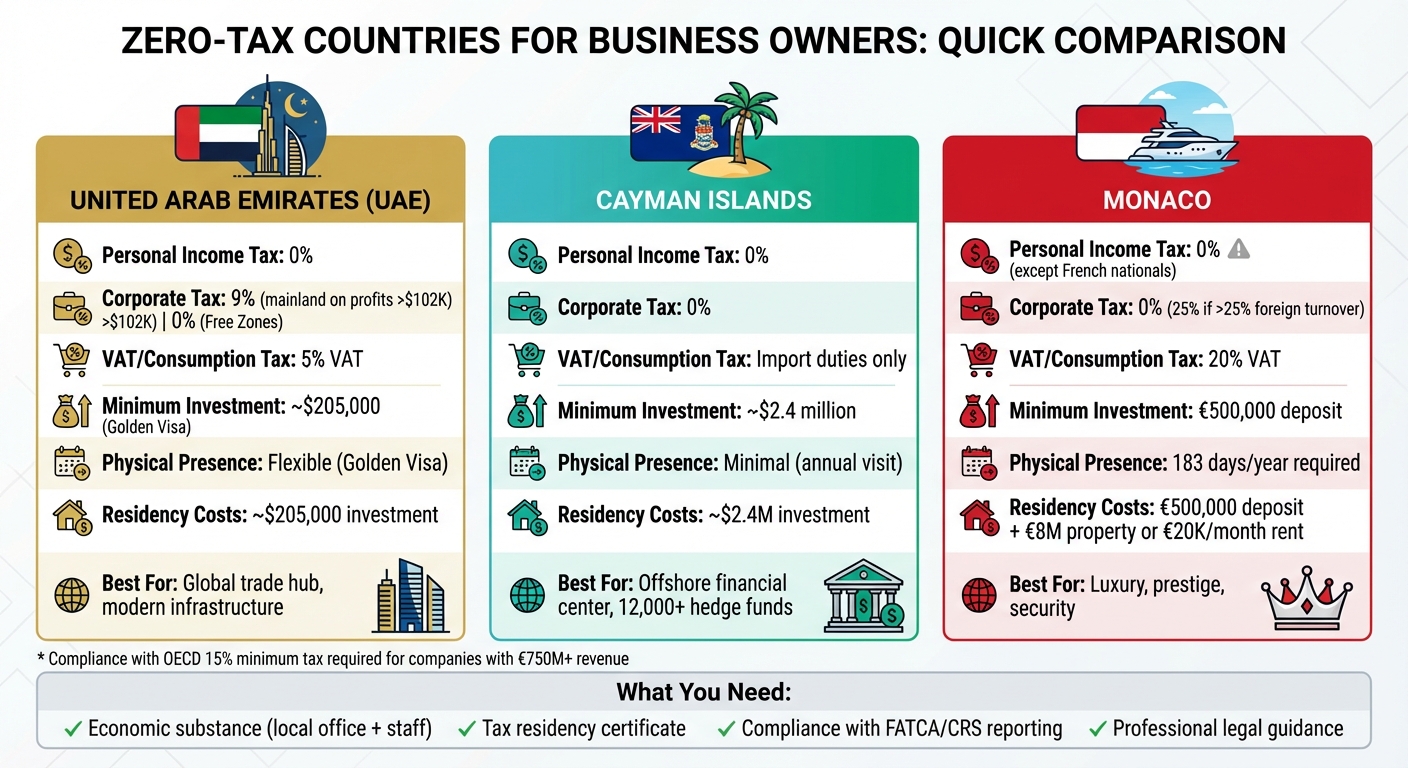

Zero-tax countries offer business owners the chance to pay 0% corporate and personal income taxes under specific conditions. These jurisdictions, like the UAE, Cayman Islands, and Monaco, attract entrepreneurs with tax-free earnings, asset protection, and global business opportunities. However, compliance is key, as international tax laws (like the OECD‘s 15% minimum tax for large companies) now require economic substance – a real local presence with staff, offices, and active operations.

Key Takeaways:

- Zero-Tax Countries: Examples include UAE, Cayman Islands, and Monaco.

- Advantages: No corporate/personal income tax, strong asset protection, and global trade access.

