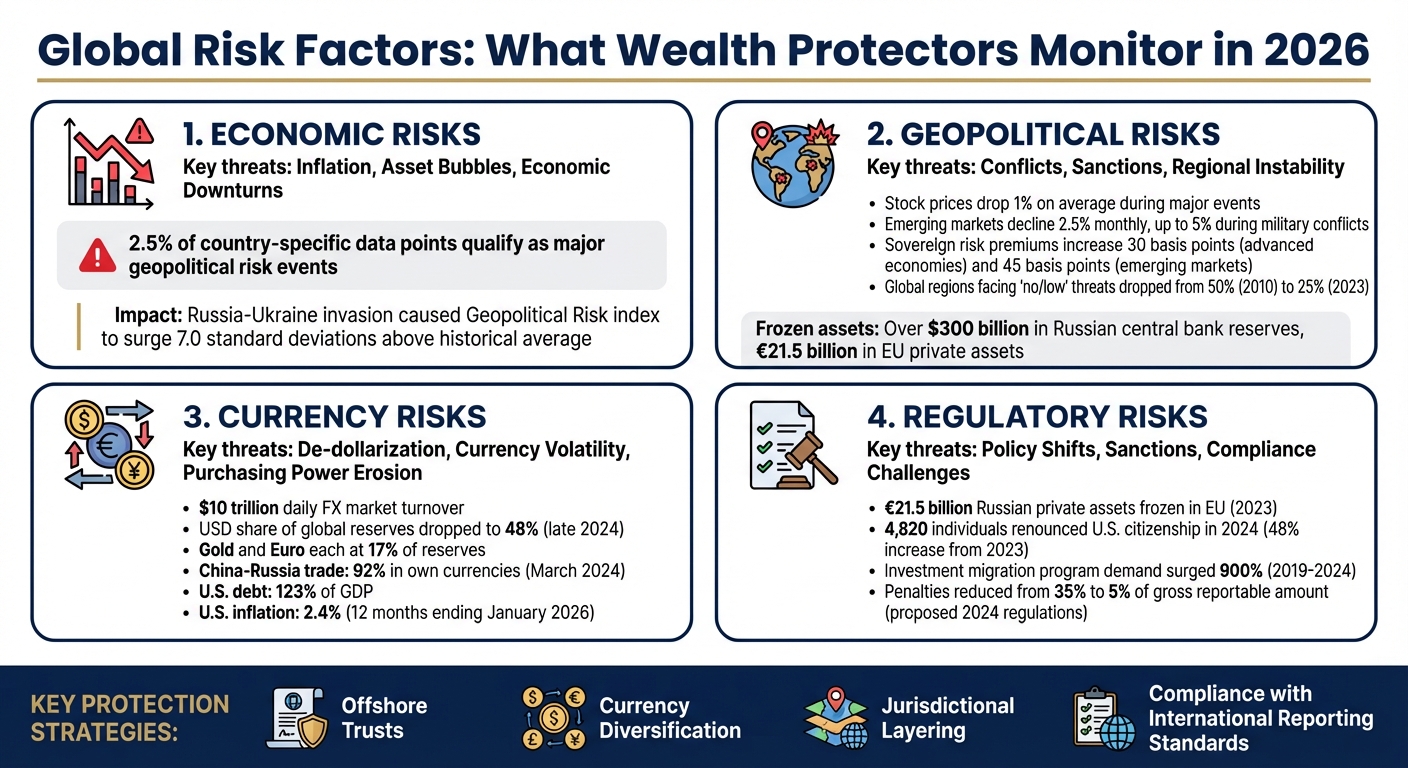

In 2026, managing wealth is more challenging than ever due to rising global risks. Economic instability, geopolitical tensions, currency fluctuations, and regulatory changes are reshaping how wealth is protected. High-net-worth individuals and investors must now actively monitor and adapt to these risks to safeguard their assets. Here’s a quick breakdown of the key risks:

- Economic Risks: Inflation, asset bubbles, and economic downturns threaten portfolios, especially those heavily leveraged or concentrated.

- Geopolitical Risks: Conflicts, sanctions, and regional instability disrupt markets, supply chains, and investor confidence.

- Currency Risks: De-dollarization and currency volatility erode purchasing power and investment returns.

