Flag Theory is about diversifying your life – citizenship, residency, banking, and businesses – across multiple countries to reduce risks like political instability, excessive taxation, or asset seizure. In 2026, as global financial transparency increases through systems like CRS and CARF, this strategy now focuses on compliance and creating genuine ties to jurisdictions. Here’s a quick overview of how to implement Flag Theory today:

- Second Citizenship: Obtain a second passport for mobility and safety. Options include Citizenship by Investment (CBI) starting at $200,000 (e.g., Caribbean nations) or ancestry-based routes for EU citizenship under $5,000.

- Tax Residency: Move to countries with territorial tax systems (e.g., Panama, Paraguay) to legally avoid taxes on foreign income.

- International Business: Set up tax-efficient entities in jurisdictions like the U.S. (for non-residents), BVI, or Singapore, ensuring compliance with local and international laws.

- Banking Diversification: Open accounts in stable financial hubs like Switzerland or Singapore, balancing liquidity and security.

- Asset Protection: Use offshore trusts (e.g., Cook Islands, Nevis) or foundations (e.g., Panama) to shield wealth from lawsuits or creditors.

This strategy requires careful planning, proper documentation, and compliance with global reporting standards like FATCA and CRS to avoid penalties. By spreading your life across jurisdictions, you gain flexibility, reduce risks, and protect your wealth in a transparent and lawful manner.