- Requirements: Economic substance rules, residency, and compliance with reporting standards (e.g., FATCA, CRS).

- Costs: Relocation and business setup costs vary widely (e.g., $205,000 in UAE, $2.4M in Cayman Islands, €500,000 deposit in Monaco).

Quick Comparison:

| Feature | UAE | Cayman Islands | Monaco |

|---|---|---|---|

| Personal Income Tax | 0% | 0% | 0% (except French nationals) |

| Corporate Tax | 9% (mainland); 0% in Free Zones | 0% | 0% (25% for foreign turnover) |

| Residency Costs | ~$205,000 investment | ~$2.4M investment | €500,000 deposit |

| VAT/Taxes | 5% VAT | Import duties | 20% VAT |

| Physical Presence | Flexible (Golden Visa) | Minimal (annual visit) | 183 days/year |

Zero-tax jurisdictions are ideal for entrepreneurs, investors, and high-net-worth individuals, but success requires planning, compliance, and aligning with international tax regulations.

Zero-Tax Countries Comparison: UAE vs Cayman Islands vs Monaco

Best Zero-Tax Countries for Business Owners

United Arab Emirates (UAE)

The UAE combines a 0% personal income tax with a modern corporate environment, offering entrepreneurs attractive options. Starting in 2023, mainland businesses face a 9% federal corporate tax on profits exceeding AED 375,000 (approximately $102,000). However, companies in designated Free Zones can still enjoy 0% tax on qualifying income. Mainland companies are ideal for local market access, while Free Zone entities are suited for those prioritizing tax benefits.

For smaller businesses, the UAE provides Small Business Relief for firms earning less than AED 3 million (about $817,000) annually, available until December 2026. The Golden Visa program offers residency for investments starting at AED 750,000 (roughly $205,000) in real estate or business ventures. The UAE expects to attract over 9,800 high-net-worth individuals by 2025, reflecting its growing appeal. Business setup costs range from AED 20,000 to AED 30,000 (approximately $5,450–$8,200), and a 5% VAT is applied to most goods and services.

"The UAE is the only no-tax country that combines residency, global trade access, modern infrastructure, and safety."

– Affinitas DMCC

Next, let’s look at the Cayman Islands – a long-standing favorite for tax-neutral businesses.

Cayman Islands

The Cayman Islands boast a tax-neutral system with 0% personal income, corporate, capital gains, and inheritance taxes. Government revenue comes from import duties, tourism, and financial service fees. It’s a hub for offshore investments, hosting over 12,000 hedge funds.

The Exempted Company is the most popular business structure here. It requires only one shareholder and one director, designed for international operations, but these companies cannot engage with local residents. For specific industries like banking, insurance, and fund management, economic substance rules mandate a genuine local presence. Residency via investment typically starts at $2.4 million, and certain permits come with no minimum stay requirement. However, companies in regulated sectors must comply with substance regulations to maintain their tax-neutral status.

Now, let’s shift to Europe and explore Monaco’s unique blend of luxury and low taxes.

Monaco

Monaco offers 0% personal income tax for residents, excluding French nationals, and no taxes on investment income, capital gains, or dividends. Businesses operating primarily within Monaco are exempt from corporate tax, but a 25% tax applies if more than 25% of turnover is generated outside the principality.

"Monaco is no longer a tax haven: it does have very low taxes, but both the European Union and the OECD have removed it from the list of non-cooperative jurisdictions."

– Marc Cantavella, Manager, The Global Wealth

Residency requires living in Monaco for at least 183 days annually, verified through utility bills or similar documents. Financially, the barrier is steep, with a minimum €500,000 bank deposit typically required. Real estate prices are among the highest globally, averaging €51,967 per square meter in 2024, with a modest two-bedroom apartment costing around €8 million to buy or €20,000 monthly to rent. Monaco also applies a 20% VAT, aligned with the French system, and non-EU nationals must secure a French type-D visa before starting residency procedures.

