If you’re an investor or entrepreneur looking to keep your profits untouched by capital gains tax, there are eight countries worth considering: United Arab Emirates, Cayman Islands, Bermuda, Bahamas, Monaco, Singapore, Hong Kong, and Switzerland. These jurisdictions have policies that allow you to retain 100% of your gains, making them attractive for wealth preservation and minimizing tax liabilities. This strategy is a core component of offshore asset protection for high-net-worth individuals.

Here’s a quick breakdown:

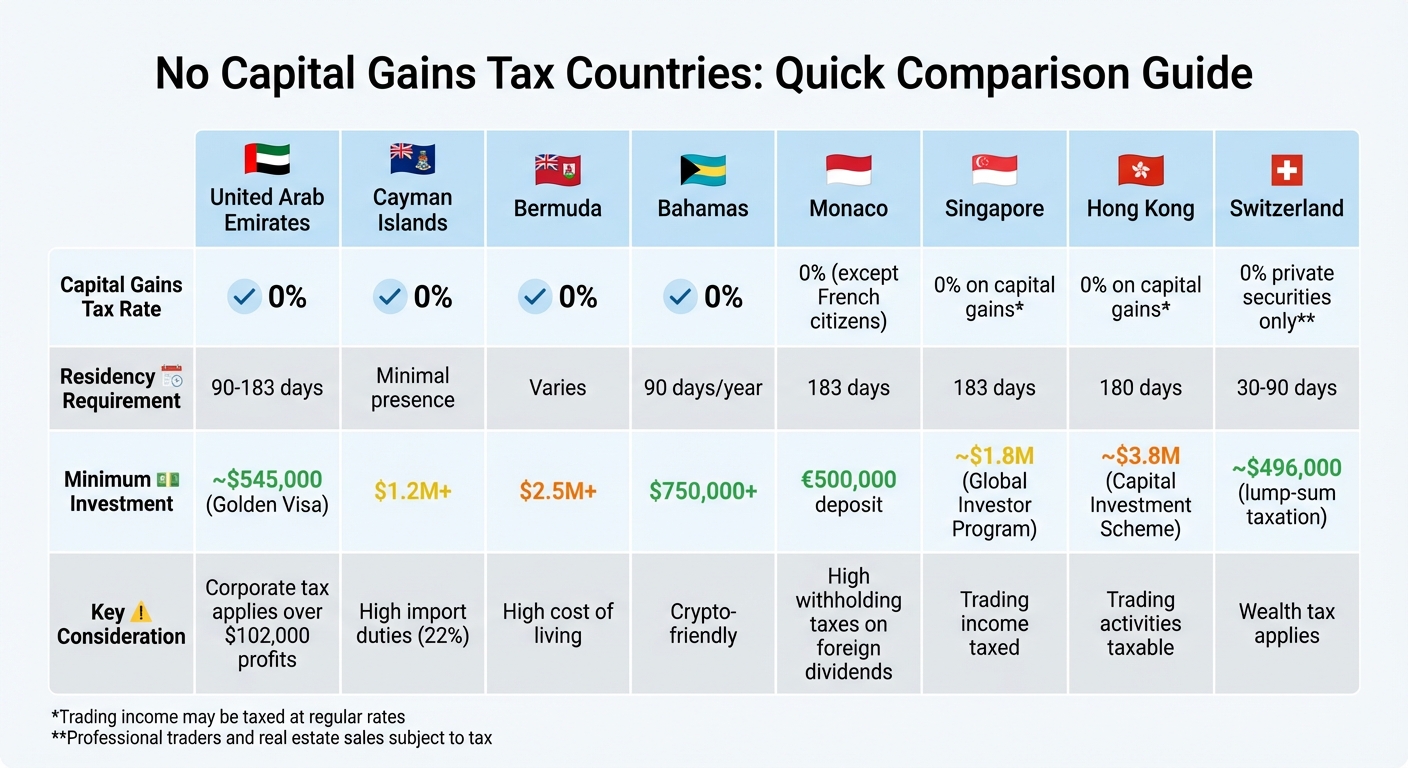

- United Arab Emirates: No capital gains tax for individuals; residency options include the Golden Visa (investment ~$545,000).

