Dubai’s reputation as a tax-free haven is no longer entirely accurate. While personal income remains untaxed, businesses face increasing tax obligations. Since June 2023, corporate profits exceeding AED 375,000 ($102,000) are taxed at 9%. Additionally, a 5% VAT (introduced in 2018), property transfer fees, and compliance costs further complicate the financial landscape. Free Zones offer tax benefits, but they come with strict conditions, such as maintaining economic substance and limiting non-qualifying income. Failure to meet these rules can lead to penalties and higher tax rates. For multinational enterprises, a 15% minimum tax applies under new global standards. Navigating Dubai’s tax system now requires careful planning to minimize liabilities and stay compliant.

Corporate Taxes in the UAE

In June 2023, the UAE introduced Federal Decree-Law No. 47 of 2022, signaling the end of its zero-corporate-tax era. This new tax framework applies to nearly all commercial activities, aligning the UAE with OECD standards on Base Erosion and Profit Shifting. Whether you’re running a small business from home or managing a Free Zone entity, you now fall under the definition of a "Taxable Person" and must register with the Federal Tax Authority (FTA). Let’s break down the key tax rates and rules that could affect your business.

Tax Rates and Income Thresholds

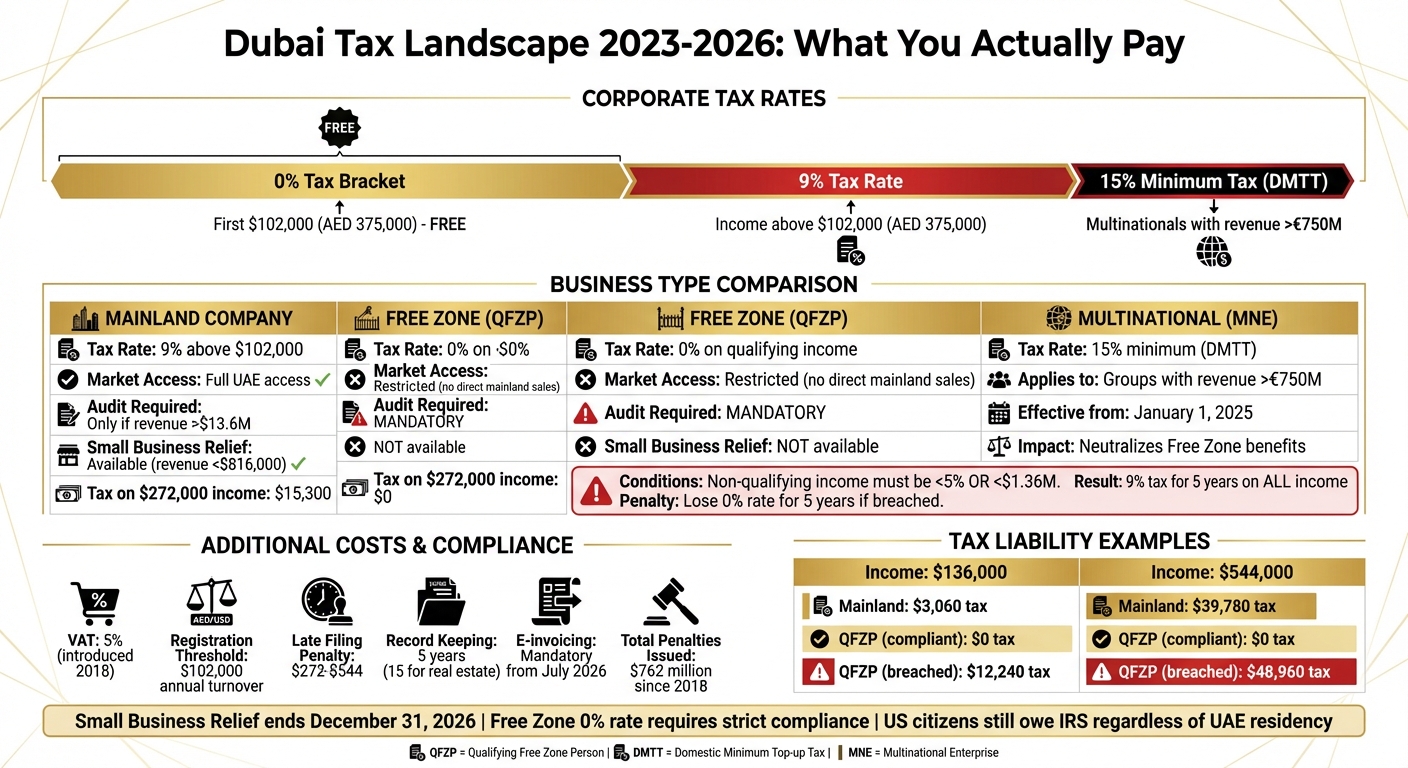

Here’s how the tax rates work: the first $102,000 (AED 375,000) of taxable income is tax-free. Income exceeding this threshold is taxed at 9%. For instance, if your taxable income is $150,000, you’ll owe approximately $4,320 in taxes on the amount over $102,000.

