High taxes and sudden policy changes are driving wealthy entrepreneurs to relocate. Countries like Denmark, Finland, France, Portugal, and Belgium impose some of the world’s steepest tax burdens, including income taxes exceeding 50%, corporate taxes as high as 36%, and additional levies on wealth, unrealized gains, and property. These policies are prompting many to seek low-tax jurisdictions like the UAE or Cayman Islands, which offer 0% income and corporate taxes alongside strong asset protection.

Key Points:

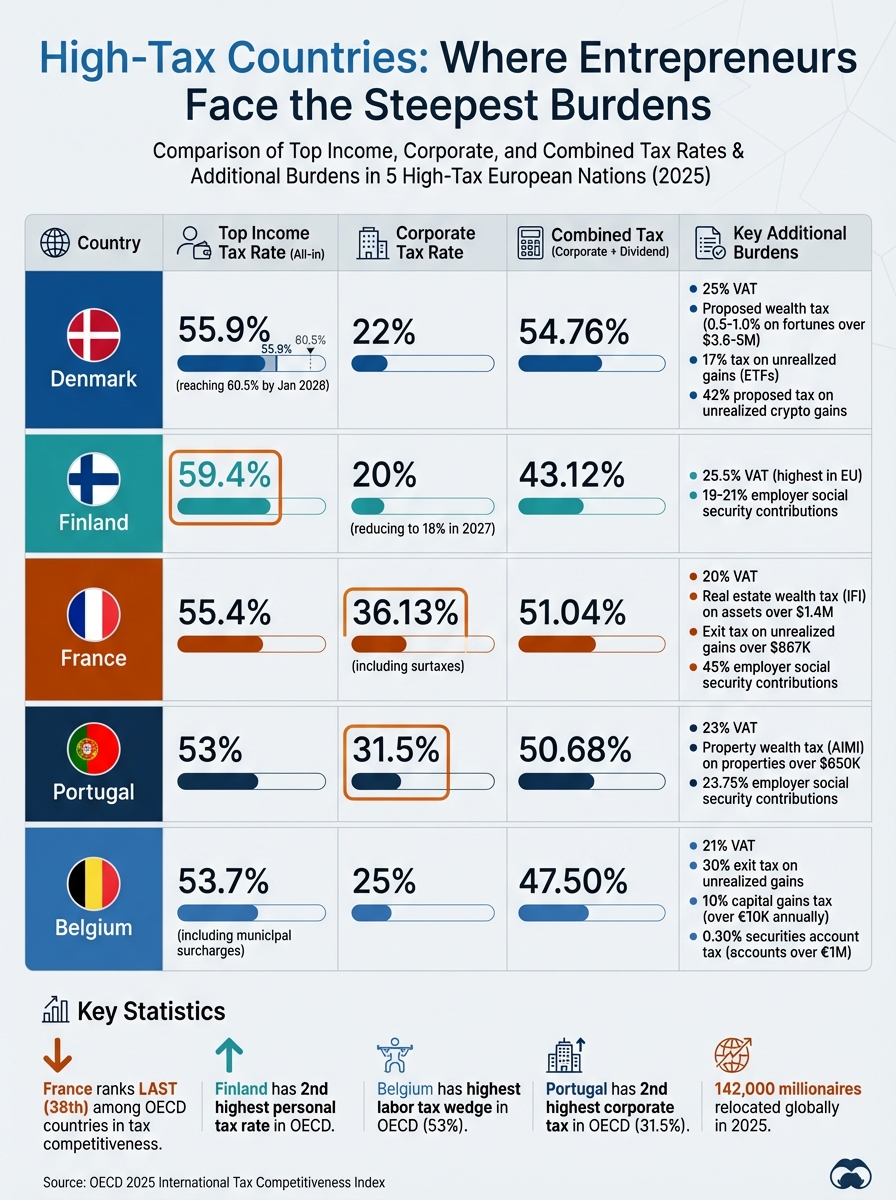

- Denmark: Top income tax of 60.5%, a proposed wealth tax, and high taxes on unrealized gains.

- Finland: Personal tax rates up to 59.4% and a 25% VAT.

- France: Combined corporate and dividend tax over 51% and real estate wealth taxes.