- Cayman Islands: No income or capital gains tax; residency requires investments starting at $1.2 million.

- Bermuda: No income or capital gains tax; high living costs and some indirect taxes apply.

- Bahamas: Tax-free on income and gains; real estate investments of $750,000+ qualify for residency.

- Monaco: No capital gains tax, but French citizens face exceptions; residency requires a €500,000 bank deposit.

- Singapore: No tax on capital gains unless classified as trading income; residency via investments of ~$1.8 million.

- Hong Kong: No capital gains tax, but trading activities may trigger taxation; residency options available.

- Switzerland: No tax on private securities gains, but wealth tax applies; residency via lump-sum taxation (~$496,000).

Quick Comparison

| Country | Capital Gains Tax | Residency Requirement | Minimum Investment | Key Note |

|---|---|---|---|---|

| UAE | 0% | 90-183 days | ~$545,000 (Golden Visa) | Corporate tax applies over $102,000 profits |

| Cayman Islands | 0% | Minimal presence | $1.2M+ | High import duties |

| Bermuda | 0% | Varies | $2.5M+ | High cost of living |

| Bahamas | 0% | 90 days/year | $750,000+ | Crypto-friendly |

| Monaco | 0% (except French) | 183 days | €500,000 deposit | High withholding taxes on foreign dividends |

| Singapore | 0% on capital gains | 183 days | ~$1.8M (Global Investor Program) | Trading income taxed |

| Hong Kong | 0% on capital gains | 180 days | ~$3.8M (Capital Investment Scheme) | Trading activities taxable |

| Switzerland | 0% private securities | 30-90 days | ~$496,000 (lump-sum taxation) | Wealth tax applies |

These countries offer unique tax advantages, but residency requirements and indirect costs vary. Always consult with a tax professional to ensure compliance and maximize benefits.

1. United Arab Emirates

No Capital Gains Tax Confirmation

The UAE offers a tax-friendly environment with zero capital gains tax and no personal income tax. This means individuals can retain the full profits from shares, portfolios, or real estate transactions. Additionally, the country imposes no inheritance, estate, gift, or annual property taxes, making it an attractive destination for wealth preservation. However, tax considerations differ for individuals and corporate entities.

"The UAE continues to support investment and business growth through its tax-friendly framework. With zero capital gains tax for individuals and a competitive system for corporates, it remains a global hub for wealth and opportunity." – GTAG

Tax Policy Details

For individuals, the tax system is straightforward – no capital gains tax applies. On the corporate side, profits above AED 375,000 (around $102,000) are taxed at 9%. However, corporate gains are exempt if holdings represent at least 5% ownership and are held for 12 months.

The UAE dirham’s peg to the US dollar provides currency stability, a key advantage for American investors. Moreover, the absence of Controlled Foreign Corporation (CFC) rules means individuals can hold foreign assets without needing to report them locally.

Residency or Citizenship Requirements

Residency rules play a significant role in accessing the UAE’s tax benefits. Tax residency can be established by spending 183 days in the country within any 12-month period or by demonstrating that the UAE is your financial and personal center. A valid residence permit and as little as 90 days’ presence may suffice for the latter.

The UAE offers long-term residency options like the Golden Visa, which requires a 10-year commitment and an investment of AED 2,000,000 (roughly $545,000). Alternatively, a standard investor visa is available with a renewable 2-year permit tied to a property investment of AED 750,000 (about $204,000).

Most residency visas are flexible, requiring only periodic visits – typically every 6 to 12 months – to remain valid.