The UAE also offers Small Business Relief (SBR) until December 31, 2026. If your gross revenue stays below $816,000 (AED 3 million), you can be treated as having zero taxable income. However, SBR doesn’t exempt you from registering with the FTA. You’re still required to file annual returns, and failing to register on time will result in penalties.

Permanent Establishment Rules

Your operational structure plays a crucial role in determining tax liability. A Permanent Establishment (PE) is triggered if a foreign business has a fixed base in the UAE or a representative with the authority to conduct business on its behalf. In such cases, the related income becomes subject to the 9% tax rate.

"A foreign person will have a Permanent Establishment in the UAE if: It has a fixed or permanent place in the UAE through which the business of the foreign person is carried on; or There is a person who has and habitually exercises an authority to conduct business in the UAE on behalf of the foreign person." – Maheshwari & Co.

On the other hand, if you work through an independent agent who serves multiple clients and isn’t economically tied to your business, you’re generally safe from PE status. However, if your agent essentially acts as an extension of your company, this could trigger the 9% tax.

Free Zone Tax Exemptions

Free Zones in the UAE offer enticing tax benefits, but there are strict conditions for maintaining these perks. Companies in Free Zones can enjoy a 0% tax rate on "Qualifying Income", but this isn’t granted automatically. To qualify, businesses must meet specific economic substance requirements, such as maintaining minimum staffing levels and operational expenditures. Additionally, non-qualifying income must stay below the lower of $1.36 million (AED 5 million) or 5% of total revenue, and audited financial statements are mandatory.

Some activities, like banking, insurance (excluding reinsurance), and mainland real estate ownership, are excluded and taxed at 9% regardless of Free Zone status. If you fail to meet the qualifying conditions, you lose the 0% tax rate for the current year and the next four years, with all income taxed at 9%.

| Feature | Mainland Company | Qualifying Free Zone Person (QFZP) |

|---|---|---|

| Tax Rate | 9% above $102,000 (AED 375,000) | 0% on Qualifying Income |

| Market Access | Full access to the UAE market | Restricted mainland access |

| Audit Requirement | Based on revenue/legal form | Mandatory for 0% rate |

| Small Business Relief | Available (if gross revenue < $816,000) | Not available |

If a Free Zone company establishes a mainland presence – such as opening a retail shop or hiring a dependent agent – it creates a PE. Any income from mainland activities will then be taxed at 9%. The key takeaway? Free Zone tax advantages come with strict rules, and staying compliant is essential to keep these benefits intact.

sbb-itb-39d39a6

VAT and Compliance Costs

The UAE’s 5% VAT, introduced on January 1, 2018, brings costs that many businesses might underestimate. This consumption tax applies to a wide range of goods and services, including retail products, utilities, professional services, and commercial property leases. While the rate may seem low compared to other regions, the associated compliance costs – like penalties, record-keeping, and adapting to digital requirements – can add up quickly. Let’s break down how VAT registration, filing obligations, and compliance measures can impact your business operations.

The 5% VAT System

The VAT system uses a credit-offset mechanism. Businesses charge 5% VAT on sales (output tax) and deduct the VAT paid on business purchases (input tax), paying the net difference to the Federal Tax Authority (FTA). Most goods and services, such as retail items, food, utilities, and commercial property transactions, fall under the standard 5% rate. However, there are exceptions:

- Zero-rated supplies: These include exports outside the GCC, international transportation, and the first sale of new residential properties within three years of completion. For these, businesses can recover input VAT.

- Exempt supplies: Items like residential leases, bare land sales, local passenger transport (e.g., taxis, buses, metro), and certain financial services are VAT-exempt. Input VAT on related expenses here cannot be reclaimed. For instance, if you lease residential apartments, the VAT paid on maintenance services becomes a direct cost, reducing profit margins.