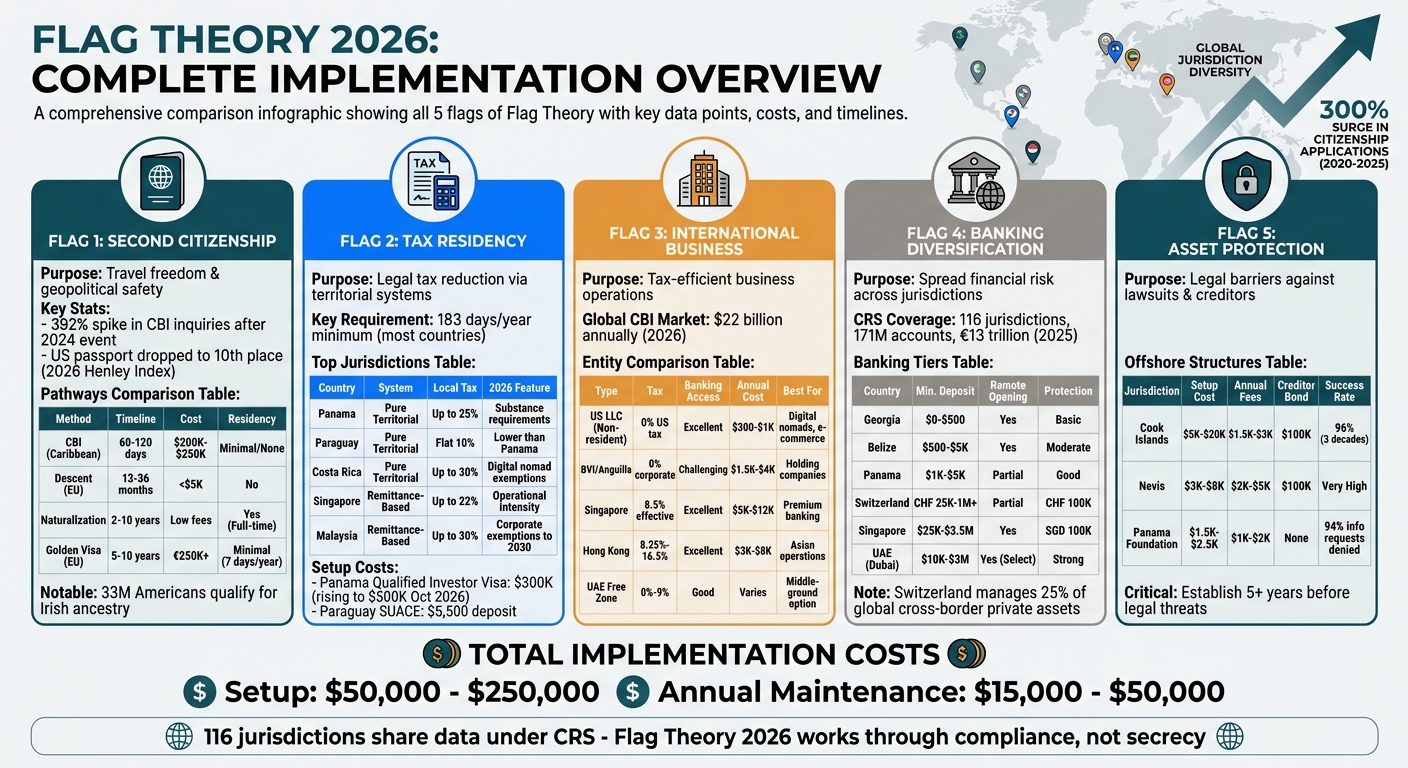

Flag 1: Getting Second Citizenship for Travel and Geopolitical Benefits

Second citizenship acts as a safeguard – a legal right to live in another country that ensures no single government has complete control over your mobility, wealth, or legal standing. As of 2026, it’s a practical tool for building a safety net that can withstand political upheavals, restrictive laws, and economic challenges.

Between 2020 and 2025, global citizenship applications surged by about 300%. A major political event in late 2024 alone triggered a 392% spike in Citizenship-by-Investment (CBI) inquiries. Meanwhile, the U.S. passport dropped to 10th place on the 2026 Henley Passport Index, its lowest ranking in over a decade. These trends highlight how second citizenship has shifted from being a luxury to a strategic necessity for many.

"A second passport has become a strategic asset – not a luxury. It is a hedge, a tool for optionality, and in many cases a gateway to healthcare systems and residency rights your home country cannot offer." – WhereNext Research Team

Why Platform-Access Citizenship Matters

Not all passports are created equal. Platform-access citizenship, like that of an EU member state, provides rights to live, work, and retire across entire blocs, offering far more than visa-free travel. For instance, a Maltese passport allows settlement in all 27 EU countries and access to healthcare systems in places like Portugal or France. This can save thousands annually on private insurance over a lifetime.

Caribbean passports, such as those from St. Kitts and Nevis (22nd on the 2025 Henley Passport Index), are valuable for travel but lack bloc-wide residency rights. Grenada, however, stands out with its E-2 treaty with the U.S., enabling citizens to apply for an investor visa. Choosing the right citizenship depends heavily on your long-term goals.

Recent changes like ETIAS (EU) and eTA (UK) in 2025-2026 now require digital pre-clearance for visa-free travel, complicating spontaneous trips for CBI holders. Additionally, Presidential Proclamation 10998 has restricted certain visa issuances for nationals of countries offering CBI without residency requirements, directly affecting Antigua & Barbuda and Dominica in early 2026. Many programs now mandate physical residency – Antigua requires 5 days, while others suggest 30 days over five years – to establish a "genuine link" to the country.

How to Obtain Second Citizenship

There are three main ways to secure second citizenship: citizenship by descent, citizenship by investment (CBI), and naturalization. Each route has its own costs, timelines, and residency obligations.

- Citizenship by descent is often the most affordable option. Around 33 million Americans qualify for Irish ancestry, 17 million for Italian, and 9 million for Polish. This path typically costs under $5,000 in fees and takes 12–36 months, with no residency requirement. It often results in highly sought-after EU passports.

- Citizenship by investment is the fastest route, taking just 60 to 120 days, with minimal or no residency requirements. The global CBI market is worth approximately $22 billion annually as of 2026. Caribbean programs start at $200,000 (e.g., Dominica), while EU options like Malta require €600,000 to €750,000, plus property or donations. Enhanced regulations now demand interviews, biometric checks, and thorough financial scrutiny. In 2023, Dominica revoked 260 citizenships for false information, signaling stricter enforcement.

- Naturalization takes longer and requires full-time residency but involves only filing fees. Portugal offers one of the quickest paths at 5 years, while Italy and Spain typically require 10 years. Many naturalization processes also require language proficiency, so early preparation is key.

The table below provides a quick comparison:

| Pathway | Timeline | Cost Estimate | Residency Required |

|---|---|---|---|

| CBI (Caribbean) | 60–120 Days | $200,000–$250,000 | Minimal/None |

| Descent (EU) | 12–36 Months | <$5,000 | No |

| Naturalization | 2–10 Years | Low (Fees only) | Yes (Full-time) |

| Golden Visa (EU) | 5–10 Years | €250,000+ | Minimal (7 days/year) |

For U.S. citizens, it’s important to note that holding a second passport does not exempt you from IRS filing or FATCA reporting. Tax compliance remains mandatory, regardless of where you hold citizenship.