Investor Suitability

The UAE’s policies make it a compelling choice for high-net-worth individuals, particularly founders planning business exits or investors managing large portfolios. If you frequently realize gains from stocks or real estate, the absence of capital gains tax can result in substantial savings.

For those severing ties with high-tax jurisdictions, obtaining a Tax Residency Certificate from the UAE Ministry of Finance can be a vital step. Corporate investors can also structure their holdings to meet the 5% shareholding and 12-month holding period required for tax exemptions.

sbb-itb-39d39a6

2. Cayman Islands

No Capital Gains Tax Confirmation

The Cayman Islands stands out for its complete absence of taxes on personal income, capital gains, inheritance, and estates. Instead of relying on direct taxation, the government generates revenue through alternative means like work permit fees, import duties (averaging 22% on goods), and tourism-related income.

"There are no income or capital gains taxes for individuals in the Cayman Islands. This is the case regardless of the circumstances by which the individual has obtained residency." – Carey Olsen

That said, there are still some indirect taxes to consider. For example, real estate transactions incur a 7.5% stamp duty, and establishing a trust involves a one-time CI$40 stamp duty. Additionally, economic substance rules require many registered companies to maintain a physical presence in the Cayman Islands, although private wealth structures often enjoy exemptions or reduced obligations.

Residency or Citizenship Requirements

Gaining permanent residency in the Cayman Islands typically involves a real estate investment of at least USD 2.4 million, with the requirement to spend just one day on the islands annually. Another option is a 25-year residency certificate, which requires an investment of approximately USD 1.2 million and a 30-day presence each year. Other pathways cater to business owners or remote workers.

For entrepreneurs, the Substantial Business Presence route is available to individuals holding at least a 10% stake in an approved business. Remote workers can apply through the Global Citizen Concierge Program, which requires an annual income of at least USD 100,000 for individuals or USD 150,000 for couples. After maintaining legal residence for five years, individuals may apply for British Overseas Territories Citizenship, which can eventually lead to full UK citizenship.

These residency options highlight the Cayman Islands’ focus on attracting investors and professionals who value asset security and global mobility.

Investor Suitability

The Cayman Islands is particularly appealing to ultra-high-net-worth individuals seeking a tax-neutral environment that safeguards their wealth while offering flexibility. The minimal physical presence requirements – just one day annually for some residency options – make it ideal for globally mobile investors.

For those planning major financial events, such as business exits or managing large investment portfolios, the lack of capital gains taxes is a major draw. However, the limited network of double tax treaties means investors need to properly exit their previous tax jurisdictions to avoid dual taxation. If a Tax Residency Certificate is needed for compliance with foreign authorities, individuals should plan to spend at least 90 days on the islands.

3. Bermuda

Bermuda’s tax framework plays a key role in preserving profits while offering strong asset protection options for global investors.

No Capital Gains Tax Confirmation

Bermuda operates under a zero-tax system, meaning no personal income, capital gains, or withholding taxes are imposed on individuals. This policy applies equally to both residents and non-residents, ensuring that profits from investments remain untaxed locally.

"Bermuda is a premier zero-tax jurisdiction… There are no personal income, capital gains, or withholding taxes, and corporate entities benefit from a stable regulatory regime aligned with OECD standards." – Black Ledger

Instead of relying on direct taxes, Bermuda generates revenue through other means, such as a payroll tax that ranges from 5% to 12% for higher earners, and customs duties, which can exceed 25% on imported goods. Additionally, starting January 1, 2025, Bermuda introduced a 15% corporate income tax, but this only applies to large multinational corporations with annual revenues exceeding €750 million, leaving smaller businesses unaffected.

Residency or Citizenship Requirements

For those seeking residency, Bermuda offers the Economic Investment Residential Certificate (EIRC). This program requires a minimum investment of $2,500,000 in local assets like real estate, business ventures, or government bonds. The application fee is about $2,625, and investors must spend at least 90 days per year in Bermuda during the first five years to maintain their status.