Registration and Filing Requirements

Efficient VAT management starts with meeting registration and filing obligations. Businesses must register for VAT if their taxable supplies and imports exceed $102,000 (AED 375,000) in the previous 12 months or are expected to surpass this threshold within the next 30 days. Voluntary registration is an option for businesses with turnover or taxable expenses over $51,000 (AED 187,500), allowing them to reclaim input VAT. Missing the registration deadline can result in a hefty $2,720 (AED 10,000) penalty.

Once registered, businesses must submit VAT returns (Form 201) and payments by the 28th day of the month following the tax period’s end. Filing frequency varies based on turnover:

- Small and medium-sized businesses typically file quarterly.

- Companies with an annual turnover above $40.8 million (AED 150 million) usually file monthly.

Late filing penalties range from $272 for a first offense to $544 for repeated violations within 24 months. Additionally, businesses must maintain VAT-related records – like invoices, credit notes, and import/export documents – for at least five years, or 15 years for real estate transactions. Failure to keep proper records can result in fines of $2,720 (AED 10,000) for the first offense and $5,440 (AED 20,000) for subsequent violations.

Additional Compliance Costs

Compliance extends beyond filing requirements, adding layers of complexity and expense. Since the VAT system’s introduction, the FTA has issued over $762 million (AED 2.8 billion) in penalties, with registration-related errors accounting for about 35% of these fines. Starting in July 2026, the UAE will begin mandatory e-invoicing, initially targeting large taxpayers before rolling it out to smaller businesses in 2027. Companies with a turnover above $13.6 million (AED 50 million) will need to adopt e-invoicing first, with non-compliance penalties reaching up to $1,360 (AED 5,000).

To meet these requirements, businesses must upgrade their accounting systems to generate electronic invoices in formats like XML or JSON, compatible with the FTA’s Peppol 5-corner model. Beyond system upgrades, other compliance costs include hiring tax agents, conducting VAT health checks, and maintaining detailed administrative records. Errors exceeding $2,720 (AED 10,000) require filing Form 211 within 20 business days to minimize penalties.

Navigating these compliance challenges demands careful planning and a clear understanding of VAT rules to prevent unnecessary costs and penalties. As the UAE’s financial regulations evolve, staying informed and prepared is essential for effective VAT management.

Free Zone Benefits vs. Limitations

When diving into VAT compliance complexities, it’s worth comparing the perks of Free Zones with mainland taxation. While Free Zones have long been seen as tax-friendly havens, the reality is evolving. By 2026, the widely discussed 0% corporate tax rate will no longer be automatic. Instead, businesses must meet Qualifying Free Zone Person (QFZP) criteria, which include maintaining proper economic substance, limiting non-qualifying income, and adhering to strict regulations. Failing to meet these conditions can lead to steep penalties, turning potential tax savings into unexpected costs.

Free Zone vs. Mainland Taxation

The tax landscape for Free Zones versus mainland companies hinges on whether your business can maintain QFZP status. Mainland entities face a 9% corporate tax on profits exceeding $102,000 (AED 375,000), while QFZPs enjoy a 0% rate on qualifying income – provided they meet the stringent conditions. However, non-qualifying income for QFZPs is taxed at 9% from the first dollar, with no exemptions.

To secure the 0% tax rate, Free Zone entities must ensure their non-qualifying revenue remains below the de minimis threshold: the lower of 5% of total revenue or $1.36 million (AED 5 million). Exceeding this threshold not only forfeits the 0% tax rate but also results in a five-year lockout from QFZP benefits.

"A Qualifying Free Zone Person that at any particular time during a tax period fails to meet any of the conditions shall cease to be a Qualifying Free Zone Person from the beginning of the relevant tax period and for the subsequent four tax periods."

Elena Ovchinnikova, Managing Director, Emirabiz

For example, in early 2025, a SaaS company based in Dubai Multi Commodities Centre (DMCC) discovered that 68% of its revenue came from mainland UAE clients, breaching the de minimis threshold. To resolve this, Dubai Business and Tax Advisors restructured the company’s mainland operations through a Domestic Permanent Establishment, reducing non-qualifying income to 3.4%. This move preserved the company’s QFZP status for both 2025 and 2026.