- Regulatory Risks: Policy shifts, sanctions, and compliance challenges create hurdles for global asset protection.

To navigate this landscape, strategies like offshore trusts and private interest foundations, currency diversification, and jurisdictional layering are essential. These tools help protect assets from market shocks, geopolitical turmoil, and regulatory scrutiny while maintaining compliance with international reporting standards.

Key Takeaway: Wealth protection in 2026 requires proactive measures, diversified asset allocation, and robust legal structures to withstand global uncertainties.

Four Major Global Risk Factors Threatening Wealth in 2026

Economic Risks: Instability, Inflation, and Asset Bubbles

Economic instability directly threatens the ability to preserve wealth. When inflation rises sharply, central banks respond by tightening monetary policies, which leads to higher borrowing costs and restricted credit. This chain reaction makes it harder for businesses to secure funding, slows economic growth, and causes asset values to drop. For those with highly leveraged or concentrated portfolios, this can result in severe losses.

The narrative around market risks has shifted over time. In 2023, inflation dominated headlines, but by late 2024, the focus turned to concerns over U.S. fiscal debt and policy uncertainties. Sovereign bond markets in countries with high government debt have become increasingly volatile as investors demand higher risk premiums. Meanwhile, emerging markets are grappling with their highest real financing costs in a decade, complicating traditional diversification strategies.

Inflation and Economic Downturns

Persistent inflation creates ripple effects in financial markets, flattening yield curves and amplifying volatility. High-net-worth portfolios, in particular, are prone to rapid asset sell-offs during such periods of market turbulence.

"Financial stability risks have increased rapidly as the resilience of the global financial system has been tested by higher inflation and fragmentation risks." – IMF Global Financial Stability Report

Geopolitical events add another layer of complexity. Historical records reveal that roughly 2.5% of country-specific data points qualify as major geopolitical risk events. A striking example is Russia’s invasion of Ukraine in February 2022, which caused the Geopolitical Risk index to surge 7.0 standard deviations above its historical average. This event disrupted energy and commodity markets, intensifying inflationary pressures.

Keeping tabs on key economic metrics is crucial. Indicators like the Consumer Price Index, long-term interest rate term premiums, and public Debt-to-GDP ratios provide early warnings of emerging challenges. For instance, unexpected increases in term premiums or rising debt-to-GDP ratios highlight potential trouble. In such scenarios, diversifying into economies with lower debt levels and transparent credit systems, while maintaining liquidity reserves, can offer a safety net against sudden market downturns. These metrics not only signal potential economic stress but also help guide proactive strategies for protecting wealth.

In addition to inflation, asset valuation bubbles present another challenge for managing portfolios effectively.

Asset Bubbles in Emerging Markets

Asset bubbles form when valuations no longer align with underlying fundamentals. A prime example occurred in 2025 when U.S. equity markets were heavily influenced by enthusiasm around artificial intelligence, leading to concentration risks in technology sectors. At the same time, weakening fundamentals in commercial real estate created significant loss exposure for financial intermediaries. Similar trends have been observed in emerging markets, where rapid capital inflows inflate property and equity prices beyond sustainable levels.

"The current combination of relatively high asset valuation pressures and heightened geopolitical and policy uncertainty increases the risk of a sudden pullback from risk-taking." – Federal Reserve Financial Stability Report

Geographical diversification is a vital strategy to mitigate these risks. Spreading investments across various countries and regions can protect portfolios from localized economic crises and market crashes. Offshore trusts, for example, provide structural safeguards by holding assets in jurisdictions with stable legal systems, reducing reliance on any single economy or government. Additionally, commodity-exporting countries – where over 60% of merchandise exports come from commodities – tend to experience sharper stock market declines during geopolitical shocks. Balancing exposure to such markets with non–commodity-linked assets and conducting regular stress tests through scenario analysis can strengthen portfolio resilience. These measures help identify vulnerabilities early, allowing for adjustments before they become urgent. Monitoring asset bubbles is essential for strategic asset allocation, ensuring stability through diversified investments and structural protections like offshore trusts.

sbb-itb-39d39a6

Geopolitical Risks: Tensions and Armed Conflicts

Geopolitical tensions can wreak havoc on global markets and supply chains, compounding economic challenges and creating uncertainty for investors.