Remote workers and digital nomads can take advantage of the Work from Bermuda Certificate, priced at $263, which allows them to stay for one year without being taxed on foreign income. Entrepreneurs also have the option to apply for the Global Entrepreneur Work Permit for $1,955, granting a year to establish a business before transitioning to long-term residency. However, Bermuda does not provide one of the simplest citizenship programs via direct investment. "Bermudian Status" is typically reserved for individuals with family ties or long-term marital connections.

Tax Policy Details

Bermuda’s zero capital gains tax is undeniably appealing, but the high cost of living – estimated at 260% of New York City’s – makes it one of the most expensive places in the world. Additionally, stamp duty on Bermuda-based property in a deceased estate can climb to 21% for properties valued above $2 million.

| Estate Value (Bermuda Property) | Stamp Duty Rate |

|---|---|

| Up to $100,000 | 0% |

| $100,000 to $200,000 | 5.25% |

| $200,001 to $1,000,000 | 10.5% |

| $1,000,001 to $2,000,000 | 15.75% |

| Over $2,000,000 | 21% |

To reduce exposure to these costs, investors often focus on "non-Bermuda property" like shares in exempted companies or foreign assets, which are not subject to local estate taxes.

These financial realities, combined with Bermuda’s regulatory advantages, create a specialized environment that appeals to a select group of investors.

Investor Suitability

Bermuda primarily caters to ultra-high-net-worth individuals. The jurisdiction is a global hub for industries like insurance, reinsurance, and investment funds, offering strong asset protection through its trust laws and firewall legislation, which shield Bermudian trusts from foreign court rulings. Investors can also utilize the Segregated Accounts Company (SAC) structure, which is ideal for managing complex portfolios due to its asset segregation capabilities. However, the high banking fees and setup costs highlight the exclusive nature of Bermuda’s market.

4. Bahamas

The Bahamas offers a simple, tax-free environment just a short distance from Florida, making it a popular choice for North American investors and entrepreneurs.

No Capital Gains Tax

The Bahamas does not tax profits from selling real estate, shares, businesses, or other assets, whether you’re a resident or non-resident. This tax-free policy also applies to personal income, corporate profits, wealth, inheritance, and gifts.

"The Bahamas stands out as one of the few countries in the world that does not impose any form of direct taxation on individuals." – Christoph Albeck, Dec 18, 2025

To fund public services, the government relies on a 10% Value-Added Tax (VAT) on most goods and services, reduced from 12% in 2022. Additional revenue comes from import duties, which range from 0% to 75% depending on the product.

Residency and Citizenship Options

Permanent residency in the Bahamas is available for investors who purchase real estate worth $750,000 or more. For those needing a formal Tax Residency Certificate, the minimum property investment increases to $1,500,000. This certificate requires spending at least 90 days annually in the Bahamas and no more than 183 days in any other single country.

The Bahamas is also crypto-friendly. The Digital Assets and Registered Exchanges (DARE) Act of 2020 provides a clear legal framework for cryptocurrency businesses, and crypto gains are not taxed. However, U.S. citizens remain subject to taxation on worldwide income, which may limit the benefits of Bahamian tax laws unless they choose to renounce their U.S. citizenship.

Understanding both residency requirements and indirect tax obligations is key for effective planning.

Tax Policy Breakdown

While there are no capital gains taxes, indirect costs can arise. For instance, real estate transactions incur stamp duties: 2.5% on properties under $100,000 and 10% on properties valued at $100,000 or more. Property taxes are also applied to owner-occupied homes, with the first $250,000 exempt, 0.75% on the next $250,000, and 1% on amounts above $500,000.

Businesses in the Bahamas must register for VAT if their annual turnover exceeds $100,000 and pay a business license fee, which ranges from a flat $100 to 3% of turnover, depending on revenue. Additionally, social security contributions are required: 3.9% for employees, 5.9% for employers, and 9.8% for the self-employed.

