Establishing tax residency abroad can help you significantly reduce your tax burden, but it requires careful planning. For U.S. citizens, this process is more complex due to worldwide income taxation based on citizenship. Here’s a quick breakdown:

- Key Benefits: Exclude up to $132,900 of foreign-earned income (2026) using the Foreign Earned Income Exclusion (FEIE). Some countries, like Panama or the UAE, impose little to no taxes on foreign income.

- Residency Requirements: You may need to spend a certain number of days in the chosen country or show economic ties like property ownership or employment.

- U.S. Filing Obligations: Even abroad, Americans must file Form 1040 and may need to report foreign accounts (FBAR) or assets (FATCA).

- Top Countries: The UAE, Panama, and Georgia are popular for their low or zero-tax systems.

To minimize taxes legally, choose a suitable country, meet residency criteria, and stay compliant with U.S. and local tax laws. Proper documentation, like a Tax Residency Certificate (TRC), is essential. Below, we’ll guide you through the steps.

Step 1: Selecting a Low-Tax Country

What Makes a Country Tax-Friendly

Countries that are considered tax-friendly typically follow one of three systems: zero-tax, territorial, or remittance-based. Zero-tax jurisdictions – such as the UAE, Monaco, and the Bahamas – don’t impose personal income taxes at all. Territorial tax systems, found in places like Panama, Costa Rica, and Paraguay, only tax income earned within their borders, leaving foreign-sourced income untouched. Meanwhile, remittance-based systems – used in countries like Singapore, Malta, and Mauritius – only tax foreign income if you bring it into the country physically.

Your choice should depend on how these systems handle your specific income. For example, if your income is entirely foreign-sourced, a territorial system (like Panama or Georgia) might save you more money compared to a zero-tax country, which could offset the lack of income tax with high VAT, import duties, or other fees. It’s worth noting that zero-tax jurisdictions often rely on VAT rates that can reach up to 20%, along with elevated import duties and administrative costs.