When instability strikes, the financial impact is immediate. Major geopolitical events typically cause stock prices to drop by 1% on average, with emerging markets experiencing sharper declines – up to 2.5% monthly. During military conflicts, emerging markets can see losses as steep as 5% per month.

The consequences extend beyond market volatility. Sovereign risk premiums – essentially the cost of insuring against government defaults – increase significantly after such events, rising by 30 basis points for advanced economies and 45 basis points for emerging markets. This drives up borrowing costs for governments, which often trickles down to businesses and consumers, stifling economic activity. Countries that rely heavily on trade with a nation involved in military conflict also see stock valuations decline, typically by around 2.5%.

These disruptions ripple through global supply chains, energy markets, and commodity prices, intensifying inflationary pressures.

"The war has also accelerated economic trends like deglobalisation, as companies reshape their global value chains and investors rethink their portfolios in order to minimise their dependence on markets in volatile countries." – Jeron Yeoh, WRISE

Over the last decade, the percentage of global regions facing "no" or "low" threats from international tensions has plummeted – from 50% in 2010 to just 25% by 2023. This shift means most of the world now grapples with moderate to severe geopolitical risks. Governments, in response, are redirecting budgets toward defense and industrial policies, often at the expense of social programs.

State Conflicts and Regional Instability

Certain regions present heightened risks for investors, particularly during conflicts. Russia’s annexation of Crimea is a prime example of how geopolitical events can swiftly dry up liquidity in affected areas. International sanctions were imposed almost immediately, freezing assets and halting financial transactions. Investors were left unable to access or move their capital. A similar pattern emerged with recent sanctions, where U.S. and allied governments froze over $300 billion in Russian central bank reserves and at least $58 billion in private wealth. Within the European Union, more than €21.5 billion in Russian private assets were frozen by 2023.

Commodity exporters face unique vulnerabilities. Conflicts often reduce global demand, driving down oil and commodity prices and triggering sharp equity declines in these sectors.

To measure and monitor geopolitical risks, tools like the Geopolitical Risk Index (GPR) and economic policy uncertainty indices are invaluable. The GPR tracks adverse news events related to tensions, while European indices quantify uncertainty by analyzing terms like "uncertainty" and "economy" in major newspapers.

"Geopolitical tension does not always overlap with market stress, but it can affect economies either by damaging confidence, and demand, or by disrupting supply chains." – John Bilton, Head of Global Multi-Asset Strategy, J.P. Morgan Asset Management

To navigate these risks, diversifying into neutral jurisdictions with balanced international relations is critical. Countries like Singapore, Ireland, and Switzerland are often seen as safe havens due to their stable environments and diplomatic strategies. Sector selection also matters – industries like healthcare and technology tend to weather geopolitical volatility better than more exposed sectors like energy or finance. Real assets, such as infrastructure, timber, and transportation, can also provide a hedge against inflation caused by supply chain disruptions.

Using International Trusts to Reduce Geopolitical Risks

International trusts in stable jurisdictions offer a powerful way to shield assets from geopolitical turmoil. Holding assets directly in volatile regions exposes them to risks like government sanctions, regulatory changes, or asset freezes. By transferring ownership to a neutral jurisdiction, international trusts add a protective layer that’s harder for sovereign actions to penetrate.

Key jurisdictions for establishing these trusts include the UAE, Singapore, Switzerland, and the Cayman Islands. Each offers distinct advantages: the UAE is valued for its neutrality and accessibility, Singapore boasts political stability and a tech-forward approach, Switzerland is known for its neutrality and robust banking system, and the Cayman Islands is favored for its tax efficiency and strong trust laws. Combining these jurisdictions – such as pairing a Singapore entity with a Cayman trust – can create a multi-layered defense against geopolitical risks.

Geoeconomic confrontation has emerged as the top global risk as of January 2026, surpassing even pressing issues like climate change and cyber threats. This underscores the urgency of jurisdictional diversification. International banks have increasingly "de-risked" by closing accounts linked to high-risk regions like Russia, Venezuela, and Hong Kong, leaving individuals without proper trust structures at risk of being locked out of the global financial system.