- Portugal: Corporate tax rates up to 31.5% and high social security contributions.

- Belgium: Top income tax of 53.7%, new capital gains taxes, and a 30% exit tax.

Quick Takeaway:

High taxes are pushing entrepreneurs to relocate to tax-friendly countries with predictable policies. By 2025, 142,000 millionaires moved globally, with many heading to low-tax havens.

1. Denmark

Income Tax Rates

Denmark uses a progressive tax system, with the top marginal rate on labor income set to reach 60.5% in January 2026. This figure includes an 8% labor market tax deducted from gross income. This high rate applies to earnings over 2,592,700 DKK (around $375,000).

For entrepreneurs, these tax rates can have a substantial impact, especially when their income comes from dividends or successful business exits. The steep tax rates significantly reduce net earnings, making financial planning more challenging.

One exception is the Researcher Tax Scheme, also known as the Expat Scheme. This program offers qualifying foreign professionals a flat tax rate of 32.84% for up to seven years. In 2026, Denmark reduced the minimum monthly salary requirement for this scheme from 78,000 DKK to 65,400 DKK to attract international talent. However, this benefit is not available to local entrepreneurs.

Adding to these challenges, Denmark’s corporate tax structure further complicates the financial landscape for business owners.

Corporate Tax Rates

Denmark’s corporate tax rate stands at 22%, aligning closely with the OECD average. While this rate seems competitive, the personal taxes on profit distributions remain high, creating a stark contrast. For financial companies, the effective tax rate increases to 26%, while businesses in the hydrocarbon extraction sector face a combined rate of 64%. Additionally, dividends paid to companies in EU-blacklisted jurisdictions are hit with a 44% withholding tax.

These factors often push entrepreneurs toward jurisdictions with more favorable tax policies.

Additional Tax Burdens

Beyond income and corporate taxes, Denmark imposes other significant fiscal pressures. A high VAT and one of the highest tax-to-GDP ratios in the world add to the burden. In February 2026, Prime Minister Mette Frederiksen proposed reintroducing a wealth tax, which had been abolished in 1997. This tax would target the wealthiest 1%, applying an annual rate of 0.5% to 1.0% on net fortunes exceeding 25 to 35 million DKK (roughly $3.6 to $5 million). The government estimates this would generate 6 billion DKK annually from fewer than 14,000 individuals.

"When the wealthiest one percent of the population owns around a quarter of Danes’ total net wealth, the imbalance has become too great." – Mette Frederiksen, Prime Minister of Denmark

Denmark also taxes unrealized gains on certain assets. For example, equity ETFs and stock savings accounts face a 17% annual tax on paper gains. There are also proposals to apply a 42% tax rate on unrealized cryptocurrency gains. For entrepreneurs holding illiquid shares, these taxes can create liquidity issues, as they may need to extract cash to cover taxes on gains they haven’t realized.

Entrepreneurial Impact

The combination of high personal tax rates and the proposed wealth tax has led some entrepreneurs to consider relocating. Cecilie Jacobsen, founder and CEO of wawa fertility, expressed concern:

"If Denmark introduces additional structural friction for founders, we would find it difficult to recommend other founders start companies here."

Research from the OECD indicates that for every dollar raised through a wealth tax, 76 cents are lost due to migration. Denmark’s Economic Councils estimate that about one-third of high-income earners may reclassify income to reduce their tax burden.

For entrepreneurs looking to relocate, Denmark’s exit tax on unrealized gains can be deferred indefinitely if they move within the EU or Nordic region. This has made Sweden an attractive option. Sweden abolished its wealth tax in 2007 and has since experienced a "billionaire boom", with 2.0 billionaires per million inhabitants compared to 0.46 in France. As Denmark approaches its March 24, 2026 election, which will decide the fate of the wealth tax, many entrepreneurs are closely monitoring these developments.

sbb-itb-39d39a6

2. Finland

Income Tax Rates

Finland uses a dual income tax system that separates earned income from capital income. As of 2026, reforms have lowered the top marginal rate on earned income to 52%, which combines state tax, municipal tax (averaging 7.57%), and social security contributions (around 9.17%). This results in an effective personal tax rate of approximately 59.4%, making it the second-highest among OECD countries, just behind Belgium. The state tax structure is progressive, starting at 12.64% for income above about $24,000 (€22,000) and reaching 44.25% for earnings over roughly $169,000 (€155,000). Municipal taxes vary widely, ranging from 4.70% in some areas to 10.90% in rural regions. For capital income, a flat 30% rate applies to amounts up to about $32,700 (€30,000), with a higher rate of 34% for income exceeding that threshold.

