If you earn money internationally, you might be paying more taxes than necessary. Territorial tax systems, used by 43 countries, only tax income earned within their borders, leaving foreign income tax-free. This approach is popular among expats, digital nomads, and international businesses because it simplifies taxes and reduces liability.

Key takeaways:

- Territorial taxation focuses on where income is earned, not where you live or your citizenship.

- Foreign income exemptions vary by country, with some taxing only when income is brought into the country.

- Residency rules, like spending 183+ days in a country, determine eligibility for these systems.

- Economic substance is essential – proof of local operations and income sourcing is often required.

Countries like Panama, Hong Kong, and Singapore offer attractive frameworks for tax optimization. However, global rules like the OECD‘s 15% minimum tax are changing the landscape, especially for large businesses. To benefit, individuals and businesses must carefully plan residency, income sourcing, and compliance with local and international laws.

What is a Territorial Tax System?

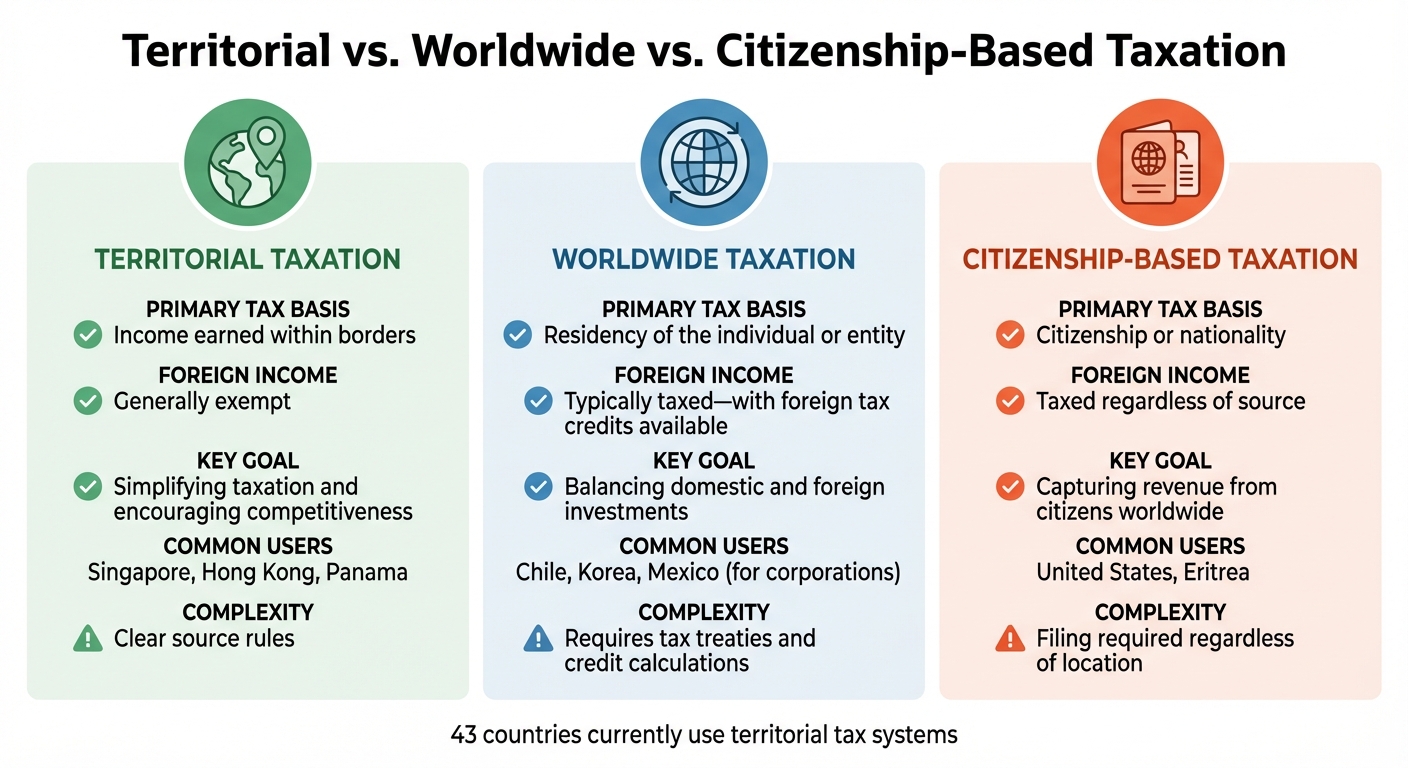

Territorial vs Worldwide vs Citizenship-Based Taxation Comparison

A territorial tax system – sometimes called source-based taxation – only taxes income earned within a country’s borders. If you live under this system and earn money from foreign sources, that income is generally exempt from local taxes. The focus here is on where the income is generated, not on the residency or citizenship of the individual earning it.