To implement these strategies effectively, careful planning is essential. A comprehensive exposure audit can help identify hidden risks and correlations tied to volatile regions. Currency hedging tools like forwards and options can mitigate unwanted foreign exchange exposure, often triggered by safe-haven flows or emerging market currency devaluations.

Tiered liquidity management also plays a vital role. A three-tier system might include immediate cash equivalents in neutral jurisdictions for emergencies, medium-term fixed income for opportunistic investments, and long-term illiquid assets for growth. This ensures that capital remains accessible even if one jurisdiction becomes inaccessible.

Historical evidence supports maintaining a diversified market presence during geopolitical tensions. A 60/40 stock/bond portfolio has historically outperformed cash 75% of the time one year after a major market shock – and 100% of the time after three years. The key lies in structuring assets across stable jurisdictions and sectors to withstand volatility.

Currency Risks: Fluctuations and De-Dollarization

Keeping an eye on currency movements is just as crucial as monitoring economic and geopolitical risks when it comes to safeguarding wealth. Currency volatility often flies under the radar but can significantly erode purchasing power and distort investment returns. The foreign exchange market, with its staggering $10 trillion daily turnover, is the largest and arguably the most unpredictable financial market in the world. This unpredictability doesn’t just shake global financial stability; it also directly impacts individual investment portfolios.

The U.S. dollar’s dominance is slipping. Central banks are diversifying their reserves, moving away from the dollar. By late 2024, the dollar’s share of global allocated reserves had dropped to 48%, while gold and the euro each accounted for around 17%. Meanwhile, countries like China and Russia are conducting most of their trade – about 92% as of March 2024 – in their own currencies, bypassing the dollar entirely. Additionally, groups like BRICS are working on payment systems that eliminate the need for the dollar.

For U.S. investors, this shift presents a double-edged sword. Domestic inflation, reported at 2.4% for the 12 months ending January 2026, steadily eats away at purchasing power. At the same time, a weakening dollar magnifies losses on international investments when profits are converted back into dollars. Compounding these challenges, the U.S. national debt now exceeds 123% of GDP, with interest payments outpacing defense spending. Moody’s downgrade of the U.S. credit rating to Aa1 further underscores these fiscal pressures.

"The decline of the U.S. dollar isn’t a speculative risk. It’s a documented trend rooted in fiscal realities and political decisions." – Jamie Vrijhof-Droese, Managing Partner, WHVP

The assumption that the dollar strengthens during times of market stress is no longer reliable. For instance, in 2025, policy uncertainty and tariff announcements led to simultaneous selloffs in U.S. stocks, bonds, and the dollar – a rare occurrence that weakened the dollar’s reputation as a safe haven. Historically, during crises like March 2020, foreign purchases of U.S. dollars surged by about 24 percentage points. However, this pattern can no longer be taken for granted.

How Currency Volatility Affects Investments

Exchange rate swings can directly diminish the dollar value of international investments, regardless of how the actual assets perform. This "valuation effect" means that even if foreign stocks or bonds perform well in their local currency, their value in dollars could decline.

The impact can be stark. For example, holding €100,000 in European bonds would equate to $110,000 if the exchange rate is $1.10 per euro. But if the euro weakens to $1.00, the same position drops to $100,000 – a $10,000 loss. On top of this, banks often apply hidden spreads, further reducing the exchange rate. If the official rate is 0.90 EUR per USD, a bank might offer just 0.87 EUR, effectively charging a 3.3% fee.

Currency volatility also drives up the cost of hedging. During stressful periods, the "cross-currency basis" – the cost of swapping one currency for another – widens, making it more expensive to protect against exchange rate risks. Bid-ask spreads also increase, and market liquidity can dry up. While non-bank institutions typically provide liquidity in currency markets, they can also add to market instability in times of crisis.

For fixed-income investments, unhedged foreign bond positions are particularly vulnerable. Factors like interest rate differentials, dollar fluctuations, and commodity price changes can account for up to 80% of exchange rate variations, often overshadowing the bond’s actual returns.

Hedging with Offshore Trusts and Multiple Currencies

Given these risks, diversifying currency exposure becomes essential. One effective strategy is to use offshore trusts in stable jurisdictions. These structures offer a level of protection that domestic multi-currency accounts cannot match.