Here’s a breakdown of tax liabilities across different income scenarios:

| Taxable Income | Mainland Entity Tax Liability | Free Zone (QFZP) on Qualifying Income | Free Zone (Non-Qualifying/Breached) |

|---|---|---|---|

| $81,600 (AED 300,000) | $0 | $0 | $7,344 (9% from $1) |

| $136,000 (AED 500,000) | $3,060 (9% of $34,000) | $0 | $12,240 |

| $272,000 (AED 1,000,000) | $15,300 (9% of $170,000) | $0 | $24,480 |

| $544,000 (AED 2,000,000) | $39,780 (9% of $442,000) | $0 | $48,960 |

Note: QFZPs are taxed at 9% from the first dollar on non-qualifying income, without benefiting from the $102,000 (AED 375,000) 0% bracket [17].

It’s also important to note that Free Zone entities are restricted from direct transactions with mainland customers unless they work through a local distributor, agent, or mainland branch.

The Domestic Minimum Top-up Tax for Multinationals

For multinational enterprises (MNEs), the tax landscape becomes even more complex. Starting with financial years beginning on or after January 1, 2025, the Domestic Minimum Top-up Tax (DMTT) ensures that MNE groups with consolidated global revenues exceeding €750 million (around $869 million) pay at least a 15% effective tax rate in the UAE.

The DMTT isn’t a replacement for the UAE corporate tax system – it’s an additional layer. If an MNE group’s effective tax rate in the UAE falls below 15%, the government collects the difference as a top-up tax. For Free Zone entities operating under QFZP rules at a 0% tax rate, this means they’ll still face a 15% effective rate if part of a qualifying MNE group. This effectively counters any offshore tax benefits.

"Free Zone incentives may improve cash flow under domestic rules but may be partially neutralized under Pillar Two."

IMC Group

The calculation for the DMTT is done at the UAE jurisdictional level, aggregating all constituent entities in the UAE to determine the effective tax rate. While purely domestic UAE groups and smaller MNEs remain subject to the standard 9% corporate tax or 0% Free Zone rate, larger multinationals face a shifting tax planning environment.

To minimize the impact of the DMTT, businesses can focus on increasing Substance-Based Income Exclusions (SBIE) by boosting payroll and tangible asset investments within the UAE. These adjustments can influence GloBE calculations and reduce potential top-up taxes. Additionally, reviewing intercompany financing and dividend structures originally designed for a 0% or 9% tax regime may be necessary.

How to Reduce Tax Exposure in Dubai

Navigating tax regulations in Dubai can be challenging, but with a well-thought-out plan, businesses can minimize their tax liabilities while staying compliant. Here’s a closer look at strategies that can help.

Using Free Zones Effectively

The 0% corporate tax rate for Free Zone entities isn’t automatic – it comes with specific conditions. To qualify as a Qualifying Free Zone Person (QFZP), businesses must carefully manage their revenue mix. Non-qualifying income, such as mainland sales or B2C transactions, must stay below the lower of 5% of total revenue or $1.36 million (AED 5 million). Crossing this threshold disqualifies the entity from the 0% rate for the current and next four tax periods.

Take this example: In 2024, ABC Logistics FZ-LLC generated AED 4,200,000 in revenue, with AED 200,000 from non-qualifying activities – just 4.76% of its total revenue. Since this percentage stayed below the threshold, the company retained its QFZP status and the 0% tax rate.

To maintain compliance:

- Monitor revenue streams monthly.

- Engage an auditor early, as audited financial statements are mandatory.

- Keep employment contracts, payroll records, and lease agreements to prove economic substance.

For businesses with significant mainland operations, a Domestic Permanent Establishment (DPE) model can help. By separating mainland revenue (taxed at 9%) from the Free Zone’s qualifying income, companies can protect their 0% tax status. For instance, a DMCC-based SaaS firm in 2025 reduced its non-qualifying income from 68% to 3.4% by restructuring its mainland revenue through a DPE, preserving its 0% rate for both 2025 and 2026.

When Free Zone strategies aren’t enough, offshore structures may provide additional options to manage tax exposure.

Structuring with Offshore Entities

Pairing a Free Zone entity with an offshore structure can be a smart move, especially for businesses with global operations. One effective approach is the High Seas Sales model, where goods are purchased in one country and sold in another without entering the UAE. This qualifies as a distribution activity eligible for the 0% tax rate.

Here’s how it works in practice: A commodity trading company based in RAKEZ faced disqualification risks in 2025 because 54% of its revenue came from warehousing and retail distribution, exceeding the 51% threshold for traders. By using a High Seas Sales model and shifting some distribution income to a DPE (taxed at 9%), the company restored its qualifying revenue to 97%, saving $626,000 (AED 2.3 million) in taxes.