| Feature | United Arab Emirates | Cayman Islands | Monaco |

|---|---|---|---|

| Personal Income Tax | 0% | 0% | 0% (except French nationals) |

| Corporate Tax | 9% on profits above AED 375k; 0% for Free Zones | 0% | 0% (or 25% if >25% of turnover is foreign) |

| VAT/Consumption Tax | 5% | Import duties | 20% |

| Minimum Investment | ~ $205,000 | ~ $2.4 million | €500,000 deposit |

| Primary Appeal | Global trade hub with modern infrastructure | Offshore financial center with a focus on hedge funds | Luxury, security, and prestige |

| Minimum Stay Requirement | Flexible (Golden Visa) | None for specific permits | 183 days per year |

sbb-itb-39d39a6

Legal Requirements for Zero-Tax Business Operations

OECD Global Minimum Tax Rules

The OECD’s Pillar Two framework applies to multinational enterprises (MNEs) with annual consolidated revenues of €750 million or more. These companies must ensure they pay a minimum effective tax rate of 15% in every jurisdiction where they operate. If they fall below this rate, they may face a "top-up tax" to meet the 15% threshold.

In response, many zero-tax jurisdictions are introducing their own Qualified Domestic Minimum Top-up Tax (QDMTT) to enforce the 15% rate locally. For instance, the UAE will implement its Domestic Minimum Top-up Tax (DMTT) starting in January 2025 for large MNEs. Additionally, these businesses must prove they have economic substance in these jurisdictions by maintaining local offices, employing staff, and generating revenue within the region. Companies covered by these rules are also required to file a GloBE Information Return (GIR) by June 30, 2026.

"The introduction of the global minimum tax has permanently altered the offshore landscape. What was once a system built on secrecy and arbitrage is now moving toward transparency, substance, and strategic alignment." – OVZA Legal Affairs

Although the €750 million threshold primarily targets large enterprises, smaller businesses are also feeling the ripple effects. Increasingly, banks and payment processors are holding offshore entities to similar transparency standards.

These international frameworks are shaping specific tax reporting requirements, especially for U.S. taxpayers.

US Tax Reporting Requirements

For U.S. citizens and residents, compliance with global tax standards comes with additional complexities. The IRS applies citizenship-based taxation, meaning worldwide income is taxable regardless of where a person lives or where their business is incorporated. In July 2025, the U.S. replaced the GILTI regime with Net CFC Tested Income (NCTI), removing the Qualified Business Asset Investment (QBAI) exemption. This change reduced the Section 250 deduction to 40%, resulting in an effective tax rate of approximately 12.6%–14% on foreign income.

U.S. taxpayers with foreign accounts and financial assets must also comply with FBAR and FATCA reporting requirements. The first GloBE Information Returns (GIR) for calendar-year groups are due by June 30, 2026. Furthermore, the OECD’s Side-by-Side (SbS) Safe Harbor, effective January 1, 2026, might allow U.S.-parented multinational groups to avoid additional top-up taxes under specific conditions.

"GILTI is dead. Long live NCTI." – Crossfoot

Given these changes, regular reviews of offshore structures are now more critical than ever. With the removal of the QBAI shield, holding tangible assets offshore offers fewer tax advantages. To prepare for potential audits, businesses should maintain detailed documentation, such as utility bills, lease agreements, and payroll records.

Double Taxation Treaties

Double Taxation Treaties (DTTs) play a key role in managing tax liabilities for cross-border income. These treaties aim to prevent the same income from being taxed in multiple jurisdictions. For businesses operating in zero-tax regions, DTTs often reduce or eliminate withholding taxes on foreign income. For example, the U.S. has tax treaties with roughly 65 countries, while India has agreements with 94 nations.

Without a treaty, the U.S. standard withholding tax on dividends is 30%. Treaties can lower this rate to 15% or even 5% for substantial holdings. Interest withholding rates are often reduced to 0% or 10% under these agreements. Treaties also define Permanent Establishment (PE) thresholds, meaning a business’s profits are generally taxable in a foreign country only if it maintains a fixed place of business there.

To take advantage of treaty benefits, businesses may need a Tax Residency Certificate (TRC) from their home country. U.S. taxpayers must also file IRS Form 8833 (Treaty-Based Return Position Disclosure) and ensure their business meets Limitation on Benefits (LOB) requirements.

However, most treaties include a "Saving Clause", which allows countries like the U.S. to tax their own citizens and residents as if the treaty did not exist. As a result, these treaties primarily shield taxpayers from foreign taxes, offering limited protection against domestic obligations for U.S. citizens.