Offshore trusts in neutral locations like Switzerland, Singapore, and the Cayman Islands provide both stable currencies and strong legal protections. For example, the Swiss franc has long been a reliable safe haven. When U.S. inflation hit 9.1% in 2022, Switzerland’s inflation was just 3.5%. Analysts predict the USD/CHF exchange rate could reach 0.76 by June 2026, reflecting ongoing dollar weakness.

Aligning your currency holdings with your spending habits can also help. If 40% of your expenses are in Europe, holding 40% of your assets in euros creates a "natural hedge", ensuring that currency fluctuations impact both assets and liabilities proportionately.

Central banks are already diversifying into nontraditional currencies like the Australian dollar, Canadian dollar, Chinese renminbi, South Korean won, Singaporean dollar, and Nordic currencies. Some are even increasing their gold reserves, recognizing that physical bullion in secure vaults remains accessible even when financial sanctions freeze currency reserves.

For more sophisticated hedging, tools like forward contracts and currency options can help. Forward contracts lock in exchange rates for future transactions without requiring upfront fees, though they prevent benefiting from favorable rate movements. Currency options, on the other hand, offer the flexibility to exchange at a set rate without the obligation, though they come with an upfront premium. In April 2025, Danish pension funds and insurance companies raised their U.S. dollar hedge ratios by 12 percentage points, nearing decade highs in response to sustained dollar weakness and policy uncertainty.

"The case for fully FX-hedging foreign bond investments is evident… Sharpe ratios are meaningfully improved when cross-border fixed income investments are FX-hedged." – Samuel Zief, Global Macro Strategist, J.P. Morgan Private Bank

Compliance is a key consideration. Foreign accounts exceeding $10,000 during the year must be reported under FBAR requirements, and higher balances may also trigger FATCA filings. Holding foreign mutual funds or ETFs directly in offshore accounts can invoke Passive Foreign Investment Company (PFIC) rules, leading to complex reporting and potentially punitive taxes.

Offshore trusts offer an added layer of security. Pairing these structures with tangible assets like foreign real estate (e.g., in Costa Rica) or precious metals stored in secure vaults in Singapore or New Zealand can protect wealth from dollar devaluation while maintaining access to global markets. This approach not only minimizes currency risk but also strengthens a broader strategy for safeguarding assets worldwide.

Regulatory Risks: Policy Shifts and Compliance Challenges

Regulatory risks are increasingly reshaping the landscape of asset protection. A single policy change can disrupt previously effective strategies, exposing assets to scrutiny and compliance challenges. Privacy measures that once shielded assets are now vulnerable due to evolving transparency rules, tax information exchange agreements, and beneficial ownership registries.

The consequences are severe. As of 2023, over €21.5 billion in Russian private assets have been frozen within the European Union. Even those not directly sanctioned face risks, as financial institutions often preemptively close accounts for certain nationalities – like Russian, Venezuelan, or Hong Kong nationals – to sidestep perceived regulatory risks.

Tax reclassifications add another layer of complexity. For example, new IRS regulations could redefine "commercial activity" or "effective control", potentially revoking tax-exempt status for foreign entities. Proposed 2025 rules suggest that veto rights over dividends, budgets, or capital expenditures might trigger effective control – even without majority ownership. Meanwhile, penalties for late foreign trust filings are being reduced under proposed 2024 regulations, dropping from 35% to 5% of the gross reportable amount.

"Regulatory and treaty changes: Jurisdictions regularly update transparency rules, tax information exchange agreements, and beneficial ownership registries. What looked like secrecy five years ago may no longer be so." – Finhelp.io

The demand for investment migration programs in the U.S. surged by over 900% between 2019 and 2024, reflecting growing concerns over domestic regulatory and political risks. In 2024 alone, 4,820 individuals renounced their U.S. citizenship – a 48% jump from 2023 – driven by fears of increasing tax scrutiny and reporting burdens. These trends highlight the importance of proactive measures to navigate shifting policies and tariffs.