For foreign specialists, Finland offers a "Key Employee" tax regime with a flat 25% rate for up to seven years, reduced from 32% as of January 2026. To qualify, individuals must earn at least $6,300 (€5,800) per month and apply within 90 days of starting their job.

Corporate Tax Rates

Finland’s corporate income tax rate is currently 20%, with plans to reduce it to 18% starting January 2027 to encourage business investments. Dividends between Finnish companies are typically tax-exempt, but individual shareholders face capital gains tax rates of 30% to 34% when withdrawing profits.

These policies create a balancing act for entrepreneurs, who must weigh the competitive corporate tax rates against the high personal tax burden.

Additional Tax Burdens

Finland’s Value-Added Tax (VAT) stands at 25.5%, one of the highest rates in the EU. Church members pay an additional 1% to 2.25%, though this can be avoided by leaving the church. While Finland does not impose a net wealth tax, it does levy estate and inheritance taxes. The inheritance tax threshold was raised to about $32,700 (€30,000) as of January 2026. Employers are also required to contribute approximately 19% to 21% of gross wages for social security.

Entrepreneurial Impact

Finland’s steep personal tax rates can pose challenges for entrepreneurs. To address this, the government has introduced several targeted incentives. These include a 150% R&D super-deduction for research partnerships (available through 2027), a 20% tax credit for large-scale green investments aimed at achieving net-zero goals, and an extension of the loss carryforward period from 10 years to 25 years starting in 2026.

Kaija Laitinen, Senior Advisor at Invest in Finland, highlights the government’s supportive approach:

"Finland’s tax system includes several targeted incentives designed to support companies at every stage of growth. This approach promotes innovation and long-term success."

Despite these incentives, Finland dropped to 24th place on the 2025 International Tax Competitiveness Index, falling six spots compared to the previous year. However, startup investment surged to around $1.5 billion (€1.4 billion) in 2024 – a 56% jump from 2023.

Next, we’ll examine how Finland’s tax policies and incentives compare to those in other high-tax jurisdictions, shedding light on potential relocation advantages.

3. France

France faces challenges similar to other high-tax countries, as its tax policies often drive entrepreneurs to seek opportunities elsewhere.

Income Tax Rates

France employs a progressive income tax system with five brackets ranging from 0% to 45%. For 2026, these brackets were adjusted upward by 0.9% to account for inflation. The top 45% rate kicks in at around $197,000 (€181,917) per share of household income. The Quotient Familial system helps mitigate tax burdens for families by dividing household income among family members, effectively lowering the tax rate.

However, high earners face additional taxes. The "Contribution exceptionnelle sur les hauts revenus" (CEHR) adds 3% to 4% to their tax bill, while the "Contribution Différentielle sur les Hauts Revenus" (CDHR) ensures that anyone earning over $271,000 (€250,000) pays a minimum effective tax rate of 20%.

Overall, labor taxes in France are steep, with a combined burden of around 47%, one of the highest in the OECD. In 2022, France’s tax-to-GDP ratio stood at 46.1%, far above the OECD average of 34%. Social contributions, including the CSG (9.2%) and CRDS (0.5%), further increase deductions, bringing total payroll taxes to between 22% and 25% of gross salary.

Corporate Tax Rates

The standard corporate tax rate in France is 25%, but additional surtaxes for large corporations push the effective top rate to 36.1% – the highest in the OECD and significantly above the average of 24.2%. As Alex Mengden, a Policy Analyst at the Tax Foundation, remarked:

"France manoeuvred itself to the bottom of the Index by implementing several surtaxes on large corporations that temporarily hike its top marginal corporate tax rate to 36.1%, the highest rate in the OECD."