This differs from a worldwide tax system (also known as residence-based taxation), where a country taxes all the income its residents earn, no matter where it comes from. For example, if you live in a country with worldwide taxation and earn rental income from overseas property, you’d owe taxes on that income in your home country. However, foreign tax credits are often available to help avoid double taxation.

Then there’s citizenship-based taxation, which taxes the global income of individuals based solely on their citizenship, regardless of where they live. The United States is the most notable example, requiring all U.S. citizens to file tax returns and potentially pay taxes on income earned anywhere in the world. Eritrea is the only other country with a similar system.

Territorial systems often include participation exemptions, meaning profits are taxed only in the country where they’re made. As former U.S. Treasury Secretary William Simon once said, "The nation should have a tax system that looks like someone designed it on purpose."

Territorial vs. Worldwide and Citizenship-Based Taxation

The differences between these systems are crucial for anyone involved in international tax planning:

| Feature | Territorial Taxation | Worldwide Taxation | Citizenship-Based Taxation |

|---|---|---|---|

| Primary Tax Basis | Income earned within borders | Residency of the individual or entity | Citizenship or nationality |

| Foreign Income | Generally exempt | Typically taxed – with foreign tax credits available | Taxed regardless of source |

| Key Goal | Simplifying taxation and encouraging competitiveness | Balancing domestic and foreign investments | Capturing revenue from citizens worldwide |

| Common Users | Examples: Singapore, Hong Kong, Panama | Examples: Chile, Korea, Mexico (for corporations) | Examples: United States, Eritrea |

| Complexity | Clear source rules | Requires tax treaties and credit calculations | Filing required regardless of location |

These distinctions make territorial systems appealing to international investors and expats looking for tax efficiency. Many find success by implementing tax and residency solutions for digital nomads to legally minimize their global obligations.

Since the 2017 Tax Cuts and Jobs Act, the U.S. has adopted a hybrid system for corporations. Income from foreign physical assets is largely taxed under territorial rules, while intangible profits (like those subject to GILTI) and passive income still fall under worldwide taxation. This reform also lowered the corporate tax rate from 35% to 21%. However, for individuals, the U.S. continues to use citizenship-based taxation.

Among OECD countries, only Chile, Korea, and Mexico still apply fully worldwide tax systems to corporations. Most nations have shifted toward territorial models to make their economies more competitive and reduce barriers to global capital flows.

Up next, learn how these systems function in practice to help you optimize your tax strategy.

sbb-itb-39d39a6

How Territorial Taxation Works in Practice

Understanding how territorial tax systems function day-to-day can help you make smarter decisions about managing your income. The basic idea is simple: tax authorities focus on where your income is earned, not where you live or what passport you hold. This geographic approach opens up opportunities to legally reduce your tax burden if you earn money across borders. Let’s dive into some real-world examples to see how this plays out.

Some countries use remittance-based rules, meaning foreign income is only taxed when you transfer it into the country. Take Singapore and Malaysia, for instance – if you keep your foreign earnings in offshore accounts, they remain untaxed. This creates a strategic advantage: earn money abroad, keep it abroad, and avoid local taxes on that income. These principles provide a foundation for understanding how various types of income are treated under territorial systems.

Examples of Foreign Income Exemptions

Different types of income are treated differently under these systems. For example, let’s say a technology consultant based in Singapore travels to Vietnam to complete a project for a U.S. client. Because the work is physically done in Vietnam, the income is considered foreign-sourced and exempt from Singapore’s taxes. The key factor here is the physical location where the service is performed.

In the case of international trade, Hong Kong offers a clear example. Businesses that negotiate, finalize, and execute contracts outside Hong Kong can structure their operations to ensure profits are treated as foreign-sourced, even if management remains in Hong Kong.