Up next, we’ll dive into how establishing tax residency in territorial tax jurisdictions can further enhance your asset protection strategy.

sbb-itb-39d39a6

Flag 2: Setting Up Tax Residency in Territorial Tax Countries

Once you’ve secured a second passport, the next logical step is establishing tax residency. In countries with territorial tax systems, you’re only taxed on income earned within the country, while foreign income remains untouched.

This approach is perfectly legal in nations like Panama, Paraguay, and Costa Rica. However, tax authorities are paying closer attention to where work is actually performed. For example, earning income from U.S. clients while working in Panama might lead authorities to classify the income as locally sourced. The era of “mailbox” residencies is fading fast.

"The territorial tax rules in 2026 reward entrepreneurs who do their homework, build real substance, and plan their transitions carefully."

– Ipanema Partners

For U.S. citizens, it’s important to note that living in a territorial tax country doesn’t eliminate IRS obligations. You’ll still need to file an annual tax return and report your global income due to the U.S.’s citizenship-based taxation system.

Selecting Countries with Territorial Tax Systems

Territorial tax systems come in two main forms. Some countries, like Panama, Paraguay, and Costa Rica, operate under "pure" systems where all foreign income is untaxed. Others, like Thailand, use remittance-based systems, which tax only income brought into the country. However, even these systems are tightening. In 2024, Thailand began taxing all remitted income, regardless of when it was earned.

Panama remains a popular choice for many reasons. It uses the U.S. dollar, offers quick residency options (30 to 45 days under the Qualified Investor Visa), and exempts the first $11,000 of locally sourced income from tax. However, as of March 2026, Panama introduced new economic substance requirements. To keep foreign passive income tax-free, you’ll need to employ local staff and maintain a physical office.

Paraguay offers a flat 10% tax rate on locally sourced income, which is lower than Panama’s progressive tax rates of up to 25%. Costa Rica, meanwhile, has specific frameworks for remote workers, granting full tax exemptions on foreign income without requiring local incorporation. Malaysia has extended its tax exemption on foreign-sourced dividend income and capital gains for resident companies until December 31, 2030, as long as the income is taxed in its country of origin.

For those considering Europe, Italy and Greece offer lump-sum tax programs. Italy charges €200,000 per year on all foreign-sourced income, while Greece imposes a flat €100,000 annual charge for individuals who invest at least €500,000 in local assets. While these aren’t territorial systems, they do cap your tax liability regardless of how much you earn abroad.

| Country | System Type | Local Tax Rate | Key 2026 Feature |

|---|---|---|---|

| Panama | Pure Territorial | Up to 25% | Substance requirements for passive income |

| Paraguay | Pure Territorial | Flat 10% | Lower local tax than Panama |

| Costa Rica | Pure Territorial | Up to 30% | Digital nomad exemptions |

| Singapore | Remittance-Based | Up to 22% | Requires operational intensity |

| Malaysia | Remittance-Based | Up to 30% | Corporate exemptions until 2030 |

Once you’ve chosen a jurisdiction, the next step is to meet the residency requirements.

Meeting Residency Requirements

Most countries require that you spend at least 183 days per year to qualify as a tax resident. Some jurisdictions, like Cyprus, lower the threshold to just 60 days, but additional conditions apply, such as maintaining a permanent home and avoiding tax residency elsewhere.

By 2026, tax authorities are looking for proof of “substance” to confirm that you’ve genuinely relocated. This includes having a physical home, utility bills in your name, a local driver’s license, health insurance, and in some cases, employing local staff or maintaining office space. Keeping detailed travel records is essential to back up your residency claims.

Before establishing residency in a new country, you’ll need to formally sever tax ties with your previous high-tax jurisdiction. This involves steps like selling your primary home, deregistering as a tax resident, and obtaining a tax residency certificate from your new country. Without these steps, you risk dual residency, where both countries claim the right to tax your worldwide income.

"The only way to fully benefit from Panama’s territorial system is to formally and legally sever tax residency in your home jurisdiction before establishing Panamanian tax residency."

– Ipanema Partners

Each country has its own residency requirements. For instance, Panama’s Qualified Investor Visa requires a minimum $300,000 investment (increasing to $500,000 after October 15, 2026) and $10,000 in government fees. Paraguay’s SUACE program is more affordable, requiring just a $5,500 bank deposit. Costa Rica offers a three-year temporary residency phase before granting permanent status. Timelines, costs, and documentation vary, so it’s crucial to understand the specifics.