Understanding how these treaties work is a critical step before considering any business relocation strategies.

How to Relocate and Set Up Your Business

How to Establish Tax Residency

Moving your tax residency to a zero-tax jurisdiction involves several practical steps, and the process can take anywhere from six months to over a year. Starting early is crucial.

The first step is securing long-term housing. This could mean purchasing property or signing a rental agreement for at least a year. You’ll also need to demonstrate financial stability, often by making a significant deposit in a local bank. For example, in Monaco, where property prices averaged €51,967 per square meter in 2024, renting is often the more feasible choice. Monaco banks typically require a deposit as proof of financial sufficiency. In the Cayman Islands, the required deposit is approximately $600,000 (KYD 500,000).

If you’re a non-EU/EEA citizen, you’ll need to secure a long-stay visa before applying for residency. For Monaco, this involves obtaining a French Type-D visa. Applicants must also provide a clean criminal record from every country they’ve lived in over the past five years. These documents must be less than three months old and professionally translated into the local language.

Meeting the physical presence requirement is another key step. For Monaco, this means spending more time in the country than in any other single location. To maintain your residency status during renewals, you’ll need to provide evidence of daily life, such as utility bills or credit card statements.

Processing times for residency applications vary widely. For EU passport holders, Monaco’s process averages around 8 weeks, while non-EU citizens may wait 16 to 20 weeks. In the Cayman Islands, temporary work permits take 5–10 days, but annual permits require 6 weeks to 3 months. Once your residency is approved, obtaining a Tax Residency Certificate is essential for protecting yourself from taxation in other countries.

There are exceptions to keep in mind. French nationals living in Monaco must still pay French income tax due to a 1963 treaty. Similarly, U.S. citizens are subject to worldwide taxation, regardless of their residency status.

| Feature | Monaco | Cayman Islands |

|---|---|---|

| Minimum Bank Deposit | ~€500,000 | ~$600,000 (KYD 500,000) |

| Major Investment Requirement | None (real estate purchase or rent) | $1.2M (KYD 1M) |

| Processing Timeline | 8 weeks (EU) to 20 weeks (non-EU) | 6 weeks to 3 months (work permits) |

| Physical Presence for Tax | 183 days (or center of interest) | Minimal (annual visit for some certificates) |

| Path to Permanent Status | 10 years for Privileged Card | 8–9 years for Permanent Residence |

Business Incorporation Steps

Once you’ve established tax residency, the next step is setting up your business in the chosen jurisdiction. In the UAE, for instance, you can start by selecting a free zone like JAFZA or DIFC. From there, choose your legal structure – whether a branch or an LLC – apply for a trade license, and secure a physical office or workspace within the free zone. These zones offer perks like 100% foreign ownership and full profit repatriation.

In the Cayman Islands, businesses often opt for an Exempted Company, which provides a 20-year tax exemption and minimal local operational requirements. Basic registration fees start at around $250, though professional services can increase the overall costs.

Regardless of location, you’ll need to demonstrate economic substance. This means having local directors or staff, maintaining a physical office, and conducting core income-generating activities within the jurisdiction. These requirements have become stricter under international frameworks like CRS and FATCA.

Costs for residency assistance vary. In the Cayman Islands, packages range from $4,500 to $9,000, with comprehensive services costing between $29,000 and $56,000. In Monaco, permit fees are €80 for one year, €100 for three years, and €160 for ten years.

Working with Global Wealth Protection

After incorporating your business, professional guidance can simplify the offshore setup process. Global Wealth Protection specializes in forming offshore companies and private U.S. LLCs, tailored for location-independent entrepreneurs. They often work with Anguilla for offshore incorporation, offering comprehensive packages that include filings, certifications, and bank introductions.

For those prioritizing asset protection and privacy, Global Wealth Protection provides U.S. LLC formation services with registered agent support and expert advice. These structures pair well with offshore companies in zero-tax jurisdictions, creating multiple layers of protection while staying compliant.

The GWP Insiders membership program offers detailed internationalization strategies, including tax minimization, jurisdiction selection, and one-on-one consultations. Members also gain access to the Global Escape Hatch action plans, which provide step-by-step guidance for relocation.

