dives deeper into these systems and their suitability for different business types.

1. Zero-Tax Jurisdictions (e.g., British Virgin Islands)

Tax Rate on Foreign Income

In zero-tax jurisdictions like the British Virgin Islands (BVI), foreign-earned income – including capital gains, wealth, and VAT – is taxed at 0%. With more than 400,000 active BVI Business Companies as of early 2026, this "tax-neutral" framework has become a go-to option for businesses with international operations.

However, this doesn’t mean companies are entirely off the hook. For instance, U.S. citizens are still required to pay taxes on their worldwide income. Additionally, the BVI’s limited network of double taxation treaties means businesses must carefully assess how profits sourced in the BVI are treated in their home countries.

Compliance Requirements

Businesses involved in activities like banking, insurance, shipping, holding operations, or intellectual property management must adhere to the Economic Substance Act. This requires maintaining a physical presence in the BVI and submitting annual documentation. Non-compliance can result in hefty fines, starting at $20,000 and climbing up to $400,000.

The BVI has signed Tax Information Exchange Agreements with over 25 countries and participates in the Common Reporting Standard for automatic information exchange. Companies can only be formed through licensed registered agents, who are required to perform Know Your Client (KYC) checks on all beneficial owners. While financial statements are not publicly filed, companies are required to maintain internal accounting records for transparency.

These regulations, though strict, are balanced by cost-effective compliance procedures.

Setup and Maintenance Costs

Setting up a business in the BVI is relatively affordable. Registration costs $300 for companies with authorized share capital under $50,000, and $1,000 for those exceeding this threshold. The structure is simple: only one shareholder and one director are required, both of whom can be corporate entities. There’s no minimum paid-up capital beyond a single share. Additionally, the absence of foreign exchange controls makes it easier to engage in global trade and investment.

This streamlined process, combined with flexible relocation options under BVI law, makes the jurisdiction appealing for international businesses.

Ideal Business Types

BVI’s zero-tax regime is particularly suitable for international trading firms, holding companies, asset protection structures, investment managers, and e-commerce businesses. The jurisdiction offers a high level of privacy as there’s no requirement to file shareholder or director details with the public Registrar. This combination of zero taxation, straightforward compliance, and low operational costs makes the BVI an attractive choice for businesses that value confidentiality and operational flexibility.

sbb-itb-39d39a6

2. Territorial Tax Systems (e.g., Anguilla)

Tax Rate on Foreign Income

Anguilla stands out with its 0% corporate tax rate on all income – whether domestic or international. The only taxes levied are a minimal 0.075% annual property tax and a 5% real estate transfer tax. International Business Companies (IBCs) and Limited Liability Companies (LLCs) enjoy exemptions from income, profit, capital gains, and withholding taxes. On top of that, there’s no sales tax or VAT.

Compliance Requirements

While the zero-tax rate is a major draw, Anguilla ensures local economic participation through specific economic substance (ES) requirements. Companies involved in activities like banking, insurance, fund management, intellectual property, or holding company operations must prove they are managed and controlled from within Anguilla. This includes maintaining a local office, employing qualified staff, and incurring local expenses.

Incorporation must occur through a licensed local agent, and all companies need a registered office on the island. LLCs are required to keep accurate accounting records and file an annual return with basic company details. Anguilla also adheres to FATCA and the Common Reporting Standard (CRS), requiring financial institutions to submit annual returns. Businesses can be exempt from local ES rules if they prove tax residency and substantial activity in another jurisdiction.

Setup and Maintenance Costs

Anguilla makes company formation quick and easy with its online registration platform, ACORN, enabling incorporation within 24 hours. Setting up a basic IBC costs around $1,200, including disbursements, while forming an LLC typically costs about $2,800 through professional service providers. Annual maintenance fees are lower compared to many other offshore jurisdictions, making it cost-effective to manage and move funds across borders.

Ideal Business Types

Anguilla’s tax system is particularly suited for intermediary holding companies that serve as tax-neutral layers in complex corporate setups. The jurisdiction ranks as the fifth-largest globally for captive insurance, following Bermuda, Cayman, Vermont, and Guernsey. North American private equity firms often choose Anguillan LLCs, which can be structured as partnerships to allow income and losses to flow directly to members.

E-commerce businesses and international consultants benefit from the ability to handle multiple currencies and simplify cross-border payments. Additionally, Anguilla is a popular choice for asset holding vehicles used in leveraged finance, investment management, and asset protection or estate planning strategies. Its flexibility and alignment with diverse business needs make it an attractive option for companies seeking both operational efficiency and future compliance readiness.

"Anguilla’s success is based largely upon that traditional stalwart of the offshore industry – the International Business Company (or IBC)."