Investment income has its own set of rules. Dividends are taxed based on where the paying company is incorporated. For instance, a Panama resident receiving dividends from a Delaware-based corporation would not owe Panama taxes on that income. Interest income, on the other hand, is sourced to where the borrower resides or where the debt is secured. Rental income is always tied to the physical location of the property.

Uruguay provides a particularly compelling case for passive income earners. New tax residents in Uruguay enjoy a 10-year tax holiday on foreign passive income, such as interest and dividends. For example, someone moving to Uruguay with a portfolio of U.S. stocks and bonds could pay no Uruguayan taxes on those earnings for a decade.

To maximize these benefits, it’s essential to understand exactly how income sourcing is determined.

How Income Source is Determined

Tax authorities rely on specific rules to classify income as either domestic or foreign, and these rules vary depending on the type of income:

| Income Type | Sourcing Rule |

|---|---|

| Services/Compensation | Where the service is physically performed |

| Dividends | Country where the paying corporation is incorporated |

| Interest | Residence of the borrower or location of the debtor |

| Rents | Physical location of the real property |

| Royalties | Where the intellectual property is actually used |

| Trading Profits | Where contracts are negotiated, concluded, and executed |

For service-based income, the deciding factor is your physical presence. For example, if you’re a software developer working from a café in Lisbon for a client in Toronto, the income is sourced to Portugal because that’s where the work occurred – even if your client is based elsewhere.

Trading income requires a more detailed look at the transaction process. In Hong Kong, for example, if all aspects of a transaction – negotiation, finalization, and execution – take place outside its borders, the profits are considered foreign-sourced. This gives businesses the flexibility to structure their operations strategically while maintaining a presence in Hong Kong.

For intellectual property, the source is tied to where the asset is used. A patent owned by a Panama company but licensed to manufacturers in China would generate income considered foreign-sourced for Panama.

Remittance rules add another layer of complexity. In countries like Singapore and Malaysia, foreign income is only taxed when brought into the country. By keeping earnings in offshore accounts, you can avoid local taxes. However, transferring those funds into a domestic account could trigger taxation.

Finally, modern territorial systems often include anti-avoidance rules to prevent artificial profit shifting. Similar to the U.S. GILTI regime, these rules target passive income or mobile profits that could be moved to low-tax jurisdictions without substantial economic activity. To comply, businesses need real substance – like physical offices, local staff, and genuine operations – rather than relying on paper-based setups.

Benefits of Territorial Tax Systems

Territorial taxation has gained traction globally, with many countries adopting it to stay competitive on the international stage. Let’s dive into why this system is appealing.

The standout benefit? Lower tax liability. In a territorial system, you’re taxed only on income earned within the country. Foreign-sourced income – whether it’s dividends, rental income, or sales from international markets – remains untaxed. This setup can lead to significant savings for individuals and businesses operating across multiple countries. For companies, it levels the playing field by removing home-country taxes on overseas earnings, making international operations more attractive.

Another major perk is the ease of repatriation. Companies can bring profits earned abroad back home without facing additional corporate taxes. By eliminating repatriation taxes, this system encourages reinvesting capital domestically.

Territorial taxation also provides strategic flexibility. High-net-worth individuals and remote workers can reduce their effective tax rates by establishing residency in a territorial jurisdiction while maintaining income streams from around the globe.

These advantages set the stage for strategies that help avoid double taxation and streamline compliance.

Avoiding Double Taxation

One of the biggest challenges under worldwide taxation is the risk of being taxed twice – once in the country where the income is earned and again in your home country. Territorial systems sidestep this issue by excluding foreign-sourced income from domestic taxation. For example, income that might be taxed twice under a worldwide system is often tax-free in a territorial system.

Another tool territorial systems use is participation exemptions. These allow multinational corporations to exclude or deduct dividends received from foreign subsidiaries from their taxable income at home. This approach is far simpler than dealing with the complex web of double tax treaties and foreign tax credits required under worldwide taxation.

The difference becomes even more striking when compared to citizenship-based taxation. Currently, only the United States and Eritrea tax their citizens on worldwide income, though residency-based taxation has been proposed as a potential alternative for U.S. expats. This means U.S. citizens living abroad must file U.S. tax returns and may owe taxes, even if they’ve lived overseas for decades. Territorial systems, by focusing solely on where the income is earned, eliminate this burden entirely.