Lastly, ensure you maintain a “bank dossier” with apostilled proof of funds, past tax returns, and professional reference letters. By 2026, many territorial tax havens, including Panama, will have automated portals for CRS and FATCA compliance, enabling real-time financial data exchange with your home country’s tax authorities. Proper documentation is not just a formality – it’s the backbone of a defensible tax strategy.

These steps set the groundwork for tax-efficient residency, paving the way for future strategies involving international business entities.

Flag 3: Creating International Business Entities

Once you’ve established your tax residency, the next logical step is to fine-tune your business structure for global operations. Just like securing second citizenship and tax residency safeguards your personal wealth, setting up an international business entity helps protect and grow your commercial interests.

After finalizing your tax residency, the focus shifts to choosing the right business structure. International business entities can provide advantages like tax efficiency, asset protection, and access to global banking. However, these benefits depend heavily on picking the right jurisdiction for your specific business needs.

The key is to align your business entity with your operational model. For instance, holding companies often find jurisdictions like the British Virgin Islands or Cayman Islands appealing due to their 0% corporate tax policies. E-commerce businesses frequently opt for UK LTDs or US LLCs, which offer smooth integration with major payment processors. Meanwhile, trading and service companies often lean toward Singapore or Hong Kong for their strong reputations and global credibility.

That said, banking access is just as important as tax advantages. A jurisdiction with 0% tax won’t do much good if banks are reluctant to open accounts for your company. By 2026, banks increasingly demand operational substance – simply having a registered address won’t cut it.

"An offshore company is only as strong as the legal system behind it."

– Savory & Partners

For U.S.-based offshore companies, it’s worth noting that IRS Controlled Foreign Corporation rules can lead to offshore profits being taxed at personal rates, regardless of whether those profits are distributed.

Pass-Through Entities for Tax Neutrality

For non-U.S. residents, forming a single-member LLC in the U.S. offers a unique opportunity for tax neutrality. The IRS treats these LLCs as "disregarded entities", making them an attractive option for digital nomads, consultants, and e-commerce operators. This structure allows access to U.S. banking and payment platforms like Stripe and PayPal without triggering U.S. taxation. Popular states for formation, such as Wyoming and Delaware, typically have annual costs between $300 and $1,000. However, compliance is crucial – missing the required annual filings (Form 5472 and Form 1120) can lead to hefty penalties. For U.S. citizens and residents, the main perks of a U.S. LLC are asset protection and privacy, as their global income remains taxable.

Offshore Company Formation in Different Countries

Traditional offshore jurisdictions, such as the British Virgin Islands (BVI), Seychelles, and Anguilla, remain popular for specific purposes. They offer 0% corporate tax, strong asset protection laws, and private beneficial ownership registers. Among these, Anguilla stands out for its blend of privacy and legal stability. Companies in Anguilla enjoy 0% personal and corporate income tax, with formation costs around $2,500 and annual maintenance fees ranging from $1,500 to $4,000.

However, banking can be a challenge in these jurisdictions. Many banks are hesitant to work with companies registered in places like the BVI or Seychelles, often pushing businesses toward electronic money institutions like Wise or Revolut.

For businesses that require access to top-tier banking services, Singapore and Hong Kong are standout choices. In Singapore, while the corporate tax rate is officially 17%, exemptions can lower the effective rate to about 8.5% on the first SGD 200,000 of income. Hong Kong uses a tiered system, taxing profits at 8.25% on the first HKD 2 million and 16.5% on anything above that. Both jurisdictions offer excellent banking options and strong international reputations. Maintenance costs for Singapore companies typically range from $5,000 to $12,000 annually, while Hong Kong companies incur $3,000 to $8,000 in annual costs.

The UAE has also become an appealing middle-ground option. Free Zone companies in the UAE can enjoy 0% corporate tax on qualifying income, though profits exceeding AED 375,000 (about $100,000) are subject to a federal tax of 9%. Formation costs vary depending on the specific Free Zone.

