February 22, 2016

By: Bobby Casey, Managing Director GWP

This is going to be a two-part series. It is a topic that deserves more than a thousand words, and likewise deserves the attention and consideration of everyone reading it.

This is going to be a two-part series. It is a topic that deserves more than a thousand words, and likewise deserves the attention and consideration of everyone reading it.

For a while now, we’ve been discussing two important things: 1. The war on cash, and 2. the rise of China as the potential reserve rival of the USD.

Much like pox, it starts with one little bump here or a little red blemish there. The average person doesn’t recognize it right off the bat as being pox; rather they dismiss it as a pimple or a bug bite. It’s not until it starts to spread, or when the fevers kick in that people realize what they really have.

If we look back at the first signs of this war on physical money, the introduction of the Federal Reserve, the confiscation of gold in the 1930’s along with the manipulation of its value, and the gradual abandonment of the gold standard were all crucial players on the battle field.

The one thing that stood in the way of the Keynesian runaway train was the lack of technological capabilities to keep up with the money printing desires of the central bankers and politicians. When that barrier was finally torn down, it didn’t take long for them to get accustomed to the ease of a keystroke.

Easy to offer lines of credit since everything is computerized. You might even remember the commercials from the credit card company where the guy paying in cash was growled at by the others in line for slowing things down when he could’ve just been considerate to everyone else and used his card? You can literally borrow and pay back money via app services on your phone. No cash ever need exchange hands.

We were sold this bill of goods as being safer and more convenient. And indeed that claim was not without merit. If your cash gets stolen, you can report it but it never gets replaced. If your card gets stolen, you can report it, and any charges made on it are taken care of by your bank or credit card company. Then a new card is issued straight away. There’s no arguing the fact that toting a little plastic card around is easier than a wad of cash and coins.

Convenience and safety are certainly factors in defining money. And unto themselves, they aren’t bad. Bitcoin certainly offers both of those things, but the one thing it has in its favor is its limited mining ability. Its volume is finite, and the mining process is likewise limited.

It’s not enough to just offer another means of transacting, however. It was meant to replace it. So whereas at one point you had a choice between cash, credit, debit, or check, now it’s just credit, debit, or check… or so is the goal.

We did a piece a while back about food stamps (“See No Evil, Know No Evil”). Back in the 1930’s you could see the physical breadlines of people outside waiting to trade in their stamps for their rations. You’ll notice those lines have become invisible. Despite the record number of people enrolled in the food stamp programs like SNAP and WIC, it was swept under the rug of a debit card of sorts.

There is no denying that there is a different psychological effect when you can use your senses and when you can’t. When you can hold the cash or gold in your hand, and see the actual physical volume, and physically exchange it for something you want or need, versus sliding a card and never feeling your wallet get lighter or experience the physical currency being taken from your hands. If you were to take a fixed amount of cash to the grocery store, and knew that was it, you would be more cautious of what you were putting into the cart. You might take frozen over fresh? Generic over brand? Skip the novelty items like gourmet cheese and smoked salmon? And when you went to pay, you would see with your eyes the money adding up on the register and look at your little envelop of cash… and maybe have to leave some items behind because there still isn’t enough? That’s the difference between a virtual and physical money.

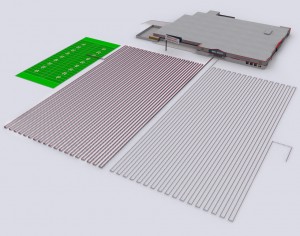

Numbers don’t mean anything until you see what they represent. So over 40 million people on food stamps? What does that mean? It’s just a number, right? Below is a graphic representation of what that number looks like if we were to just line those folks up:

(Right) 6856 SNAP Children per Month, per Walmart Super Center. The bread line is 3.67+ miles (5.9km+) long.

The meaning of 40 million just gained new dimensions, didn’t it?

The same goes for our national debt. That’s just a large line of credit. It’s the US sliding its credit card. Whereas you and I get our credit limits set by our credit card company, the US gets its limit set by the Congress and President. As you know, it was recently suspended until March 2017. It’ll be sitting there for the next president to deal with.

Aside from literally desensitizing people to the pangs of spending – and subsequently compelling them to continuously “stimulate the economy” rather than save – the government has other ulterior motives.

The first of which is to track you and your money.

If there is ONE thing every economically unstable country fears, it’s capital flight and/or a run on the banks. The US is notorious about tracking down that which it feel entitled to (e.g. FATCA). Politicians are rabid about jobs and money leaving the US. They add more and more regulations and penalties to force jobs and money to stay in the US. Obviously, no one ever told them that they can attract more flies with honey than vinegar. Punishment isn’t nearly as effective as reward. Incentives work better than disincentives.

So how do we get people on board the anti-cash train? Seems obvious right? Link the anonymity of cash and hard assets to criminal behavior like money laundering, drug dealing, or *GASP* terrorism. Repeat like a broken record, “if you have nothing to hide, you have nothing to fear”. It’s the same portal that allows for government spying: “nothing to hide, nothing to fear”. This is how we’ve transitioned to a presumption of guilt, rather than innocence.

Then, when you see people dealing in cash, you presume it’s for criminal purposes. Driving with too much cash in your car? The cash is guilty of being involved in a drug related crime. Enter asset forfeiture. Withdrawing or depositing too much cash? You must be up to something. As we discussed, this is already the position Sweden has taken in its race to become the first fully cashless society. Louisiana has put some restrictions on its cash transactions as well.

Going cashless in the American and European contexts is about control: capital controls, social engineering, tracking people’s goings, all of it. Abandoning cash isn’t bad advice, just put it into something a little more stable. Let’s discuss some options! Click here to set up an appointment.