Examples of Low-Tax Countries

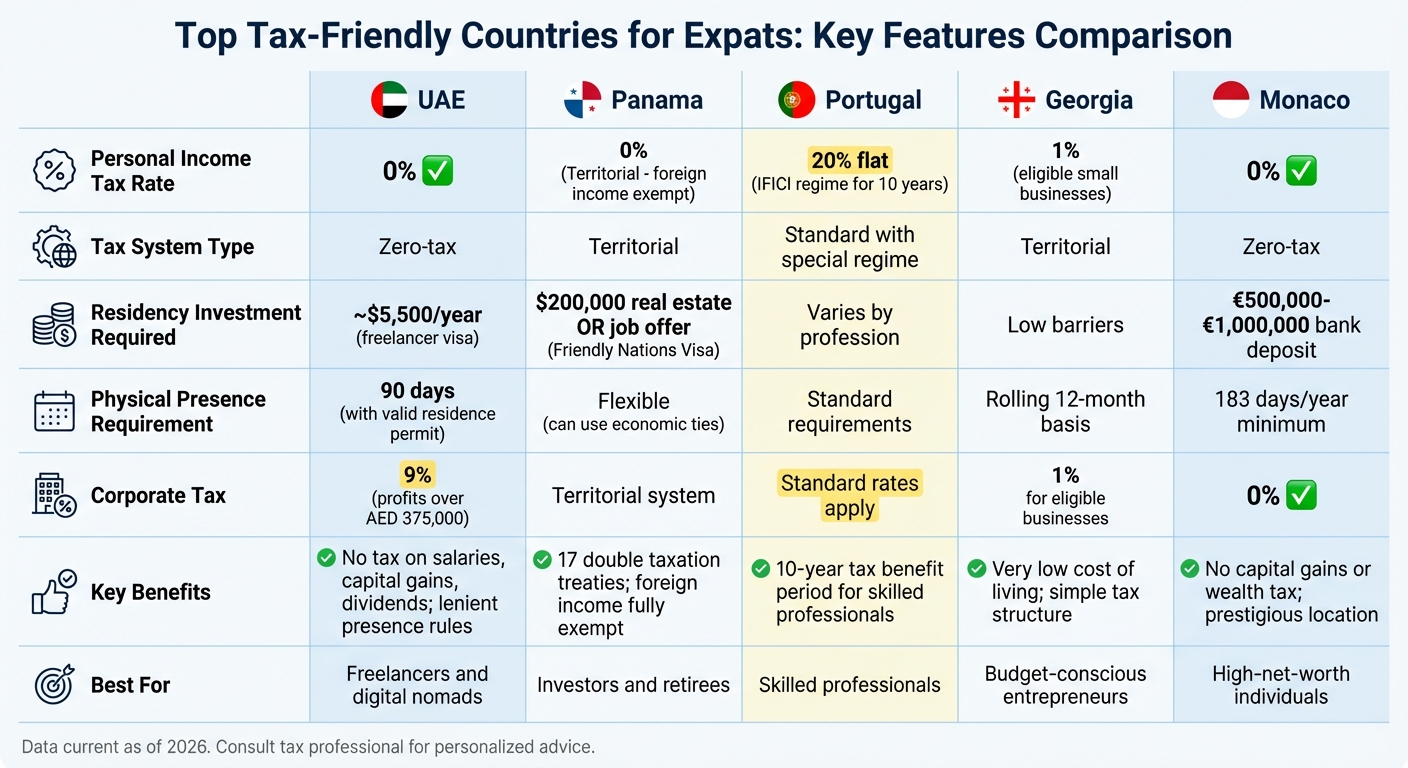

The UAE offers a 0% personal income tax rate on salaries, capital gains, and dividends. However, corporate profits exceeding AED 375,000 are taxed at 9%. Freelancers can secure a visa for around $5,500 annually, and the country has lenient physical presence requirements.

Panama uses a territorial tax system, meaning foreign-sourced income is completely tax-exempt. The Friendly Nations Visa is available with either a $200,000 real estate investment or a local job offer. On the other hand, Portugal’s IFICI regime (a revamped version of the Non-Habitual Resident program) offers skilled professionals a flat 20% tax rate for 10 years. Georgia stands out with a 1% tax rate for eligible small businesses and a very low cost of living compared to other tax-friendly countries.

For those with substantial wealth, Monaco imposes no taxes on capital gains or wealth. However, residency requires a bank deposit of €500,000 to €1,000,000. The Cayman Islands also have no VAT or corporate taxes and boast a strong banking infrastructure, though the cost of imported goods can be extremely high.

How to Choose the Right Country for You

Start by assessing your income sources and picking a tax system that aligns with your needs. If you’re planning a major liquidity event, secure residency in advance to take advantage of lower tax rates. Check for double taxation treaties between your chosen country and the United States to avoid being taxed twice on the same income.

Taxes aside, consider practical factors like lifestyle and work needs. Remote workers should prioritize reliable internet, access to co-working spaces, and time zone compatibility with clients. The country’s international reputation also matters – jurisdictions flagged by the OECD or EU can make banking and compliance more difficult. Physical presence requirements vary widely: the UAE and Panama are flexible, while Monaco mandates at least 183 days of residency per year.

Once you’ve established residency, apply for a Tax Residency Certificate (TRC). This document proves your tax status and activates benefits under double taxation treaties. To strengthen your tax residency claim, maintain local utility bills, rental agreements, and bank statements – these can be crucial if you face an audit from U.S. authorities.

Picking the right jurisdiction is a critical step in lowering your tax liability. Once you’ve made your decision, the next move is to establish legal residency and meet the country’s entry requirements.

sbb-itb-39d39a6

Step 2: Meeting Residency Requirements

Ways to Obtain Residency

Many tax-friendly countries provide multiple pathways to establish legal residency. One common option is through investment-based programs. Take Panama, for instance: its Friendly Nations Visa typically requires a $200,000 real estate investment or a valid job offer. Meanwhile, the Qualified Investor Visa demands an investment of $300,000–$500,000 in real estate, $500,000 in stocks, or a $750,000 bank deposit. This route can sometimes lead to fast-track approval in as little as 30 days. Retirees can also qualify through Panama’s Pensioner Visa by proving a lifetime monthly pension of at least $1,000.

Alternatively, you can establish residency by creating economic ties. This might involve incorporating a local business with commercial contracts or securing a local job. In Panama, demonstrating such ties – like owning property or running a business – can qualify you for tax residency, even if you don’t meet the typical 183-day physical presence requirement.

Understanding the distinction between physical presence and legal residency is crucial for determining your tax status.

Physical Presence vs. Legal Residency Status

Having a residence permit doesn’t automatically make you a tax resident. A residence permit simply grants legal permission to live in a country, whereas tax residency depends on factors like how long you stay and where your primary economic and personal interests lie.