US LLCs vs. Offshore Companies: A Comparison

| Feature | US Single-Member LLC (Non-Resident) | Traditional Offshore Company (e.g., BVI/Anguilla) |

|---|---|---|

| Tax Treatment | Pass-through; 0% US tax when no US trade exists | 0% corporate tax at the entity level |

| Banking Access | Excellent – access to US banks, Stripe, PayPal, Wise | More challenging; may require electronic money institutions |

| Credibility | High; generally viewed as a standard onshore entity | Moderate; may trigger enhanced due diligence |

| Annual Cost | Approximately $300–$1,000 | Typically around $1,500–$4,000 or more |

| Privacy | Lower | Superior |

| Best For | Digital nomads, consultants, e-commerce operators | Holding companies and asset protection |

Before setting up any entity, make sure the jurisdiction you choose is compatible with the banks or payment processors your business relies on. A jurisdiction that seems cost-effective at first may end up being costly if it limits access to critical financial services.

Once your business entity is properly structured, the next step is to diversify your banking and financial assets across international borders.

Flag 4: Spreading Banking and Financial Assets Across Countries

Once you’ve set up your international business entity, the next crucial step is to avoid keeping all your banking and financial assets in one country. Concentrating your funds in a single jurisdiction leaves you vulnerable to risks like political upheaval, currency fluctuations, and capital controls. This isn’t about hiding assets but about managing risks effectively. As of late 2025, 116 jurisdictions are part of the Common Reporting Standard (CRS), sharing financial data on 171 million accounts worth about €13 trillion. By spreading your assets across multiple countries, you protect yourself from systemic risks, ensuring no single government or crisis can restrict access to your wealth. This diversification also opens the door to premium banking options, which we’ll cover shortly.

"Offshore does not mean invisible anymore. It means your assets are not trapped inside one jurisdiction."

– Cunicula

A smart way to approach this is through a two-tier strategy. Use jurisdictions like Georgia or Belize for day-to-day operational funds, as they offer easy accessibility, while placing long-term capital in stable financial hubs such as Switzerland or Singapore. This approach balances liquidity for daily needs with security for your core assets.

Opening Accounts in Top-Tier Banking Countries

When it comes to offshore banking, Singapore and Switzerland continue to set the benchmark in 2026. Switzerland alone manages around 25% of the world’s cross-border private assets, while Singapore’s banks – DBS, OCBC, and UOB – rank among the safest globally. Both countries are CRS-compliant, meaning account data is automatically reported to your home country, but they compensate for this with unparalleled financial stability and reliability.

In Singapore, priority banking services require deposits ranging from $25,000 to $250,000 for standard accounts, and between $1.5 million and $3.5 million for private banking. Switzerland, on the other hand, starts with CHF 25,000 for basic accounts and CHF 1 million for premium services. Both jurisdictions also offer strong deposit insurance (SGD 100,000 in Singapore and CHF 100,000 in Switzerland) and maintain Tier 1 capital ratios of 12–15%.

Here’s a quick comparison of deposit requirements and banking options across popular jurisdictions:

| Country | Typical Min. Deposit | Remote Opening | Best For |

|---|---|---|---|

| Georgia | $0 – $500 | Yes (In-person preferred) | Easy setup, low cost |

| Belize | $500 – $5,000 | Yes | Transactional banking |

| Panama | $1,000 – $5,000 | Partial | SMEs, entrepreneurs |

| Switzerland | CHF 25,000 – CHF 1,000,000+ | Partial (Video KYC) | Wealth preservation |

| Singapore | $25,000 – $3,500,000 | Yes (via Fintech) | Stability, access to Asian markets |

| UAE (Dubai) | $10,000 – $3,000,000 | Yes (Select banks) | Middle-ground option |

Be prepared to provide detailed source-of-funds documentation, as incomplete or unclear records are a common reason for account application rejections. This means compiling evidence like tax returns, business contracts, or sales agreements into a clear, chronological narrative to explain where your funds originated.

"The wrong jurisdiction doesn’t fail you obviously. It fails you in transfer delays, in FX margins you didn’t track, and in minimum balances sitting idle."

– Bertrand Théaud, Founder of Statrys

While traditional banks offer stability, modern financial tools can complement your strategy for more agile fund management.

Using Global Payment Platforms

Fintech platforms like Wise, Revolut, and Statrys have revolutionized the way businesses manage multi-currency operations. These platforms offer benefits like lower fees, faster transfers, and remote account setups – making them indispensable for maintaining liquidity in 2026.

For example, Wise allows you to hold and convert over 50 currencies at real exchange rates with minimal fees, often beating traditional banks on foreign exchange margins. Similarly, Statrys focuses on business accounts tailored for SMEs and digital nomads, with seamless integrations for payment processors like Stripe and PayPal.