The UAE also offers a 0% withholding tax on outbound payments, including dividends, interest, royalties, and service fees, making profit repatriation more tax-efficient. Additionally, the Participation Exemption allows dividends and capital gains from share disposals to be exempt from corporate tax if ownership and holding period conditions are met.

Here’s a quick comparison of common business structures:

| Structure Type | Corporate Tax Rate & Treatment | Audit and Substance Requirements |

|---|---|---|

| Mainland Only | 9% on profits above $102,000 (AED 375,000) | Audit required if revenue exceeds $13.6M (AED 50M); physical office needed |

| QFZP Only | 0% on qualifying income | Mandatory audits; strict substance requirements (qualified employees, operations) |

| Hybrid (QFZP + DPE) | 0% on Free Zone income; 9% on mainland sales | Audits required for Free Zone component; robust substance needed |

In addition to structural strategies, businesses can explore tax relief mechanisms to further reduce their liabilities.

Using Tax Relief Mechanisms

Small Business Relief (SBR) is available for UAE resident businesses with annual revenue under $816,000 (AED 3 million), treating them as having zero taxable income until the end of 2026. However, QFZPs are excluded from this benefit.

For smaller consultancies, it might make sense to choose the standard 9% tax rate to access SBR. If revenue remains below AED 3 million, avoiding mandatory audits could save more than the benefits of the 0% rate.

Other relief options include:

- Intra-group Transfer Relief: Allows tax-neutral transfers of assets or liabilities between entities with at least 75% common ownership.

- Business Restructuring Relief: Provides tax benefits for mergers, spin-offs, or other restructurings done for valid commercial reasons.

- Foreign Tax Credit: Lets taxable persons claim credit for taxes paid in other jurisdictions, capped at the amount of UAE corporate tax on that income.

"The era of the ‘paper company’ or the ‘shelf entity’ used solely for tax shielding is effectively over."

– Dubai Business and Tax Advisors

Conclusion

Dubai may not be the tax-free paradise many imagine. While personal income is untaxed at 0%, the UAE has transitioned into a low-tax jurisdiction with real compliance requirements. Key taxes include a 9% corporate tax on profits exceeding $102,000 and a 5% VAT, both of which demand careful adherence to regulations.

This changing tax environment has specific implications for expats, particularly US citizens. Despite Dubai’s low-tax appeal, compliance with IRS, Social Security, and FATCA reporting remains mandatory. Without a tax treaty between the US and UAE, US citizens are still required to report to the IRS, regardless of where they reside. Self-employed individuals face an added 15.3% Social Security and Medicare tax, and the lack of a totalization agreement means there’s no relief from these contributions. UK expats should also be cautious of the five-year rule, as returning to the UK too soon could result in retrospective taxation on Dubai earnings.

These factors underscore the importance of proactive planning to navigate Dubai’s tax framework. It’s essential to understand how the 9% corporate tax applies to your company setup in Dubai, determine whether your Free Zone entity qualifies for the 0% rate, and ensure that mainland revenue doesn’t disrupt your tax status. Proper documentation of contract and decision-making locations is also crucial to avoid unintentionally pulling foreign income into the UAE tax system.

Dubai still provides tax benefits, but they are reserved for those who take the time to understand the rules and structure their finances wisely. The days of relying on superficial setups are over. Instead, a well-informed approach to compliance and wealth management is the key to thriving in this jurisdiction that prioritizes substance over shortcuts.

FAQs

Do I need to register with the FTA even if I owe $0 corporate tax?

Yes, registering with the Federal Tax Authority (FTA) is required for all taxable individuals and businesses operating in the UAE. This rule applies even if your corporate tax liability is $0 or if you’re not generating a profit. It’s a necessary step to stay aligned with UAE regulations.

How can a Free Zone company lose the 0% rate?

A Free Zone company risks losing its 0% tax rate if it doesn’t meet the requirements to qualify as a "qualifying free zone person." This could happen if the company fails to follow specific regulations or earns income that doesn’t meet the qualifying criteria. Such missteps may lead to penalties and a reassessment of tax liabilities. Staying compliant with the rules is essential to keep the 0% tax rate intact.

What triggers a UAE permanent establishment for a foreign business?

When a foreign business establishes a notable presence in the UAE – whether through a fixed place of business or dependent agents – it triggers what’s known as a UAE permanent establishment (PE). This connection forms a taxable link, meaning the business becomes responsible for paying UAE corporate tax on any profits earned within the country.