Under the 2026 Finance Act, these surtaxes were extended for two more years. Companies with revenues between $1.6 billion and $3.3 billion (€1.5 billion and €3 billion) are subject to a 20.6% surcharge, resulting in an effective tax rate of about 31%. For companies exceeding $3.3 billion (€3 billion) in revenue, the surcharge rises to 41.2%, pushing their effective rate to around 36%. Additionally, a 20% tax applies to luxury assets such as yachts, aircraft, and high-end cars owned by holding companies.

These corporate tax policies significantly increase the cost of doing business in France.

Additional Tax Burdens

France also imposes a standard VAT of 20%, along with a real estate wealth tax (IFI) on net property assets exceeding $1.4 million (€1.3 million), with rates ranging from 0.5% to 1.5%. An exit tax applies to unrealized gains on assets worth more than $867,000 (€800,000). Luxury assets like yachts and art are taxed at a flat 1%.

Employer social security contributions average 45% of gross pay, significantly higher than the European norm, making labor costs a heavy burden for businesses.

Entrepreneurial Impact

France’s tax policies have a direct impact on wealth migration and business decisions. The country ranks last (38th) among OECD nations in the 2025 International Tax Competitiveness Index, scoring just 45.8 compared to Estonia’s perfect 100. Between 2000 and 2017, about 60,000 millionaires left France, and capital flight between 1988 and 2007 amounted to roughly $217 billion (€200 billion).

Former Finance Minister Bruno Le Maire openly acknowledged the issue:

"Overtaxing capital had led to more investors and creators of wealth leaving."

Current Economy and Finance Minister Roland Lescure echoed similar concerns, cautioning against unilateral wealth tax measures:

"If we do it by ourselves, we’re going to have what is happening in the UK: we’re going to have people fleeing and going elsewhere."

French businesses also carry an annual tax burden that exceeds their European counterparts by $136 billion (€125 billion). High-income rental property owners face a total tax rate of up to 66.2%, factoring in the 45% top income tax bracket, 4% exceptional contribution, and 17.2% social contributions.

While setting up a business in France takes only five days on average, this efficiency pales in comparison to Estonia, where it can be done in just 18 minutes.

4. Portugal

Portugal presents a mixed tax landscape for wealthy entrepreneurs. On one hand, the government has been lowering corporate tax rates to attract investment. On the other, high earners face steep tax obligations comparable to those in other European nations. This duality is prompting many entrepreneurs to rethink their fiscal residency in search of better asset protection and financial predictability.

Income Tax Rates

Portugal operates on a progressive income tax system, with rates ranging from 12.5% to 48%. Starting in 2026, individuals earning up to $998 (€920) per month are exempt from income tax due to an updated minimum subsistence level of $13,967 (€12,880). High earners, however, face additional "solidarity surcharges", which push the top rate to 53%. These surcharges include a 2.5% levy on middle-income brackets and 5% on higher earnings. This places Portugal among the least competitive tax systems in Europe, ranking 33rd out of 38 OECD countries on the 2025 International Tax Competitiveness Index. Social security contributions further add to the burden, with employees paying 11% and employers contributing 23.75%, with no cap on payments.

Corporate Tax Rates

Portugal has been gradually reducing its corporate tax rate, dropping from 20% in 2025 to 19% in 2026, with plans to lower it further to 18% and 17% in subsequent years. Small and medium-sized businesses benefit from a reduced rate of 15% on the first $54,200 (€50,000) of taxable income starting in 2026.

However, the effective corporate tax rate can climb significantly due to various surtaxes. The top effective rate currently stands at 31.5%, making it the second-highest in the OECD. Alex Mengden, an economist at the Tax Foundation, explains:

"Portugal has the second highest top corporate tax rate in the OECD at 31.5 percent, including multiple top-up taxes. This puts Portugal’s corporate tax rate 8 percentage points above the OECD average of 23.6 percent."

Additional taxes include state surtaxes of 3% to 9% on profits exceeding $1.6 million (€1.5 million) and municipal surcharges of up to 1.5%. The Autonomous Region of Madeira offers a more competitive alternative, with a proposed general rate of 13.3% for 2026 and a 5% rate for companies within the Madeira International Business Centre.