However, fintech platforms lack traditional deposit protection and regulatory oversight. This makes them ideal for operational tasks like supplier payments, client transactions, and currency conversions, but they aren’t suitable for long-term wealth storage.

For U.S. citizens, compliance with regulations is critical. If your total foreign accounts exceed $10,000 at any point in the year, you must file an FBAR (FinCEN Form 114). Additionally, ensure any offshore bank you choose is FATCA-compliant, as many institutions avoid U.S. clients due to the reporting requirements.

The best strategy is to align the right tool with the right purpose: use established banks for asset preservation, accessible jurisdictions for daily transactions, and fintech platforms for efficient international transfers. This layered approach ensures you maintain control over your funds, regardless of challenges in any one location.

Flag 5: Protecting Assets with Offshore Structures

Once you’ve diversified your banking and financial assets across multiple countries, the next step is setting up legal structures to shield your wealth from threats like lawsuits and creditors. These structures act as legal barriers, making it far more difficult for others to seize your assets. By 2026, with over 120 jurisdictions participating in the Common Reporting Standard (CRS), these setups operate transparently, relying on legal protections rather than secrecy. Offshore structures add a critical layer of protection for your wealth, complementing your diversified financial base.

"Asset protection is planning, not magic."

– Cunicula

Offshore structures generally fall into two main categories: trusts and foundations. Trusts place assets under the management of a trustee for the benefit of specified beneficiaries, while foundations act as independent legal entities that own assets. For Americans and other common-law users, trusts in places like the Cook Islands or Nevis are popular choices. Meanwhile, individuals from civil-law regions such as Europe, the Middle East, or Latin America often lean toward foundations in jurisdictions like Panama or Liechtenstein.

Using Offshore Trusts and Foundations

Certain jurisdictions, such as the Cook Islands, Nevis, and Panama, are well-known for providing strong asset protection. These locations impose strict limitations on creditor actions and make it costly and difficult to challenge asset transfers. For example, the Cook Islands International Trusts Act has successfully protected trusts in 96% of cases over three decades. Similarly, Nevis offers robust protections at a lower cost, requiring creditors to litigate locally, where the legal standards are much tougher. In Nevis, creditors must prove fraudulent intent "beyond a reasonable doubt" – a criminal standard – and post a $100,000 litigation bond just to file a case.

Time is also a factor. In these jurisdictions, creditors typically have only one to two years to challenge a trust after assets are transferred. Compare this to the U.S., where the Bankruptcy Code allows a 10-year look-back period for transfers to self-settled trusts. This makes it crucial to establish these structures long before any legal threats arise.

For those looking for a simpler and more affordable option, Panama foundations offer strong privacy protections at a lower cost. Panama has reportedly denied 94% of foreign information requests, and setting up a foundation typically costs between $1,500 and $2,500 – much less than the $5,000 to $20,000 needed for a Cook Islands trust. Foundations are particularly effective for holding international business entities or real estate and are more widely recognized in civil-law countries.

One advanced approach is the "Bridge Trust" model. This strategy involves a Nevis or Cook Islands trust owning a Nevis LLC, which then holds the assets. This creates dual layers of protection: the LLC shields personal assets from business liabilities, while the trust protects the LLC from personal creditors.

Here’s how the most popular jurisdictions compare:

| Jurisdiction | Setup Cost | Annual Fees | Burden of Proof | Creditor Bond | Best For |

|---|---|---|---|---|---|

| Cook Islands | $5,000–$20,000 | $1,500–$3,000 | Beyond reasonable doubt | $100,000 | Maximum protection, battle-tested |

| Nevis | $3,000–$8,000 | $2,000–$5,000 | Beyond reasonable doubt | $100,000 | Strong LLC/trust hybrid |

| Panama Foundation | $1,500–$2,500 | $1,000–$2,000 | Clear and convincing | None | Cost-effective, privacy-focused |

Maintaining Compliance and Proper Structure

Setting up an offshore trust or foundation is just the beginning. To ensure its effectiveness, proper governance and compliance are critical. Courts are quick to invalidate "sham" structures where the settlor retains too much control. A well-known example is the FTC v. Affordable Media case (also called "The Anderson Case"), where settlors who appointed themselves as Trust Protectors were jailed for contempt. Their retained powers – such as the ability to fire the trustee – were seen as evidence of undue control over the trust.