Managing Policy Changes and Tariff Risks

Policy changes often create immediate compliance headaches. Sudden reforms, tariffs, or reporting requirements can catch international investors off guard. For instance, the IRS has intensified its focus on "dual-resident" taxpayers. Even if classified as a non-resident for income tax purposes, you might still be treated as a U.S. person for international reporting. Missing required filings can lead to penalties that exceed the account’s value.

To navigate these challenges, it’s crucial to monitor how "effective control" is defined. Regulators are moving beyond simple ownership percentages to assess control based on operational or managerial influence. Keeping partnership stakes below 5% or avoiding veto rights and management roles can help qualify for safe harbors in certain jurisdictions.

Another approach involves leveraging "inadvertent commercial activity" exceptions. Some jurisdictions allow a 180-day window to correct accidental regulatory breaches, preventing permanent classification as a controlled commercial entity. Acting quickly within this timeframe is essential to avoid long-term tax consequences.

Diversifying across jurisdictions also mitigates risks. Maintaining accounts in politically neutral locations like Singapore, Switzerland, or the Cayman Islands can ensure access to funds even if one bank deems your nationality or activities too risky. In this evolving regulatory environment, specialized legal structures are key to maintaining resilience.

Using Offshore Foundations for Regulatory Advantages

Offshore foundations have emerged as a flexible tool for navigating complex regulations. Unlike traditional trusts, foundations offer asset segregation, succession planning, and privacy benefits. Jurisdictions like Anguilla, Liechtenstein, and Panama provide private foundation options tailored to these needs.

Anguilla foundations are particularly appealing, as they keep beneficial ownership details private. Similarly, the Nevis Multiform Foundation Ordinance of 2004 allows entities to switch between trust, company, partnership, or foundation structures based on regulatory requirements.

Foundations also simplify cross-border transactions. Unlike trusts – which may not be recognized everywhere – foundations are widely accepted under civil law systems, making them ideal for holding international assets or managing succession across countries. However, they must be structured carefully to comply with local rules and avoid anti-avoidance measures.

"The spectrum of outbound wealth planning ranges from relatively straightforward international investment diversification to full expatriation." – Suzanne L. Shier, Partner, Levenfeld Pearlstein, LLC

Timing is critical. Offshore structures should be established well before any legal or regulatory challenges arise. Transfers made after a lawsuit begins are often deemed "fraudulent transfers", leaving assets unprotected and potentially subject to penalties. Engaging professional oversight, such as third-party trustees or "protector" provisions, ensures compliance without compromising the structure’s integrity.

While offshore foundations don’t eliminate reporting obligations – such as FBAR (FinCEN Form 114) and IRS Form 8938 – they offer a solid framework for protecting assets while meeting compliance requirements.

Key Regulatory Risks and Mitigation Strategies

The following table summarizes major risks and potential strategies:

| Regulatory Risk Factor | Impact on Asset Protection | Mitigation Strategy |

|---|---|---|

| Transparency Rules | Loss of privacy; automatic data sharing | Use compliant, transparent structures like QPIs |

| Sanctions/De-risking | Frozen assets; account closures | Diversify banking across neutral jurisdictions |

| Tax Reclassification | Higher taxes; loss of exemptions | Monitor "effective control" and "commercial activity" definitions |

| Reporting Failures | Severe penalties (e.g., 5% of assets) | Comply with FBAR, FATCA, and Form 3520 requirements |

The regulatory landscape is in constant flux. Staying informed, adapting to changes, and working with experienced professionals are essential to safeguarding assets. Offshore foundations and trusts are not about concealing wealth – they’re about creating structures that can withstand regulatory pressure while keeping assets secure and accessible.

Offshore Diversification Strategies

Building on the earlier discussion about offshore trusts and regulatory safeguards, spreading assets across multiple jurisdictions adds another layer of protection. By diversifying holdings across countries, you create legal obstacles that can discourage creditor claims. Each country operates under its own legal system, meaning creditors would need to pursue separate legal actions in every jurisdiction – a time-consuming and costly process that often deters litigation entirely.

This approach typically involves combining jurisdictions with layered structures. For instance, a Cook Islands trust might own a Nevis LLC, which holds a Singapore bank account and Swiss franc deposits. This setup forces any legal challenge to navigate multiple court systems, each with its own rules, procedures, and even language barriers. The complexity alone can discourage potential plaintiffs.