– Colin Riegels, Author and Partner, Harneys

3. Hybrid Tax Models (e.g., Saint Vincent)

Tax Rate on Foreign Income

Saint Vincent and the Grenadines operates with a two-tier tax system. Local companies are subject to a 28% corporate income tax on profits made within the country. However, International Business Companies (IBCs) and Limited Liability Companies (LLCs), governed by the IBC Act of 1996, enjoy a 0% tax rate on income sourced from abroad. Additionally, LLCs can opt for a 1% corporate tax rate to qualify for benefits under the CARICOM Double Taxation Treaty. The jurisdiction offers further tax advantages, such as no capital gains tax, no withholding tax on dividends or interest paid to non-residents, and no taxes on estates, inheritances, or gifts. This structure provides a favorable environment for businesses looking to optimize tax obligations.

Compliance Requirements

All tax filings are handled via the e-Tax Platform. Companies must submit audited or reviewed financial statements along with their annual returns within three months of the end of their financial year. Delayed filings incur a monthly penalty of XCD 250, while late payments are subject to a 10% penalty plus 1.25% monthly interest. LLCs enjoy simplified compliance, as they are not required to disclose member or manager details in any public register and are exempt from economic substance declarations. However, LLCs must maintain a registered office, a licensed agent, and pay an annual government fee, typically due in December. These streamlined procedures make compliance manageable for most businesses.

Setup and Maintenance Costs

Incorporating a Limited Liability Company in Saint Vincent is relatively affordable, with costs starting at around $1,600. IBCs are not subject to any minimum capital requirements. Companies also benefit from 0% stamp duty on share transfers and other corporate transactions, reducing overall operational expenses.

Ideal Business Types

Saint Vincent is particularly well-suited for holding companies managing international assets, as they are exempt from capital gains tax on asset sales and withholding taxes on dividends. Intellectual property management companies can also benefit by transferring patents or trademarks to subsidiaries in Saint Vincent, allowing them to collect royalties without incurring withholding tax. The jurisdiction has become increasingly attractive to fintech and cryptocurrency businesses, as well as international trade companies and digital service providers. These businesses can take advantage of the 0% tax on foreign income while operating in a jurisdiction with an established legal framework. For companies seeking a combination of tax efficiency and simplified regulations, Saint Vincent offers a compelling option.

4. Low-Rate Corporate Systems for Offshore Use

Tax Rate on Foreign Income

Low-rate corporate tax systems strike a balance between competitive tax rates and strong regulatory oversight. These jurisdictions typically impose corporate taxes ranging from 8% to 20%, offering an attractive alternative to zero-tax regimes. For context, the global average corporate tax rate across 181 jurisdictions is 23.51%.

Here are some notable examples:

- Hong Kong: Taxes profits at 8.25% on the first HKD 2,000,000 and 16.5% on amounts above that.

- Singapore: While the headline rate stands at 17%, various exemptions and incentives often reduce the effective rate to under 10%.

- Ireland: Maintains a 12.5% rate on trading income, with a reduced 6.25% rate for qualifying intellectual property income under its Knowledge Development Box.

- United Arab Emirates (UAE): Introduced a 9% federal corporate tax in 2023, though qualifying free zone businesses may still benefit from a 0% rate.

The OECD’s Pillar Two initiative has further shaped the tax landscape by introducing a 15% global minimum tax for multinational enterprises with revenues exceeding €750 million. As of 2024, several low-tax jurisdictions, including Bulgaria, Hungary, Ireland, Liechtenstein, and Barbados, adopted this 15% rate for large corporations through the Qualified Domestic Minimum Top-up Tax.

"Since 1980, countries have recognized the impact that high corporate tax rates have on business investment decisions; in 2024, the average is now 23.51 percent" – Cristina Enache, Tax Foundation

Compliance Requirements

Low-rate tax systems come with stricter compliance obligations compared to zero-tax regimes. These include bookkeeping, annual filings, and maintaining Beneficial Ownership Registers. Additionally, companies must demonstrate real economic substance, which often involves having a physical office, hiring local employees, and ensuring that key decisions are made locally.

- Singapore: Requires at least one ordinarily resident director.

- Hong Kong: Mandates a resident company secretary.

For businesses with annual profits below $50,000, the administrative workload and associated costs might outweigh the benefits of the lower tax rate. These compliance requirements contribute to the overall setup and maintenance costs, which vary depending on the jurisdiction.

Setup and Maintenance Costs

Meeting the compliance and substance requirements in low-rate jurisdictions comes with varying costs:

- Estonia: Annual costs range from EUR 1,500 to 3,000.

- Singapore: Costs fall between SGD 3,000 and 8,000 annually.

- UAE Free Zones: Annual expenses can range from AED 15,000 to 50,000, depending on the specific zone and license type.

Additional expenses, such as registered agent and office fees, typically range from EUR 500 to 3,000 annually. Accounting and tax filing services can add another EUR 1,000 to 5,000.

Ideal Business Types

Low-rate jurisdictions are particularly appealing for certain types of businesses. Their competitive tax rates and well-developed infrastructure make them a good fit for:

- Multinational corporations: Ideal as regional headquarters to manage and reduce taxes on international earnings.

- Intellectual property-heavy companies: Benefit from IP Box regimes, such as Cyprus’s 2.5% tax on qualifying IP income or Poland’s 5% rate.