Who Benefits Most?

The Bahamas is particularly appealing to North American investors looking for a nearby tax haven. Its close proximity to the U.S. makes it convenient for travel while maintaining tax residency. The jurisdiction is ideal for real estate investors, digital asset entrepreneurs, and business owners who can manage the indirect costs while enjoying the benefits of a no-income-tax system. This setup allows investors to focus on protecting their assets and maximizing their profits.

5. Monaco

Monaco has been Europe’s only zero-tax haven for individuals since 1869, offering a tax-free lifestyle with no personal income, capital gains, or wealth taxes. This historical policy continues to attract investors seeking financial advantages in a luxurious setting.

No Capital Gains Tax

Monaco residents enjoy a 0% tax rate on capital gains, whether it’s from stocks, bonds, real estate, or cryptocurrency. Additionally, there is no wealth tax or inheritance tax for direct-line heirs.

However, Monaco’s limited network of double taxation agreements – covering just 10 jurisdictions – can lead to withholding taxes of 30–35% on foreign dividends from countries like the United States or Switzerland. This rate is nearly double what residents in France or the UK typically face.

"Monaco residents face withholding taxes of 30-35% at source on foreign dividends (double what residents of France or the UK pay). This is one of the most misunderstood aspects of Monaco taxation." – Marc Cantavella, International Tax Expert

Residency and Citizenship Requirements

To establish tax residency in Monaco, individuals must spend at least 183 days per year in the country or demonstrate that Monaco is their primary economic base. Applicants need to provide:

- Proof of accommodation

- A clean criminal record

- Health insurance

- A bank deposit of $550,000 to $1,100,000

French nationals, however, remain largely subject to French income tax due to a 1963 treaty.

Tax Policy Details

While Monaco imposes no personal income tax, it funds public services through a 20% VAT. Real estate transactions come with acquisition costs of 6.25% for transparent ownership and 11% for opaque structures.

For businesses, corporate tax applies at 25% if more than 25% of revenue is generated outside Monaco. New companies benefit from a 0% corporate tax rate for their first two years.

Investor Suitability

Monaco is an attractive option for high-net-worth individuals whose income stems from salaries, local business ventures, or real estate. Entrepreneurs who generate at least 75% of their revenue locally can avoid corporate taxes entirely. However, investors relying heavily on U.S. or Swiss dividends should carefully consider the impact of high withholding taxes.

This environment is ideal for preserving capital gains and safeguarding wealth, making it a strategic choice for those focused on asset protection and financial stability.

6. Singapore

Singapore, known as a global financial hub, offers a 0% capital gains tax on assets like stocks, bonds, real estate, and cryptocurrencies. This policy applies to both residents and non-residents, making it a compelling option for international investors without requiring citizenship.

No Capital Gains Tax: How It Works

The Inland Revenue Authority of Singapore (IRAS) uses a "Badges of Trade" test to differentiate non-taxable capital gains from taxable income. For corporate investors, the "Safe Harbour" rule provides clarity: any gains from share disposals are exempt if the company holds at least 20% of the ordinary shares for a minimum of 24 months.

"Singapore’s policy of not taxing capital gains is driven by economic considerations… supporting the country’s position as a global financial hub." – BBCIncorp

This tax-friendly environment is just one part of Singapore’s broader appeal for investors.

Residency and Citizenship: What to Know

To be considered a tax resident in Singapore, individuals typically need to spend at least 183 days per year in the country or show strong economic ties, such as employment, long-term leases, or banking relationships. For those looking to establish a more permanent presence, the Global Investor Programme (GIP) offers a pathway to permanent residency with a minimum investment of S$2.5 million (roughly $1.8 million) into a new or existing business, or an approved fund.

Citizenship isn’t necessary to enjoy the zero capital gains tax, but residency status can influence other costs. For example, foreigners buying residential property may face an Additional Buyer’s Stamp Duty (ABSD) of up to 60%. It’s also worth noting that Singapore doesn’t allow dual citizenship for adults, requiring naturalized citizens to renounce their original nationality.