Another key aspect is currency diversification. Holding assets in various currencies – like Swiss francs or Singapore dollars – or in tangible assets like gold can protect against the risk of single-currency devaluation. This strategy proved especially useful in early 2025 when the U.S. dollar lost over 10% of its value against a basket of major currencies, marking its worst six-month performance since 1973.

Timing plays a critical role here. Offshore structures must be established well before any legal trouble arises. Transfers made after litigation begins can be labeled as "fraudulent transfers", exposing the assets and possibly leading to penalties. Experts recommend creating these frameworks during stable periods, not during a crisis.

Global Wealth Protection specializes in crafting these multi-jurisdictional setups through offshore trusts and foundations. These structures allow for cross-border asset holding while ensuring compliance with U.S. reporting laws like FBAR and FATCA. This layered strategy helps identify the most suitable jurisdictions for asset protection.

Selecting Jurisdictions for Asset Protection

Not all offshore jurisdictions offer the same level of protection. The best locations share a few common traits: short statutes of limitations on fraudulent transfer claims (usually 1–2 years), high standards of proof (often requiring evidence "beyond reasonable doubt"), and a refusal to enforce foreign judgments. These features create strong barriers for creditors.

Political and economic stability is equally important. Switzerland, for example, manages around $2.2 trillion in international assets, thanks to its neutrality and consistent legal system. Similarly, Singapore, with its AAA-rated stability, saw its assets under management grow to S$5.4 trillion by 2025, with 77% of that coming from foreign clients.

The legal framework also matters. Common law jurisdictions like the Cook Islands and Nevis are known for their specialized trust courts and extensive case law supporting asset protection. On the other hand, civil law jurisdictions like Liechtenstein and Panama excel in structuring foundations, which are ideal for managing wealth across generations.

Modern offshore planning now prioritizes "regulated confidentiality" over outright secrecy. Jurisdictions like Jersey and the Cook Islands use "firewall" provisions to limit public access to trust documents while still complying with legitimate government requests. This approach balances privacy with the transparency required by frameworks like FATCA and the Common Reporting Standard.

Here’s a quick comparison of key jurisdictional features:

| Jurisdiction | Statute of Limitations | Foreign Judgments Recognized? | Best For |

|---|---|---|---|

| Cook Islands | 1–2 years | No | High-risk profiles, lawsuit risk |

| Nevis | 1–2 years | No | Professionals, entrepreneurs |

| Belize | 1 year | No | Budget-conscious formation |

| Cayman Islands | 2–3 years | Limited | Institutional wealth, estate planning |

| Singapore | Varies | Limited | Asian gateway, AAA-rated stability |

| Switzerland | Varies | No (requires full review) | Neutrality, franc stability |

Cost is another factor to consider. Setting up a trust can range from around $5,000 in Belize to over $25,000 in the Cayman Islands. In Nevis, creditors may need to post bonds exceeding $50,000 before filing a claim, adding another layer of deterrence. However, choosing a jurisdiction based solely on cost can backfire if the legal system lacks reliability or strong case law.

Combining Trusts, Companies, and Foundations

Integrating multiple structures creates a robust defense by layering legal protections. For instance, an offshore trust might act as the shareholder of an offshore LLC, which then holds investment portfolios or operates businesses. This "hub-and-spoke" model forces creditors to deal with several entities across various jurisdictions, making legal action both costly and complex. This strategy not only deflects claims but also aligns with the broader goal of mitigating risks through asset dispersion.

"Multi-jurisdictional wealth structuring functions like a diversified investment portfolio. Each jurisdiction contributes something distinctive… so the family is never hostage to a single authority." – Christopher Clayton, Alpha Wealth Group

This setup also balances control and protection. An LLC can handle day-to-day operations – like managing investments or signing contracts – while a trust or foundation provides long-term security and succession planning.

Combining legal systems can further enhance protection. For example, a common law trust in Nevis or the Cook Islands can be paired with a civil law foundation from Liechtenstein or Panama. This approach is especially effective for families managing wealth across multiple regions.

Different entities within the structure can also serve specialized roles. For instance, an Irish company might hold intellectual property to benefit from favorable tax laws, a Dutch entity could centralize dividend flows, and a Swiss account might offer liquidity in a stable currency.