While many countries use the 183-day rule to define tax residency, some also consider your “center of vital interests.” For example, Georgia calculates tax residency on a rolling 12-month basis rather than a calendar year. Other nations, such as the UAE, apply a "90-day test", where spending 90 days in the country with a valid residence permit and maintaining a permanent home or business can qualify you as a tax resident.

The main advantage of formal tax residency is the documentation it provides. A Tax Residency Certificate (TRC) from the local tax authority – such as Panama’s DGI or the UAE’s FTA – serves as crucial proof for foreign tax authorities and allows access to benefits under double taxation treaties.

"Tax residency is not the same as having a visa or residence permit." – Gegidze

Required Documents and Legal Steps

Once your residency status is clear, you’ll need to gather specific documents to legally establish and prove your residency.

Start by obtaining a local tax identification number. In Portugal, this involves securing a Número de Identificação Fiscal (NIF), which can be done through a fiscal representative or in person. In Panama, you’ll need an E-cedula to apply for a tax residency certificate.

The typical application process requires:

- A valid passport (with at least six months’ validity)

- An apostilled criminal background check

- Proof of economic solvency (such as bank statements or letters)

- Proof of address (utility bills or lease agreements)

- Apostilled birth or marriage certificates for dependents

Make sure to notarize and apostille all documents before leaving your home country, as most migration and tax authorities require legalized paperwork. If you’re working with a legal representative, you’ll also need a notarized power of attorney.

To verify your physical presence for the 183-day requirement, keep records like entry and exit stamps, boarding passes, hotel receipts, lease agreements, and utility bills. Some authorities, such as those in Portugal, may request detailed proof of your whereabouts. Finally, apply for your Tax Residency Certificate to formalize your status and secure treaty protections.

Step 3: Organizing Your Finances for Tax Savings

Once you’ve secured foreign residency, it’s time to fine-tune your financial setup to minimize tax obligations. By taking advantage of U.S. tax provisions, setting up offshore accounts or companies, and navigating cross-border tax rules, you can significantly reduce your overall tax burden. Below, we’ll walk through key strategies to achieve this.

Using the Foreign Earned Income Exclusion (FEIE)

The Foreign Earned Income Exclusion (FEIE) is a powerful tool for U.S. citizens living abroad. For 2026, it allows you to exclude up to $132,900 of foreign-earned income – such as wages, salaries, or self-employment earnings – from federal taxes. However, this exclusion doesn’t apply to passive income like dividends, interest, or rental income.

To qualify, you’ll need to establish a foreign "tax home" and meet one of these two tests:

- Physical Presence Test: Spend at least 330 full days outside the U.S. within any 12-month period.

- Bona Fide Residence Test: Show long-term intent to live abroad, such as by opening local bank accounts, getting a local driver’s license, or signing a long-term lease.

Keep detailed travel records, as only full 24-hour periods count toward the Physical Presence Test. While the FEIE reduces taxable earned income, self-employed individuals should note that it doesn’t lower self-employment taxes. Self-employment tax (approximately 15.3%) still applies, unless a Totalization Agreement with your host country is in place.

If you move abroad mid-year, you can prorate the exclusion for the portion of the year you qualify. Additionally, you might combine the FEIE with the Foreign Housing Exclusion, which lets you deduct housing costs – such as rent and utilities – that exceed a base housing amount (e.g., $20,240 for 2025).

Keep in mind: the FEIE applies only to federal taxes. States like California and New York may still tax your worldwide income. To avoid this, consider establishing domicile in a state with no income tax, such as Florida, Texas, or Nevada.

Opening Offshore Bank Accounts and Companies

Setting up offshore structures can help you better manage taxes on foreign-sourced income. Jurisdictions with territorial tax systems – like Panama, Hong Kong, and Singapore – offer significant advantages. In these countries, only locally generated income is taxed, while foreign-sourced income can remain untaxed if properly documented.

For example:

- Panama: Features 17 double taxation treaties to prevent overlapping tax obligations.

- United Arab Emirates (UAE): Offers 0% corporate tax in free zones like DIFC and JAFZA, often paired with long-term tax holidays.

To ensure your offshore company is recognized as a legitimate tax resident, you’ll need to establish "economic substance." This means holding board meetings locally, maintaining a physical office, and appointing local directors. A Tax Residency Certificate (TRC) can confirm your status and unlock treaty benefits, ensuring foreign income remains untaxed by your host country.