"A trust that provides meaningful protection requires meaningful independence: a professional trustee exercising genuine discretion."

– Ipanema Partners

To avoid these pitfalls, it’s essential to appoint a truly independent trustee – ideally a professional firm with no personal ties to the settlor. This trustee must have real authority over distributions and investments. Many also appoint an independent Trust Protector, who can replace trustees or move the trust to a different jurisdiction if needed.

Regular governance practices, like holding board meetings and documenting decisions, help demonstrate that the structure serves a legitimate purpose beyond tax avoidance. Tax authorities and courts increasingly scrutinize these details to uncover who actually controls the assets.

For U.S. citizens, compliance is mandatory. Offshore trusts must file Form 3520 (Transactions with Foreign Trusts) and Form 3520-A (Annual Information Return of Foreign Trusts) annually. Failure to comply can result in penalties starting at $10,000 or 5% of the trust’s assets. Additionally, offshore structures do not provide tax secrecy. Under CRS and FATCA, financial information is automatically shared with your home country.

Timing is everything. These structures should be established well before any potential legal threats arise – ideally at least five years in advance. Transfers made after receiving a demand letter are often classified as fraudulent and can be undone. For instance, in United States v. Huckaby, a Nevada Spendthrift Trust failed to protect California real estate from an IRS lien. The court ruled that California law applied to the property, invalidating the trust’s protections.

"If you wait until you’re already being sued to set up an asset protection structure, you are playing a losing game regardless of jurisdiction."

– Ipanema Partners

When designed with genuine independence, proper governance, and proactive planning, offshore trusts and foundations remain some of the strongest tools for safeguarding wealth. The prominence of trust-based structures in the Cayman Islands, which account for over 55% of the nation’s GDP, highlights their central role in global wealth management.

How Global Wealth Protection Helps Implement Flag Theory

Implementing Flag Theory in 2026 requires careful planning, especially with the increased transparency brought by CRS 2.0 and the Crypto-Asset Reporting Framework. Global Wealth Protection (GWP) steps in to simplify this process by offering incorporation and compliance services for LLCs in over 50 jurisdictions, along with consulting to help you design a structure tailored to your needs. Over the last seven years, GWP has supported over 1,000 businesses in developing internationalization strategies.

One of their standout offerings is access to a vast network of banking and payment providers, including Stripe, PayPal, and Wise, ensuring your financial operations run smoothly despite regulatory challenges. For non-US residents, forming a US single-member LLC in states like Wyoming or Delaware is particularly advantageous. These LLCs are considered disregarded entities, which means they are exempt from US corporate tax and avoid Controlled Foreign Corporation (CFC) rules in many territorial tax jurisdictions. GWP takes care of the administrative work, including filing IRS Form 5472 for $325, helping you avoid penalties and focus on growing your business.

"The updated international diversification strategy that practitioners now use works through transparency and compliance rather than opacity and invisibility."

– Ipanema Partners

In addition to US LLCs, GWP assists with setting up offshore companies, trusts, and foundations in jurisdictions that align with your goals. Whether you need asset protection in Anguilla or licensing for industries like fintech or crypto, their services are designed to meet your specific requirements. This aligns with the broader concept of creating a "Jurisdiction Stack", which unbundles your life into distinct areas like physical residence, business domicile, asset custody, and digital identity.

Action Plan for Implementing Flag Theory

Once your global structures are in place, the next step is to implement Flag Theory strategically. The key is sequencing – each step builds on the last. Here’s a breakdown of the process:

- Establish tax residency: Start by securing tax residency in a territorial tax country like Panama or Paraguay. Obtain a Tax Residency Certificate to document your "center of life." This step simplifies compliance since CRS reporting flows to your country of residency.

- Register your business entity: For location-independent entrepreneurs, GWP’s US LLC service is a strong option. Ensure the LLC doesn’t have a physical office or employees in the US, so its income remains classified as foreign-source.

- Open banking relationships: Diversify by setting up accounts in two to three jurisdictions. This redundancy protects you if one bank closes accounts due to your passport nationality. Platforms like Wise Business can manage cash flow and multi-currency needs while you establish private banking relationships in places like Singapore or Switzerland, which can take 3–12 months.

- Pursue a second passport: Explore citizenship-by-investment programs (starting at $200,000 for Caribbean options in early 2026) or ancestry-based routes.