Additional Tax Burdens

Portugal’s Value Added Tax (VAT) rate is 23%, ranking among the highest in Europe and accounting for 37.3% of the country’s total tax revenue. While Portugal does not impose a wealth tax on financial assets, it does levy AIMI (Adicional ao IMI), a property wealth tax targeting high-value real estate. Properties valued above $650,600 (€600,000) are taxed at rates between 0.7% and 1.5%, though married couples filing jointly enjoy a higher exemption threshold of $1.3 million (€1.2 million).

Inheritance tax was abolished in 2004 for direct heirs, such as spouses, children, and parents. However, a 10% Stamp Duty applies to assets transferred to non-direct heirs.

These tax layers not only increase complexity but also shape how entrepreneurs conduct business and plan their financial strategies.

Entrepreneurial Impact

Portugal’s tax system is a double-edged sword for entrepreneurs. On one hand, the country offers some of the most generous R&D incentives in the OECD, with a 35% implicit subsidy rate on qualifying expenses. This makes it particularly appealing for tech startups and innovation-driven businesses. On the other hand, the overall tax structure – marked by high rates and numerous surcharges – often drives wealthy entrepreneurs to seek more predictable tax environments.

Despite these challenges, Portugal has become a hub for startups, boasting thousands of companies in its ecosystem. However, its ranking of 37th out of 38 countries on the 2023 International Tax Competitiveness Index highlights the strain imposed by its layered tax system. The once-popular Non-Habitual Resident (NHR) regime closed to new applicants in January 2024, replaced by the more restrictive IFICI (NHR 2.0). This new program offers a flat 20% tax rate for 10 years, but only for highly qualified professionals in fields like research, innovation, and high-tech sectors.

Portugal’s tax landscape reflects broader trends seen in other high-tax jurisdictions, setting the stage for further comparisons in upcoming discussions.

5. Belgium

Belgium is known for its challenging tax landscape, particularly for wealthy entrepreneurs. With high personal income taxes and new measures targeting wealth, both earnings and assets face significant pressure. These factors are causing many entrepreneurs to reconsider their fiscal residency in favor of more predictable tax regimes.

Income Tax Rates

Belgium’s progressive income tax system starts at 25% and climbs to 50%. When municipal surcharges (ranging from 0% to 9%) are factored in, the effective top rate reaches 53.7%. This positions Belgium among the highest-taxed nations globally, ranking fifth for personal income tax rates.

The labor tax burden is even more striking. Belgium has the highest labor tax wedge in the OECD, standing at 53% for an average single worker. This figure includes income tax and social security contributions, with employers covering roughly 35% and employees contributing 13.07%. Alex Mengden, a Policy Analyst at the Tax Foundation, commented:

"Belgium has manoeuvred itself to the bottom of the Index… the Belgian tax wedge on labor is the highest among the OECD countries."

Starting January 1, 2026, Belgium implemented a capital gains tax that significantly alters the taxation of private wealth. Gains on financial assets like listed shares, bonds, and crypto-assets are taxed at 10% if they exceed $10,850 (€10,000) annually. For major shareholdings exceeding 20% of a company, progressive rates from 1.25% to 10% apply after a $1.08 million (€1 million) exemption. DLA Piper highlighted the importance of this reform:

"This comprehensive reform, effective as of 1 January 2026, constitutes a fundamental shift in Belgian personal income taxation. Capital gains realized within the ‘normal management of private wealth’ will, for the first time, become taxable on a broad scale."

Additionally, an exit tax introduced in mid-2025 targets entrepreneurs relocating abroad. This tax treats company emigration as a "deemed dividend" distribution, immediately imposing a 30% tax on unrealized capital gains, even without an actual cash distribution.

Corporate Tax Rates

Belgium’s corporate income tax system includes a standard rate of 25%, with a reduced 20% rate available for small and medium-sized enterprises on their first $108,500 (€100,000) of taxable profit. However, companies must meet specific conditions to qualify for the lower rate, such as paying at least one director a minimum salary of $54,250 (€50,000).

For the 2026 tax year, a 6.75% surcharge applies to the final corporate tax amount, though businesses can avoid this by making sufficient advance tax payments. Additionally, the "basket rule" limits deductions for companies with profits exceeding $1.08 million (€1 million), ensuring a minimum taxable base even if they have carried-forward losses.