These residency options, combined with the tax benefits, make Singapore a standout choice for global investors.

Tax Structure: Beyond Capital Gains

Singapore’s tax system includes a progressive personal income tax, with the top rate reaching 24% for income over S$1 million starting in 2024. Corporate tax is a flat 17%, and newly established companies may qualify for various tax exemptions during their early years. The Goods and Services Tax (GST) is set at 9%.

Operating under a territorial tax system, Singapore taxes only income earned within the country. Foreign-sourced income is generally exempt for individuals. However, since 2024, companies without sufficient economic substance in Singapore may face taxes on certain foreign-sourced capital gains. Additionally, Singapore has no inheritance, estate, or gift taxes, simplifying wealth transfers across generations.

Best Fit for Investors

Singapore is particularly appealing to long-term investors and entrepreneurs who can demonstrate clear investment intent rather than engaging in frequent trading. Crypto investors, for example, are advised to use separate wallets for personal and business transactions to clearly establish capital gains status. Keeping detailed records of purchase and sale dates, along with the purpose of the investment, is crucial for classifying gains as capital.

Moreover, Singapore benefits from an extensive network of double taxation agreements, reducing withholding taxes on foreign dividends. Together, these policies solidify Singapore’s reputation as a top destination for wealth preservation and asset protection.

7. Hong Kong

Hong Kong’s zero capital gains tax policy for both individuals and corporations has long been a magnet for investors and entrepreneurs. Its territorial tax system, detailed in Section 14 of the Inland Revenue Ordinance (IRO), ensures that profits from the sale of capital assets – like stocks, bonds, and real estate – are exempt from Profits Tax. This setup applies regardless of residency, as only income sourced within Hong Kong is taxed.

No Capital Gains Tax Confirmation

Capital gains on a wide range of assets, including financial instruments and property, are not taxed. However, if the Inland Revenue Department (IRD) considers the transactions to be trading activities rather than passive investments, the gains are subject to Profits Tax. To make this determination, the IRD uses a "six badges of trade" test, which evaluates factors like transaction frequency, holding period, and intent.

"Profits tax shall be charged… on every person carrying on a trade, profession or business in Hong Kong in respect of his assessable profits… (excluding profits arising from the sale of capital assets)." – Section 14 of the Inland Revenue Ordinance

For corporations, Profits Tax is applied at two levels: 8.25% on the first HK$2 million (around $256,000 USD) and 16.5% on earnings above that. Unincorporated businesses face rates of 7.5% on the first HK$2 million and 15% on the remainder. While long-term capital gains remain untaxed, short-term trading gains are taxed under these standard rates.

Residency or Citizenship Requirements

Hong Kong’s tax benefits are not tied to residency or citizenship. Tax liability depends entirely on whether income is sourced within the jurisdiction. However, for those seeking residency, programs like the Quality Migrant Admission Scheme (QMAS) or the Investment as Entrepreneur visa offer pathways to settle in Hong Kong. Permanent Residency is typically available after seven years of continuous residence. It’s worth noting that since January 1, 2023, the Foreign-Sourced Income Exemption (FSIE) regime may subject certain offshore capital gains earned by entities to Profits Tax if they lack economic substance in Hong Kong. Individuals, however, remain unaffected.

Tax Policy Details

Hong Kong’s broader tax landscape further solidifies its appeal. Dividend and interest incomes are not taxed, and there is no VAT or GST. However, stamp duty applies to transfers of Hong Kong stocks and property. Personal income tax follows a progressive structure, with rates generally capped between 15% and 17%. Share options granted through employment are subject to Salaries Tax when exercised and sold. On the international front, Hong Kong has established Comprehensive Double Taxation Agreements with 49 jurisdictions as of 2024, reducing tax complexities for cross-border investors.