Simpler Tax Compliance

Territorial taxation doesn’t just save money – it also saves time. Instead of tracking and reporting global earnings, taxpayers only need to focus on income earned domestically. Worldwide taxation, on the other hand, often requires complex filings that can drain significant resources.

"The nation should have a tax system that looks like someone designed it on purpose." – William Simon, former U.S. Treasury Secretary

Territorial systems simplify reporting requirements. Unlike worldwide systems, which demand full disclosure of global assets and income, territorial jurisdictions usually require reporting only for income sourced within their borders. For corporations, participation exemptions remove the need to calculate extra domestic taxes on repatriated profits. This clarity not only simplifies compliance but also speeds up financial planning and decision-making for international growth.

For individuals – like digital nomads – this means a lighter administrative burden. If you live in a territorial jurisdiction, you only need to report income earned within that country, while other earnings remain untaxed locally. This straightforward approach makes managing taxes much easier, freeing up time and energy for other priorities.

Countries with Territorial Tax Systems

Currently, 43 countries operate under territorial tax systems. Each country treats foreign income and tax benefits differently, so understanding these nuances is essential when deciding which jurisdiction aligns with your needs. Let’s look at how some key jurisdictions handle these systems.

Panama and Paraguay keep things relatively simple. Panama uses a pure territorial system, meaning foreign-source income isn’t taxed – even if it’s deposited into local banks or spent domestically. However, local income is taxed progressively, ranging from 0% to 25%. Paraguay, on the other hand, applies a flat 10% tax on local income while leaving foreign earnings untouched.

Some countries use a remittance-based system, taxing foreign income only when it’s brought into the country. Singapore generally exempts foreign-sourced income from taxation. Hong Kong follows a similar model, taxing foreign income only if it’s remitted into the territory. Since January 1, 2023, however, Hong Kong has introduced economic substance requirements for certain types of income, like dividends and interest. Malta also taxes foreign income only upon remittance.

Other jurisdictions design their systems to attract specific groups. For instance, Malaysia has historically exempted foreign income and continues to do so for individuals until December 31, 2026. To establish tax residency, you’ll need to spend 182 days in the country. Georgia offers an attractive 1% tax rate for small businesses, with most foreign income exempt if structured correctly. Meanwhile, Costa Rica and Nicaragua exclude foreign income from taxes altogether, with Nicaragua offering a fast-track, three-month process to gain tax residency.

Territorial Tax Jurisdictions

Here’s a quick comparison of some popular territorial tax systems:

| Jurisdiction | Tax on Foreign Income | Tax on Local Income | Residency Requirement | Best For |

|---|---|---|---|---|

| Panama | 0% | 0–25% progressive | 183 days | Remote professionals, retirees |

| Singapore | 0% (conditions apply) | Up to 24% | 183 days | Trading, investment firms |

| Hong Kong | 0% (unless remitted) | 17% profits tax | Business substance | International business operations |

| Malaysia | 0% (until 2026) | Progressive rates | 182 days | Digital nomads, remote workers |

| Paraguay | 0% | 10% flat rate | Varies | Low-tax local operations |

| Georgia | 0% (with setup) | 1% for small business | Varies | Small business owners |

| Costa Rica | 0% | Progressive rates | Varies | Remote workers |

These comparisons help pinpoint which jurisdiction might suit your specific situation.

To take advantage of these systems, you’ll typically need to meet certain requirements. Most countries require about 183 days of physical presence to establish tax residency. You’ll also need to prove that your income is foreign-sourced. For example, in Hong Kong, income is classified based on where contracts are negotiated and executed. In Panama, you must demonstrate that your center of economic interest lies outside the country.

Additionally, modern territorial systems increasingly emphasize economic substance. This means you’ll need genuine local operations, not just a mailing address. For example, jurisdictions like Singapore and Hong Kong now require local staff and operating expenses to qualify for exemptions. These changes reflect global efforts by organizations like the OECD and EU to curb "paper-only" structures.

"The most sophisticated tax strategies don’t rely on loopholes or aggressive schemes – they leverage fundamental differences in how tax systems treat global income." – Project Black Ledger

Keeping detailed records of your income sources and physical presence is critical for meeting residency and economic substance requirements.

Strategies for Tax Optimization Using Territorial Systems

Taking advantage of territorial taxation can help you manage your tax obligations more efficiently. By combining strategic offshore company structures with thoughtful residency planning, you can reduce your tax burden while staying compliant with local and international laws.