- Active online businesses: Particularly advantageous for owners who relocate locally.

These jurisdictions also offer robust Double Taxation Treaty networks and strong banking systems, though the administrative demands may deter smaller businesses.

Pros and Cons of Each Tax System

Each corporate tax system comes with its own set of benefits and challenges, balancing tax savings, compliance demands, and operational needs. Here’s a closer look at how different tax systems align with varying business priorities.

Zero-Tax Jurisdictions

Places like the British Virgin Islands boast a 0% corporate tax rate and strong privacy protections. These jurisdictions are particularly appealing to holding companies and investment funds. However, there are some significant downsides. For instance, countries with higher tax rates, such as Germany or Australia, often reject intellectual property charges originating from zero-tax locations due to limited treaty networks. Additionally, banking can be tricky because of stricter due diligence requirements. There’s also the cost of complying with Economic Substance rules, which can effectively amount to around 2–3% of the profits being shielded.

Territorial Tax Systems

Territorial systems tax only income earned locally, making them a good fit for trading firms or regional headquarters. Anguilla, for example, offers a 0% corporate tax rate on all income, which simplifies tax obligations for global businesses. However, these systems can come with added complexities, such as mandatory record-keeping, annual filings, and the application of Controlled Foreign Corporation (CFC) rules designed to prevent tax avoidance.

Low-Rate Systems and Innovation Incentives

For businesses willing to meet stricter compliance requirements, low-rate systems strike a balance between competitive tax rates and access to Double Taxation Treaty networks. Ireland, for instance, offers a 12.5% tax rate on trading income, with additional benefits like Patent Box regimes that can reduce the effective tax rate on qualifying intellectual property income to as low as 6.25%. These setups are particularly attractive to tech and pharmaceutical companies. However, they require significant effort to establish, such as meeting substance requirements like maintaining a physical office and hiring local employees.

"The ‘race to the bottom’ is effectively over. Competition is now shifting towards ‘qualifying refundable tax credits’ and grants." – Global Tax Lead, BATO

The introduction of the OECD’s 15% global minimum tax has changed the game for large multinationals with revenues exceeding €750 million. For these companies, treaty access and substance requirements now carry more weight than headline tax rates. On the other hand, smaller businesses below this threshold often prioritize minimizing administrative burdens. In many cases, jurisdictions with "Small Profits Rates" – like the United Kingdom’s 19% rate for profits under £50,000 – offer better overall value compared to zero-tax havens, especially when compliance costs are factored in.

Ultimately, the choice of tax system depends on a company’s specific needs, weighing tax savings against regulatory requirements and operational considerations.

Conclusion

When selecting a tax system, it’s essential to consider how well it fits your business model and operational priorities. For instance, zero-tax jurisdictions like the British Virgin Islands are often appealing to holding companies and intellectual property owners. However, these locations now enforce strict economic substance requirements, which businesses must comply with.

Territorial tax systems, such as those in Hong Kong or Singapore, are particularly suitable for trading companies and regional operations. They offer a 0% tax rate on foreign income, alongside strong legal protections and extensive treaty networks.

For businesses focused on intellectual property or research and development, low-rate systems like Ireland’s 12.5% corporate tax regime provide competitive effective tax rates and access to a wide range of treaty benefits.

Hybrid systems, such as those in Saint Vincent, strike a balance. With a 15% headline rate, partial exemptions can reduce the effective tax burden to as low as 0% to 3% for Global Business Companies. These systems also grant access to numerous double taxation treaties, offering additional flexibility.

Global tax policies are shifting rapidly, influenced by reforms like the OECD’s 15% global minimum tax. Larger enterprises are now focusing on tools like qualifying refundable tax credits, substance-based income exclusions, and establishing genuine operational footprints to stay compliant and competitive in this evolving landscape.

"Choosing a domicile is no longer just about the lowest headline rate. It requires a holistic view of the regulatory environment, labor markets, and supply chain logistics." – Global Tax Lead, BATO

FAQs

How do I pick the best offshore tax system for my business?

When selecting an offshore tax system, it’s important to look beyond just the tax rates. Consider how the jurisdiction’s tax policies fit with your business model, industry specifics, and compliance requirements. Pay attention to factors like legal stability, access to key markets, banking infrastructure, and any available incentives. The best option will combine low tax rates with operational ease, strong legal safeguards, and opportunities for growth that align with your business objectives.

Will I still owe U.S. tax if my offshore company pays 0% corporate tax?

Yes, if you’re a U.S. tax resident, you’re taxed on your worldwide income – no matter what tax rate your offshore company pays. Even if your offshore company enjoys a 0% corporate tax rate, you could still owe U.S. taxes on your global earnings. It’s always a smart move to consult a tax professional to stay compliant with U.S. tax laws.

What do “economic substance” rules actually require in practice?

Economic substance rules mandate that companies demonstrate a real presence in the jurisdiction where they are registered. This includes proving they have genuine management, a physical presence, relevant business activities, and local expenditure. The goal is to prevent businesses from operating as mere shell companies without actual operations.