For U.S. citizens, worldwide income is still taxable. To mitigate this, you can combine strategies like the FEIE and Foreign Tax Credits. However, be cautious of Controlled Foreign Corporation (CFC) rules, which may tax offshore company profits – even if they aren’t distributed. Compliance with international regulations like the Common Reporting Standard (CRS) and FATCA is also non-negotiable.

Preventing Double Taxation

Because the U.S. taxes citizens on worldwide income, avoiding double taxation is crucial. Here are some tools to help:

- Tax Treaties: The U.S. has treaties with over 70 countries to clarify which nation has the primary right to tax specific income types.

- Foreign Tax Credit (FTC): This allows you to offset U.S. taxes with foreign taxes paid, reducing your overall liability.

- FEIE: While you can’t use the FEIE and FTC on the same income, you can strategically apply one to wages and the other to investment income, depending on what works best.

- Totalization Agreements: These agreements ensure you pay into only one country’s Social Security system, preventing dual contributions.

Here’s a quick comparison of these mechanisms:

| Mechanism | Purpose | Key Requirement |

|---|---|---|

| Tax Treaties | Allocates taxing rights between countries | Must reside in a treaty country |

| Foreign Tax Credit (FTC) | Reduces U.S. tax liability with foreign taxes paid | Must have paid/accrued foreign income tax |

| FEIE | Excludes foreign wages from U.S. taxable income | Must meet Physical Presence or Bona Fide Residence test |

| Totalization Agreements | Prevents dual Social Security taxation | Must be covered by one country’s system |

Planning ahead is key. Establish residency and corporate structures before significant income events to maximize tax efficiency. For example, forming a company in a jurisdiction with favorable tax treaties can simplify tax obligations and reduce the risk of being taxed twice.

Step 4: Staying Compliant with U.S. and Local Tax Laws

Once you’ve optimized your tax strategy abroad, staying compliant with both U.S. and local tax laws is crucial to protecting your savings. Even if you live overseas, U.S. citizens are still taxed on their worldwide income. Keeping up with both U.S. and local tax filing requirements is essential to avoid penalties that could erase any benefits you’ve worked to achieve.

Tax Filing Requirements for U.S. Expats

Even if you don’t owe taxes, you must file a U.S. tax return (Form 1040) if your income exceeds the standard deduction – $16,100 for single filers in 2026. For self-employed individuals, the threshold is even lower: earning just $400 in net self-employment income triggers the filing requirement. Expats get an automatic extension to June 15, but interest on any taxes owed starts accruing from April 15.

In addition to Form 1040, expats must file several forms to report foreign accounts and assets:

- FBAR (FinCEN Form 114): Required if your foreign bank accounts collectively exceed $10,000 at any point during the year. Missing this form can result in penalties of $10,000 per account, per year for non-willful violations – or up to $100,000 or 50% of the account balance for willful violations.

- Form 8938 (FATCA): For reporting foreign financial assets, with thresholds of $200,000 on the last day of the year or $300,000 at any time for single filers living abroad.

Here’s a quick overview of key forms and deadlines:

| Form | Purpose | Threshold | Deadline |

|---|---|---|---|

| Form 1040 | Annual U.S. Tax Return | $16,100 (2026) | June 15 for expats |

| FBAR (FinCEN 114) | Report Foreign Bank Accounts | $10,000 aggregate | April 15 (auto-extension to Oct 15) |

| Form 8938 | Report Foreign Financial Assets | $200,000/$300,000 | Filed with Form 1040 |

| Form 2555 | Claim FEIE | N/A | Filed with Form 1040 |

Additionally, if you maintain ties to certain states like California, New York, Virginia, or South Carolina, you may still owe state taxes unless you formally sever your connections.

While U.S. deadlines are critical, understanding your host country’s tax system is just as important.

Complying with Local Tax Laws

Your new country of residence will have its own tax rules, and knowing them is essential to avoid unexpected liabilities. Some countries, like Panama, Hong Kong, and Singapore, operate on territorial tax systems, meaning they only tax income earned within their borders. This can be advantageous if your income is foreign-sourced. However, accurately identifying your income’s source is key. For instance, in Panama, remote work for a foreign company is typically tax-exempt, but income from services benefiting a local client is taxable.

Obtaining a tax residency certificate from local authorities, as discussed earlier, can help you access treaty benefits and confirm your residency status to both local and U.S. tax authorities. Keep in mind that some countries require annual tax filings even if no taxes are owed, so consulting a local tax professional is highly recommended.