Setting Up Offshore Companies

Creating an offshore company in a territorial tax jurisdiction can significantly lower your tax liability. Many countries with territorial systems allow businesses to exclude foreign-earned income from domestic taxation through participation exemptions. Essentially, only income generated within the country’s borders is taxed, leaving global revenue untouched as long as it isn’t locally sourced.

However, meeting economic substance requirements is key. Most jurisdictions demand that companies demonstrate real local operations, such as maintaining a physical office and hiring local staff. For example, if you operate a consulting business, you could set up in a country like Panama or Georgia. By establishing a local office, opening a bank account, and ensuring your services cater to clients outside the country, you can take advantage of favorable tax policies. Panama taxes foreign income at 0%, while local income is taxed at a flat 10% rate. In Georgia, small businesses pay just 1% on turnover up to 500,000 GEL annually, with most foreign income excluded when structured properly.

To ensure your income qualifies as foreign-sourced, carefully document where your services are performed, where contracts are signed, and where your clients are located. Keep in mind anti-avoidance laws, especially if you’re a U.S. citizen. Rules like Controlled Foreign Corporation (CFC) provisions, Subpart F, and GILTI (Global Intangible Low-Taxed Income) can impose domestic taxes on certain types of foreign income.

These corporate structuring strategies work best when integrated with personal residency planning, creating a well-rounded approach to tax optimization.

Residency Planning

Choosing the right residency is equally important for leveraging territorial tax benefits. Your residency determines which tax system applies to you, and living in a territorial tax country can exempt your foreign income from taxation – provided you meet specific criteria.

A central concept is the 183-day rule, which many territorial systems use to establish tax residency. Spending 183 days or more in a country during a rolling 12-month period often triggers tax residency. However, simply holding a visa or residence permit doesn’t automatically make you a tax resident. You typically need to either meet the physical presence threshold or establish your "center of life" in that country.

Before relocating, track your physical presence carefully, establish meaningful local ties, and analyze your income sources. Definitions of "foreign-sourced" income vary by jurisdiction. For instance, in Hong Kong, income classification depends on where contracts are negotiated and executed. In Panama, you must prove that your economic interests lie outside the country. Ensuring your income streams meet these definitions is critical.

Once you fulfill residency requirements, register with the local tax authority and secure a tax residency certificate. This document proves your tax residency to foreign authorities and is essential for utilizing double taxation treaties, which can prevent your income from being taxed in both your new and former countries.

Timing your move strategically is also crucial. Arriving in January versus December can affect which tax year you’re subject to and when your local tax obligations begin. For U.S. citizens, moving to a territorial tax country like Panama can help maximize the benefits of the Foreign Earned Income Exclusion (FEIE) while avoiding local taxes on the remaining income.

Different countries offer various pathways to residency. Nicaragua provides a three-month process to establish tax residency, while Malaysia’s Digital Nomad Visa simplifies residency for remote workers. In remittance-based systems like Malaysia or Malta, keeping foreign-sourced and domestic income in separate accounts is vital. Bringing foreign income into the country can trigger taxes, so maintaining separate bank accounts simplifies reporting and avoids unnecessary tax liabilities.

"The strength of a territorial tax structure lies not in its complexity, but in the clarity and completeness of its documentation." – Project Blackledger

Lastly, always consult a local tax attorney. Tax laws and residency programs are subject to frequent changes, and requirements differ across jurisdictions. A qualified attorney in both your home country and your target jurisdiction can help you stay compliant with changing regulations and anti-avoidance measures.

The OECD Minimum Tax and Its Impact

When navigating tax strategies under territorial systems, the OECD’s Pillar Two framework has become a game-changer.

In January 2026, the global tax environment underwent a major transformation with the rollout of the OECD’s Pillar Two framework. This 15% global minimum tax ensures that multinational enterprises (MNEs) pay at least this rate on profits in every jurisdiction where they operate. For businesses using territorial tax systems – where foreign income is usually exempt from domestic taxation – this introduces a significant shift. Now, if foreign income is taxed below 15%, the home country (or another jurisdiction) can impose a "top-up" tax to bridge the gap.

This framework applies to MNEs with annual consolidated revenues of at least €750 million in at least two of the last four fiscal years. It operates through three primary mechanisms:

- Income Inclusion Rule (IIR): Allows a parent company’s home country to impose a top-up tax on low-taxed foreign subsidiaries.

