May 4, 2015

By: Kelly Diamond, Publisher

Has Obamacare become a worn out subject to you yet? I mean, has it just played out from every angle, and at this point it’s so far gone, you’ve thrown your hands in the air and accepted the fact that it’s here to stay? Nothing you can do.

Has Obamacare become a worn out subject to you yet? I mean, has it just played out from every angle, and at this point it’s so far gone, you’ve thrown your hands in the air and accepted the fact that it’s here to stay? Nothing you can do.

Sorry if I’m projecting my own sentiments on the readers of this article, but on the one hand that’s exactly where I’m at. But on the other, I have something nagging at me saying, “That’s exactly what the politicians were hoping would happen: let the story fizzle out and people will forget about it and integrate it like every other imposition by the government.”

You know we’re never allowed to forget the tragedies that usher in these outrageous policies, right? When the slogan “Never Forget” comes out, you know that scar is being reopened at LEAST once a year. And just as it’s against the unwritten law to attempt to move past 9/11, so is it against the unwritten law to forget about the uninsured. We’re told 43.3 million people were uninsured. That’s approximately 16% of the US population, but that number is considerably smaller than 43.3 million, so we aren’t reminded of that fact: that we turned 1/6 of our economy on its ear for 16% of the population.

No doubt of that 16%, there were some that actually wanted health insurance, but couldn’t afford it. But there was also a percentage of them that didn’t want it at all. Insurance for things like health and cars isn’t worthwhile for incredibly wealthy people because they can afford the out of pocket expense of any incidentals that might come up. It seems pointless to pay a premium when you have the funds to pay for something outright if and when the need arises.

There are also the young and healthy that, at most, might have needed catastrophic coverage for major problems but don’t have long standing issues. They would need car insurance, but maybe a $50/month catastrophic plan. But that wasn’t available as a legal package to buy.

So here we are. Had to pass it to see what’s in it, right? And now that we’ve passed it, we have to wait for a new unveiling of what’s in it every year or so. But with every little “optimization” or tweak made to the law, the Congressional Budget Office (CBO) and the Government Accountability Office (GAO) rerun the numbers. Essentially, what was sold to you at the point of election and what is currently happening or what will happen down the line are very different things.

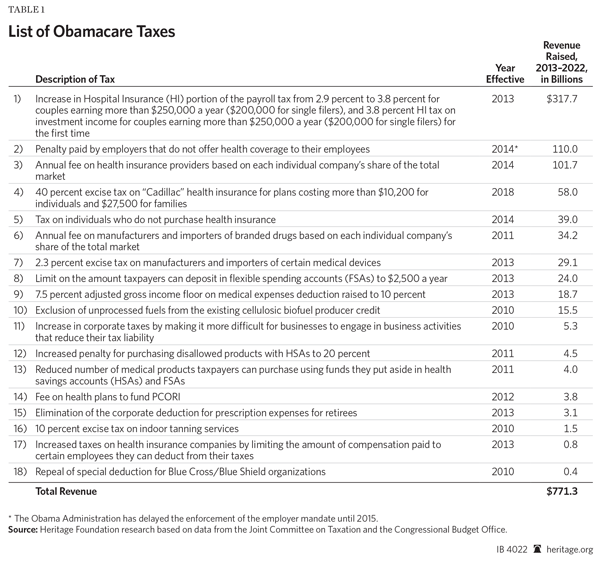

The Heritage Foundation culled through the information available from the Joint Committee on Taxation and the CBO and consolidated their findings into the chart below. It itemizes where the federal government expects to find “revenue” or “funding” to sustainably support the Affordable Care Act.

If you read the items closely, it doesn’t look like a source of revenue as much as it looks like a contingency plan. It relies on a certain percentage of people behaving a certain way. I relies on a certain number of individuals paying the fine/tax for not having insurance. I relies on a certain number of businesses paying the fine over insuring individuals. It relies on cuts to Medicare reimbursements, and assumes people will be okay with it.