Economic substance is essential for these arrangements to comply with regulations like BEPS. Offshore companies must demonstrate real activity – such as hosting board meetings or employing local staff – to retain tax treaty benefits. Professional trustees and registered offices can help meet these requirements without requiring you to be physically present.

Compliance is non-negotiable. Offshore structures do not exempt you from U.S. tax obligations. You’re still required to file FBAR (FinCEN Form 114) for accounts exceeding $10,000 and IRS Form 8938 for specified foreign assets. The aim is not to hide wealth but to create strong legal barriers that protect assets from private creditors while staying transparent with tax authorities.

Global Wealth Protection offers tailored services to design these integrated structures. From forming offshore companies to introducing clients to reputable foreign banks, they handle operational needs like annual filings and documentation. Their private consultations ensure that each structure aligns with individual risk profiles, whether the goal is to guard against lawsuits, business liabilities, or geopolitical uncertainties.

Conclusion: Managing Risks to Protect Wealth

In 2026, protecting your wealth is about safeguarding what you have, not just focusing on growth. The challenges we’ve discussed – ranging from economic instability to regulatory changes – require a forward-thinking and multifaceted strategy. Diversifying your assets across different classes, regions, currencies, and legal systems can help ensure that trouble in one area doesn’t jeopardize your entire portfolio.

A strong defense often includes offshore legal tools like Asset Protection Trusts and International Foundations, combined with jurisdictional layering in stable financial hubs such as Switzerland, Singapore, and the UAE. Currency diversification is equally important. For instance, after the U.S. dollar fell by over 10% against major currencies in early 2025, relying solely on one currency became a risky move. Pair these strategies with tiered liquidity management – balancing immediate cash, quality fixed-income investments, and long-term growth assets – for a more resilient approach.

As experts emphasize:

"Timing really matters when protecting your money. You need to set things up before any problems start. If you wait until someone sues you, it’s too late." – The Nestmann Group

Preparation is key. Setting up asset protection structures before a crisis hits can shield you from claims of fraudulent conveyance, which often arise when assets are transferred after litigation begins. Such claims can expose your wealth and lead to penalties. With around 5 million new court cases filed in the U.S. in 2023, it’s clear that building these safeguards during stable times is far more effective than scrambling during a crisis.

Global Wealth Protection provides customized solutions to handle complex asset protection needs. Their services include private consultations, offshore trust setups, and company formations. These measures create strong legal barriers to protect your assets from private creditors while ensuring compliance with U.S. reporting requirements like FBAR and FATCA. Whether you’re managing professional risks, business liabilities, or geopolitical challenges, expert advice can help you avoid pitfalls and tailor your strategy to your unique risk profile.

FAQs

Which risks should I monitor monthly to protect my wealth?

To safeguard your wealth, it’s crucial to keep an eye on key risks every month. Pay attention to geopolitical tensions, such as conflicts or sanctions, as these can have ripple effects on global markets. Watch for currency fluctuations, especially if you hold assets in multiple currencies, and stay updated on regulatory changes in the regions where your investments are based.

Beyond these, monitoring macro-financial indicators is just as important. Keep tabs on stock market indices, sovereign risk premiums, and interest rates. These can give you a sense of how markets might react in the near future. By staying informed, you’ll be better equipped to adjust your asset allocation, diversify globally, and maintain enough liquidity to cushion against potential losses.

When is the right time to set up an offshore trust or foundation?

The ideal moment to establish an offshore trust or foundation is before facing any legal, financial, or personal claims. Taking this step early ensures these structures are both effective and compliant when it comes to protecting assets. Many high-net-worth individuals choose to set them up during times of financial stability, incorporating them into broader wealth and estate planning strategies. This proactive approach helps secure their benefits well in advance of any potential risks.

How can I reduce currency risk without triggering tax reporting problems?

To manage currency risk while avoiding tax reporting complications, explore lawful approaches like opening multi-currency accounts or utilizing hedging tools such as forward contracts and options. It’s also crucial to stay compliant with IRS regulations, including FBAR (Foreign Bank and Financial Accounts) and FATCA (Foreign Account Tax Compliance Act), by keeping precise records and ensuring all necessary disclosures are properly filed.