Additional Tax Burdens

Belgium applies a standard Value Added Tax (VAT) rate of 21%, with reduced rates of 6% and 12% for certain goods and services. Dividend, interest, and royalty payments face a standard withholding tax of 30%, which can complicate profit distributions.

The annual tax on securities accounts increased from 0.15% to 0.30% in 2026 for accounts valued above $1.08 million (€1 million). While Belgium does not impose a broad wealth tax, this levy functions similarly for individuals with large investment portfolios.

Entrepreneurial Impact

Belgium’s tax system creates a heavy burden for entrepreneurs, combining a high top income tax rate, the steepest labor tax wedge in the OECD, and the new 2026 capital gains tax on private wealth. Together, these factors contribute to Belgium’s 30th overall ranking on the 2025 International Tax Competitiveness Index.

Although Belgium offers incentives for research and development – such as an 85% Innovation Income Deduction and an 80% wage withholding tax exemption for scientific researchers – the broader tax environment remains a deterrent. The introduction of the exit tax adds further complexity, making it costly for entrepreneurs to relocate their businesses abroad. As a result, many high-net-worth individuals and business owners are increasingly drawn to jurisdictions with more favorable tax policies.

Tax Policy Comparison: Benefits and Drawbacks

Countries like Denmark, Finland, France, Portugal, and Belgium impose notably high tax rates, which can significantly impact entrepreneurial wealth. For example, Finland’s personal tax rate tops out at 59.4%, while Portugal’s corporate tax rate sits at 31.5%, far exceeding the EU average of 21.27%.

These high-tax systems are designed to fund universal services and promote income redistribution. However, they come with a downside: high marginal tax rates can hinder growth by taxing entrepreneurs on unrealized gains. Fredrik Haga, co-founder of Dune, highlighted this challenge:

"This so-called wealth tax meant that I faced a tax bill many times larger than my after-tax income. The only way to pay it was to sell shares and dilute my ownership in my company".

The following table provides a snapshot of key tax metrics across these countries:

| Country | Top Marginal Income Tax (All-in) | Corporate Tax Rate | Combined Tax (Corp + Dividend) | Key Additional Burdens |

|---|---|---|---|---|

| Denmark | 55.9% | 22% | 54.76% | 25% VAT |

| Finland | 59.4% | 20% | 43.12% | – |

| France | 55.4% | 36.13% | 51.04% | Real estate wealth tax (IFI) |

| Portugal | 53% | 31.5% | 50.68% | – |

| Belgium | 53.5% | 25% | 47.50% | Securities account tax (accounts > €1M) |

The combined tax rate – which includes both corporate profit and dividend taxes – offers a clearer picture of the overall tax burden on entrepreneurs. For instance, France’s combined rate of 51.04% reflects its upcoming corporate tax hike from 25.83% in 2024 to 36.13% in 2025. Business owner Knut-Erik Karlsen also shared his perspective:

"The wealth tax system makes it harder for companies to compete with the rest of the world".

These comparisons underline how high tax burdens can push entrepreneurs to seek friendlier fiscal environments elsewhere.

Low-Tax Jurisdictions for Relocation

With high-tax domestic regimes pushing entrepreneurs to seek alternatives, low-tax jurisdictions are becoming increasingly attractive. These destinations, like the Cayman Islands and the British Virgin Islands (BVI), offer tax frameworks with 0% personal income tax, 0% corporate tax, and no capital gains or inheritance taxes [83–85]. For many business structures, relocating to these regions can entirely eliminate tax burdens.

But it’s not just about reducing taxes. These jurisdictions also provide strong asset protection, a critical factor for entrepreneurs who value international mobility.

In 2025, approximately 142,000 high-net-worth individuals migrated to new countries, with a notable number heading to tax-neutral havens. The Cayman Islands, for instance, host over 99,000 registered companies, including nearly 300 banks and 10,500 mutual funds. Similarly, the BVI boasts a staggering number of registered companies – more than 1,000% more than its population.