Ever take a course in statistics? If you have, you’ll remember those problems that took about 5 to 6 pages to solve. And you’ll also remember the devastation of getting something wrong on page 2 that totally screwed you by page 6. Unlike solving a problem on paper, however, we’re doing this one LIVE. So when someone screws up in 2015, 2020 is wondering what the hell brought on this dystopic nonsense.

Just for a moment, let’s assume everything goes exactly according to plan. The estimated cost of just state level exchange subsidies and the expansion of Medicaid alone is estimated to cost $1.8 TRILLION from 2014 to 2023. It would seem that the bottom line solution to 16% of Americans not having health insurance was to add 10% of Americans to government programs of some sort.

Now let’s assume that things don’t quite go according to plan, but instead go according to how things are going now! According to this January’s CBO report nearly 10 million people will lose their employer-based insurance by 2021; and by 2025 there will still be 31 million people uninsured!

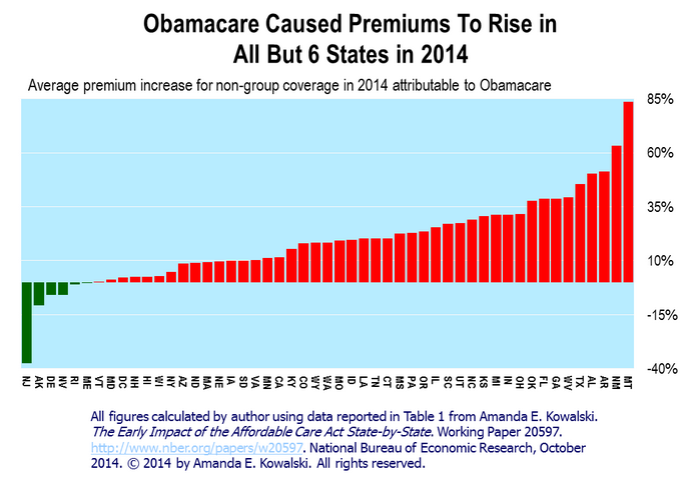

Forbes offered an analysis from the National Bureau of Economic Research that isolated the non-group coverage premiums, and if finance could break your heart, the numbers from this study would do just that. Here are some highlights, but I sincerely invite you to read their entire article as well as the study:

- “In 2014, premiums in the non-group market grew by 24.4% compared to what they would have been without Obamacare.”

- “…[In] nearly one third of states (16), Exchange coverage constitutes 40% or less of the entire non-group market.”

- “…Out of an estimated 13.2 million people covered in the non-group market in second quarter 2014 (Kowalski’s estimate), only about 7 million qualified for subsidies. Thus, there were 6.2 million in the non-group market who had to absorb these premium increases without the benefit of any help from Uncle Sam.”

It appears we have several moving parts that are destined to collide over the next decade. We have one part that represents $1.8 Trillion in costs. We have another part that consists of an unreliable revenue stream of $770 Billion. We have people who are being financially stressed with higher premiums. We have people who are losing their plans and coverage. And we have a senior crowd who won’t tolerate losing coverage or reimbursement under Medicare.

The prognosis would seem to be that more people will be harmed than helped. When I see the give and take of how this is playing out, I think of a Rubik’s Cube: You got all the yellow squares to match up, but the rest of the cube is mismatched, so you have to undo the yellow side to match up the other sides, then you undo what progress was gained on the red side for the blue side, and so forth and so on. The thing is: there is actually a trick to solving the Rubik’s Cube. Those who know it and can do it, compete on when rather than if they can solve it. In the case of Obamacare, they don’t know the trick. In the case of Obamacare, the issue of uninsured Americans was never a problem for the government to solve in the first place, but rather one from which the government should have removed itself.

In conclusion, ask one thing: don’t “get over” Obamacare. I understand it gets tiresome. But just because you won’t see the itemization of the bill you’re paying, doesn’t mean you’re not paying it. Every tax and fine on every medical product or institution gets passed on to you. Every tax on insurance companies is passed on to you. Every person who’s priced out of the market is passed on to you. The anonymity of the bill you and your children will be paying is how they get you to comply. The only thing society can afford LESS than Obamacare is your apathy toward it. I encourage you to find a way to protect yourself, your assets, and your family from the wave of new costs you are likely to face.