- Undertaxed Profits Rule (UTPR): Acts as a safeguard, letting other countries deny deductions if the IIR is not applied.

- Qualified Domestic Minimum Top-up Tax (QDMTT): Enables local jurisdictions to tax their entities up to 15% before other countries can step in.

These changes demand a fresh approach to international tax planning for businesses seeking to retain the benefits of territorial systems.

"Pillar Two and the broader global tax deal will ultimately impact US and foreign interests by increasing effective tax rates on cross-border investment, especially by increasing taxes on earnings in low-tax jurisdictions." – Tax Foundation

For U.S.-headquartered companies, the "Side-by-Side" package provides an advantage, exempting qualifying U.S. MNEs from IIR and UTPR if they meet domestic requirements. However, smaller businesses and digital nomads with offshore operations need to stay vigilant. The first GloBE Information Return (GIR) filings for calendar-year taxpayers are due by June 30, 2026, requiring detailed reporting of over 100 data points per jurisdiction.

To prepare, assess whether your group meets the €750 million revenue threshold and identify jurisdictions where your effective tax rate falls below 15%. Take advantage of safe harbors like the "Simplified ETR Safe Harbor" or the "Transitional CbCR Safe Harbor", which has been extended through 2027, to ease compliance burdens. Additionally, ensure thorough documentation of local employees, office leases, and management decisions to meet Pillar Two’s requirements. Substance-based planning is now a critical component for navigating the complexities of territorial tax systems alongside these global minimum tax rules.

Conclusion

Territorial tax systems offer a legitimate way for expats, digital nomads, and entrepreneurs to minimize or even eliminate taxes on foreign income. These systems operate on a simple premise: if you’re a resident in a territorial tax jurisdiction and your income is classified as "foreign", you can legally avoid taxation on those earnings.

However, success in leveraging these systems depends on three key elements: accurate income sourcing, establishing real economic substance, and maintaining thorough documentation. Residency alone isn’t enough. You’ll need to back it up with tangible proof – like a local address, active bank accounts, and time spent physically in the country. Tax authorities now demand verifiable evidence showing where your work is performed, contracts are signed, and business decisions occur. Outdated “paper-only” setups simply won’t cut it anymore.

"Success in territorial tax planning comes not from choosing the lowest tax rate, but from selecting the jurisdiction that best aligns with your long-term strategic objectives." – Project Black Ledger

The rules are tightening. With initiatives like the OECD’s 15% global minimum tax and increased information sharing through agreements such as the Common Reporting Standard, compliance has become non-negotiable. For U.S. citizens, the challenge is even greater due to citizenship-based taxation, which requires careful planning to balance foreign residency benefits with U.S. tax obligations.

In this evolving landscape, a well-documented, substance-driven approach is critical. Territorial tax systems, when used appropriately, remain a powerful tool for preserving wealth. To make the most of these opportunities, clearly define your income sources, establish genuine economic presence, track your physical presence, and seek expert guidance on both local and international tax regulations. By doing so, you can reinvest the money saved on taxes into growing your business – all while staying fully compliant with the law. Territorial tax strategies can be a cornerstone for protecting and growing your wealth.

FAQs

Will I still owe U.S. tax if I move to a territorial tax country?

Moving to a country with a territorial tax system can often mean you won’t be subject to U.S. taxes on income earned abroad. However, as a U.S. citizen, you’re still required to report all worldwide income to the IRS. Depending on your situation, you might still owe taxes unless you qualify for certain provisions, such as the Foreign Earned Income Exclusion (FEIE). To reduce your tax liability legally, it’s crucial to carefully review the eligibility requirements for these exclusions.

How do I prove my income is foreign-sourced?

To demonstrate that your income comes from foreign sources, you’ll need proper documentation. This might include contracts, invoices, bank statements, or payment receipts from entities based outside the U.S. Additionally, you may need to provide evidence of your work location, such as travel records or residency documents. Keeping thorough and organized records is crucial to back up your claim when it comes to taxes.

What counts as “economic substance” for tax purposes?

For tax purposes, economic substance refers to the idea that transactions or arrangements must have a legitimate purpose beyond just reducing taxes. In other words, they should involve real economic activity and align with genuine business operations or investments. If a transaction exists only to dodge taxes without any actual business activity or practical purpose, it typically fails to meet this standard.