- Diversify asset custody: Use offshore trusts or foundations to secure your assets. Ensure these structures have legal substance and meet regulatory standards to avoid scrutiny.

Comprehensive five-flag strategies for high-net-worth individuals typically cost between $50,000 and $250,000 for setup, with annual maintenance ranging from $15,000 to $50,000 for compliance and management.

"Flag Theory encourages the idea that you should ‘go where you’re treated best.’"

– Nomad Capitalist

Benefits of GWP Insiders Membership

The GWP Insiders program offers a wealth of resources to help you navigate internationalization. Membership includes access to a global network of experts – lawyers, accountants, and bankers – as well as tailored advice and exclusive content on tax reduction, jurisdiction selection, and asset protection. This support is invaluable in an era where AI-driven tax enforcement tools analyze geolocation data, transaction patterns, and CRS reports to detect inconsistencies in residency claims.

Properly executed Flag Theory strategies can lead to significant tax savings while staying fully compliant. For instance, a remote founder earning $300,000 annually could save around $141,000 by relocating from a high-tax country like Germany to the UAE. The membership ensures you avoid pitfalls like incorrect residency claims, which can result in penalties, withholding taxes, or account freezes. These benefits highlight the importance of diversifying your jurisdictions and managing your global strategy effectively.

Conclusion: Using Flag Theory for Maximum Protection in 2026

Flag Theory in 2026 revolves around strategically spreading your life across multiple jurisdictions to reduce taxes, safeguard your assets, and maintain personal freedom. The landscape has shifted – what once relied on secrecy now demands transparency. With the Common Reporting Standard (CRS) and cryptocurrency reporting becoming the norm, the old "invisible offshore" approach no longer works.

The modern take on Flag Theory builds a resilient structure by focusing on key strategies. At its core is establishing tax residency in a country with territorial taxation, such as Panama, Paraguay, or the UAE. This approach allows you to legally eliminate taxes on foreign-sourced income while staying fully compliant with global reporting requirements. From there, diversifying your banking across two or three jurisdictions, creating tax-neutral entities like US LLCs, and securing a second passport can collectively strengthen your protection and flexibility.

"The ultimate goal of Flag Theory isn’t tax minimization alone, but creating a resilient, global framework that protects what you’ve built."

- Project Black Ledger

In today’s world, substance is critical. Advanced tax enforcement tools – like AI-driven systems – now cross-check geolocation data, transaction records, and CRS reports to validate claims. Outdated tactics like paper companies or mailbox residencies won’t hold up under scrutiny. Genuine economic ties are essential, including physical presence, local banking relationships, and evidence that establishes your "center of life."

The beauty of Flag Theory lies in its flexibility. You don’t need to implement all five flags simultaneously. Start with the one offering the most immediate advantage – tax residency is often the first step – and expand from there. With expert advice from organizations like Global Wealth Protection, you can navigate the complexities, stay compliant, and position yourself where you’re treated best. In this context, relocating your life isn’t just a lifestyle choice – it becomes a strategic tool to secure your financial future.

FAQs

What’s the first “flag” I should plant in 2026?

In 2026, one of the first steps to consider is securing a second citizenship in a country known for low taxes and strong privacy laws. This serves as a cornerstone for global diversification, opening doors to more residency options, offshore banking opportunities, and increased mobility. By obtaining a second citizenship, you gain greater flexibility and an added layer of security for both your legal and financial affairs.

How do I prove “substance” for tax residency without getting dual-taxed?

To demonstrate substance for tax residency and avoid the complications of dual taxation, it’s crucial to establish real connections to the jurisdiction. This can involve:

- Living there for a significant part of the year: A physical presence is often a key indicator of residency.

- Participating in local economic activities: This might include running a business, holding a job, or other forms of active involvement in the economy.

- Maintaining proper documentation: Examples include local bank accounts, lease agreements, or utility bills that confirm your active ties to the area.

Taking these steps can help confirm legitimate residency and minimize potential tax issues.

Will CRS/FATCA reporting expose my offshore bank accounts or trusts?

CRS and FATCA reporting have made offshore accounts more transparent. U.S. account holders must adhere to FATCA, which mandates reporting to the IRS. On the other hand, accounts in jurisdictions outside the CRS framework might still offer certain privacy protections. It’s crucial to carefully assess the legal and financial consequences of these regulations when handling offshore assets.