For high-net-worth individuals, Global Wealth Protection offers advanced estate planning options like offshore trusts and private interest foundations in Anguilla. These tools go beyond basic corporate structures, offering sophisticated solutions for managing assets. Personalized consultations are available, ensuring strategies align with your tax obligations, business goals, and relocation plans.

Conclusion

Summary of Zero-Tax Jurisdiction Benefits

Zero-tax jurisdictions allow businesses to keep 100% of their earnings in places where statutory tax rates are 0%. This creates opportunities for streamlined tax planning, international trade, holding companies, and managing intellectual property ownership. Additionally, these jurisdictions often provide strong asset protection and privacy. Locations like the Cayman Islands and Bermuda stand out for their stable political environments and legal systems rooted in English common law.

However, the rules have tightened. Today, leveraging these jurisdictions effectively requires genuine economic substance – think local directors, physical office space, and real business activity. Compliance is no longer optional. The OECD’s Pillar Two rule imposes a 15% minimum tax on multinationals with revenues above €750 million. Meanwhile, U.S. citizens must navigate worldwide tax obligations and FBAR requirements, with penalties for non-willful violations starting at $16,536 per form in 2025. Successful use of zero-tax jurisdictions now hinges on strict adherence to international standards like the Common Reporting Standard (CRS) and FATCA reporting.

"The lowest-tax country is rarely the smartest choice on its own. What matters is how well a country aligns with where you actually live and where your income is generated."

- Savory & Partners

With these factors in mind, aligning your business with the right jurisdiction requires careful planning and execution.

Your Next Steps

To determine if a zero-tax jurisdiction works for your business, start by assessing whether it aligns with your financial and operational goals. For instance, consider the $270,000 threshold for UAE residency or the $1.2 million requirement for the Cayman Islands. Ensure you can document your physical presence with evidence like utility bills, travel records, and bank statements to establish tax residency.

Next, secure a Tax Residency Certificate and cut ties with your previous jurisdiction. This means canceling licenses, closing local bank accounts, and addressing any exit tax obligations while reviewing our offshore banking report for secure capital management. A residency certificate is essential for activating double taxation treaty benefits and shielding foreign-sourced income from being taxed by your home country.

For those navigating these complexities, Global Wealth Protection offers tailored solutions. Their services include offshore company formation in Anguilla, private U.S. LLC structures for asset protection, and advanced estate planning using offshore trusts and private interest foundations. Through their GWP Insiders membership, you can access expert strategies on jurisdiction selection and personalized advice to meet your tax and business needs. Whether you’re aiming for zero-tax status or exploring territorial tax systems, professional guidance is key to staying compliant while maximizing the advantages of international structuring.

FAQs

Will I still owe tax in my home country if I move to a zero-tax jurisdiction?

When you move to a zero-tax jurisdiction, you might still have tax obligations in your home country. This hinges on how your home country defines tax residency. Some nations tax their citizens or residents on their worldwide income, no matter where they live. Others only tax income earned within their borders. To understand your responsibilities, it’s crucial to review your home country’s specific tax laws.

What counts as "economic substance" to keep zero-tax status?

Economic substance refers to showcasing actual business operations within a particular jurisdiction to prove genuine economic involvement. This usually involves maintaining a physical office, employing local staff, and carrying out core business activities on-site. Adhering to these standards is crucial to steer clear of allegations related to tax avoidance or exploiting zero-tax advantages.

How do I avoid triggering permanent establishment (PE) tax in other countries?

To steer clear of triggering permanent establishment (PE) tax, it’s crucial to structure your operations thoughtfully and adhere to local tax regulations. Here are some practical strategies to consider:

- Limit physical presence: Avoid maintaining a fixed place of business in a foreign country unless absolutely necessary.

- Avoid dependent agents: Ensure that individuals or entities acting on your behalf do not have the authority to conclude contracts in the local jurisdiction.

- Monitor activities: Keep a close eye on business operations that could unintentionally create PE risks, such as extended stays or frequent visits by employees.

Additionally, maintaining thorough documentation is essential. You might also explore compliant legal options, such as working with independent contractors or partnering with an Employer of Record (EOR). These approaches can help reduce the risk of PE tax exposure while ensuring compliance with local laws.