Mistakes to Avoid

Staying compliant isn’t just about filing the right forms – it’s also about avoiding common pitfalls that could jeopardize your tax benefits. One frequent error is assuming that moving abroad ends your U.S. tax obligations. This misunderstanding can result in unfiled returns and mounting penalties. Another mistake is attempting to claim both the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC) on the same income, which is prohibited and will attract IRS scrutiny.

Certain investments, like foreign mutual funds or some life insurance policies, can trigger Passive Foreign Investment Company (PFIC) rules, leading to higher tax rates and the complex Form 8621. Additionally, self-employed individuals should be aware that even if their income is excluded under the FEIE, they may still owe the 15.3% U.S. Social Security and Medicare tax unless a Totalization Agreement exists between the U.S. and their host country.

If you’re behind on filings, the Streamlined Filing Compliance Procedures allow you to catch up without penalties, provided your non-compliance was unintentional. Be diligent about tracking your travel days, as even partial days in the U.S. can disqualify you under the Physical Presence Test. Lastly, serious tax debt can have broader consequences: the IRS can notify the State Department, which may lead to the denial or revocation of your U.S. passport.

Conclusion: Reducing Your Tax Burden Through Foreign Residency

Key Takeaways

Establishing tax residency abroad can significantly lower your tax obligations, but it requires thoughtful planning and execution. The process involves choosing a jurisdiction that matches your financial and lifestyle needs, meeting physical presence and economic substance criteria, optimizing your finances to take advantage of benefits like the Foreign Earned Income Exclusion (FEIE), and adhering to both U.S. and local tax regulations.

It’s crucial to understand the distinction between legal residency and tax residency. As one expert puts it: "While a residence permit hands you the legal right to live in a country physically, a tax residence certificate is a contract between you and a particular country that requires you to pay taxes there". Misunderstanding this difference can result in unexpected tax liabilities or missed opportunities. Additionally, jurisdictions with territorial tax systems – taxing only income earned within their borders – are especially favorable for those with foreign-sourced income.

Achieving minimal taxation hinges on meticulous planning. Whether you’re considering the UAE’s 0% personal income tax, Panama’s territorial system with no wealth or inheritance taxes, or Portugal’s Non-Habitual Resident program, success depends on properly documenting your presence, maintaining economic ties, and ensuring timely compliance with all tax filings. Errors, such as claiming both the FEIE and the Foreign Tax Credit on the same income or missing FBAR deadlines, can lead to steep penalties.

By understanding these essentials, you’re better equipped to move forward confidently.

Why You Need Expert Guidance

The next step in your journey is to seek professional assistance. International tax planning is complex, and mistakes can be costly. An expert can help you navigate the intricacies of U.S. tax laws and foreign residency requirements, ensuring you avoid pitfalls and maximize your tax savings. Beyond just tax rates, professionals will also consider factors like corporate substance rules, remittance policies, and the long-term stability of your chosen jurisdiction.

Global Wealth Protection is one such firm that specializes in assisting entrepreneurs and investors with tax residency and asset protection strategies. Their advisors can create a tailored plan that simplifies the process, covering everything from residency and tax reduction to asset diversification. With expert support, what might feel overwhelming becomes a clear and actionable path to legally reducing your tax burden as much as possible.

FAQs

Do I have to give up U.S. citizenship to lower my taxes abroad?

U.S. citizenship does not need to be relinquished to reduce your tax burden while living abroad. However, as a U.S. citizen, you’re required to report and pay taxes on your worldwide income, no matter where you reside. That said, certain exclusions or tax credits under U.S. tax laws can help lower the amount of taxable income you owe.

How do I prove tax residency if I don’t stay 183 days in one country?

If you don’t spend 183 days in a single country, you can still establish tax residency by demonstrating significant ties. This could include factors like where your family lives, where you own property, or where your primary business operations are based – essentially, your center of vital interests. Other legal criteria may also apply, depending on the country.

To support your case, it’s crucial to keep thorough records. Document your travel dates, economic activities, and any residency-related paperwork. Additionally, some countries offer residency through investment or special visa programs, which may allow you to qualify even without meeting the 183-day threshold.

Will the IRS still tax me if I use the FEIE and foreign bank accounts?

Yes, the IRS can still impose taxes on you even if you take advantage of the Foreign Earned Income Exclusion (FEIE) and maintain foreign bank accounts. However, these options can help lower or even eliminate your U.S. tax liability – but only if you meet the specific eligibility requirements and fulfill all reporting obligations, such as FBAR (Foreign Bank Account Report) and FATCA (Foreign Account Tax Compliance Act).