Asset Protection and Tax Benefits

Beyond tax savings, these locations offer robust tools for safeguarding wealth. In the Cayman Islands, foundations and trusts help separate business assets from personal wealth, protecting them from creditors and simplifying succession planning. Additionally, exempt companies in the Caymans can secure Tax Exemption Certificates, guaranteeing tax-free status for up to 30 years.

As Jeremy Savory, founder of Millionaire Migrant, notes:

"More people are rethinking traditional wealth hubs like the UK and China, while places like Portugal, the UAE, and Singapore are surging in popularity".

Meeting Compliance and Residency Requirements

Relocating to these jurisdictions isn’t without its challenges. Entrepreneurs must meet economic substance requirements, which often include appointing local directors, maintaining physical offices, and holding regular board meetings to comply with global standards. For example:

- A Substantial Business Presence certificate in the Cayman Islands costs around $6,000.

- Permanent residency in the Cayman Islands requires a $2.4 million real estate investment.

- The UAE offers 0% personal income tax with its Golden Visa residency program, but annual setup costs range between $4,000 and $10,000.

To maximize benefits, it’s crucial to establish residency before a major liquidity event or a high-income year. Obtaining a Tax Residency Certificate (TRC) activates double taxation treaty benefits and demonstrates your status to foreign tax authorities. Keeping detailed records – such as entry/exit stamps, utility bills, and local bank statements – helps solidify your residency and defend against potential challenges from your prior tax jurisdiction.

This growing trend highlights how entrepreneurs are leveraging global opportunities to optimize their tax strategies and protect their assets.

Conclusion

The movement of wealthy entrepreneurs away from high-tax countries is picking up speed. By 2026, it’s projected that 165,000 millionaires will relocate internationally, a jump from 142,000 in 2025. Additionally, 35% of high-net-worth individuals are actively considering moving themselves or their assets to jurisdictions with lower tax burdens. This trend highlights a growing shift in how entrepreneurs view geography – not just as a place to live, but as a strategic tool for financial planning.

Countries like the UK, where capital gains tax for higher-rate taxpayers increased from 20% to 24% and non-domicile rules were scrapped, have created an environment of tax uncertainty. In contrast, jurisdictions such as the UAE and Cayman Islands are gaining attention for their lower taxes, legal stability, and strong asset protection frameworks. These features make them attractive destinations for those looking to safeguard and grow their wealth.

"Millionaire migration isn’t a vanity metric. It’s a leading indicator of future capital, innovation, and talent concentration".

– Lila Jones, Senior Business News Editor at CEOWORLD Magazine

The numbers tell a compelling story. In 2025 alone, the UAE welcomed 9,800 millionaires, while the UK saw an exodus of approximately 16,500. These figures emphasize the importance of strategic planning for relocation.

For entrepreneurs, careful preparation is essential. Steps like establishing residency before a major liquidity event, obtaining a Tax Residency Certificate to leverage treaty benefits, and maintaining thorough documentation (such as utility bills, travel records, and bank statements) are critical for ensuring compliance and maximizing benefits.

The real question isn’t whether this migration will continue – it’s which entrepreneurs will seize the opportunity to benefit from these shifts.

FAQs

What taxes can affect me if I move abroad?

If you decide to move abroad, it’s important to know that you may still be required to pay U.S. taxes on your worldwide income. This includes earnings such as wages, dividends, interest, capital gains, pensions, and distributions from trusts. On top of that, if you renounce your U.S. citizenship or give up long-term residency, you could also be subject to an exit tax on your assets.

How do I prove I’m a tax resident in my new country?

To establish tax residency in a new country, you’ll generally need to show specific documents like a residence permit, visa, or evidence of your physical presence. This could include things like lease agreements or utility bills tied to your name and address. Many countries also have a rule requiring you to stay within their borders for a set number of days each year – 183 days is a common benchmark.

Beyond this, you might need to register with the local tax office and secure a tax identification number or a residency certificate to finalize your status.

When should I relocate if I’m planning a business exit?

To get the most out of tax benefits and safeguard your assets, it’s wise to relocate before starting the process of exiting your business. This is particularly crucial if you anticipate large capital gains or hefty tax obligations. Many business owners choose to move to states or regions with lower tax rates or more lenient policies. By planning ahead, you can take advantage of more favorable tax conditions and optimize your financial strategies.