Investor Suitability

Hong Kong’s tax framework is particularly attractive for those focused on wealth preservation. Founders and holding companies benefit from the absence of withholding taxes on dividends and interest. Investors should maintain thorough records to confirm long-term holdings and avoid classification as trading activities, which are subject to taxation under the "six badges of trade" test. With its extensive tax treaty network and zero capital gains tax, Hong Kong offers a strong foundation for safeguarding assets and implementing effective wealth management strategies.

8. Switzerland

Switzerland takes a unique approach to capital gains taxation. While individuals enjoy tax-free gains on private securities, the country offsets this with an annual wealth tax based on total asset values.

No Capital Gains Tax Confirmation

In Switzerland, private investors benefit from tax-free gains on private securities. For business founders, selling company shares can also qualify for tax exemption – provided the shares are held as private assets rather than business inventory. However, Swiss tax authorities use strict criteria to distinguish private investors from "professional securities traders." If classified as a professional trader, all gains are taxed as self-employment income and are subject to social security contributions.

Swiss courts have consistently upheld this distinction, ensuring tax-free treatment for qualifying private gains.

"The realization of a tax-free capital gain preconditions the (profitable) sale of private assets. By contrast, gains from the sale of business assets are in any case subject to income tax and social security contributions." – Dominic Nazareno and Christian Attenhofer, Certified Tax Experts

Real estate is an exception. Property sales are taxed by cantonal governments, though longer holding periods often reduce the tax rate significantly – by 50% to 70% after four to five years of ownership.

Although Switzerland offers appealing tax advantages, the annual wealth tax adds an extra layer of consideration for investors.

Residency or Citizenship Requirements

Switzerland’s residency options further shape its tax landscape. Residency is triggered after 30 days of physical presence with gainful employment or 90 days without employment. For wealthy foreigners who don’t work in Switzerland, the lump-sum taxation regime offers an alternative. Under this system, taxes are based on living expenses rather than actual income. Eligibility requires foreign nationality, no gainful employment in Switzerland, and establishing Switzerland as the primary residence.

The federal minimum taxable expenditure base for this regime is CHF 434,700 (around $496,000 USD), though annual tax burdens typically range from CHF 200,000 to over CHF 500,000 depending on the canton. After 10 years of continuous residence – or 5 years for US, Canadian, and certain EU/EFTA nationals – investors can apply for permanent residency (C permit).

Tax Policy Details

To maintain private investor status and ensure tax-free gains, individuals must follow specific guidelines. These include holding securities for at least six months, keeping transaction volumes low relative to total wealth, using leverage only for hedging, and ensuring trading profits are not their primary income source.

| Factor | Private Investor (Low Risk) | Professional Trader (High Risk) |

|---|---|---|

| Holding Period | Long-term (e.g., >6 months) | Frequent short-term trading |

| Financing | Self-funded | Heavy use of leverage |

| Income Source | Salary or business income | Trading profits as primary income |

| Derivatives | Hedging only | Speculative trading |

| Transaction Volume | Low turnover | High turnover relative to portfolio |

Federal income tax tops out at 11.5%, while combined cantonal and municipal rates can range from 20% to over 40%. The wealth tax applies at rates between 0.1% and 1% for individuals with assets exceeding CHF 50,000 (about $57,000 USD). Dividends from qualifying participations (holdings of at least 10%) receive a roughly 30% reduction in federal and cantonal tax rates. Switzerland imposes no exit taxes on individuals unless commercial assets with hidden reserves or certain pension benefits are moved out of the country.

Investor Suitability

For those prioritizing long-term wealth preservation, understanding Switzerland’s tax policies is essential. The country is ideal for long-term investors who can document their strategies and avoid high-frequency trading. Business founders should carefully structure their assets before establishing residency to ensure that any capital gains are classified as private assets.

Switzerland combines a tax-free environment for private securities with a stable legal framework, making it attractive for wealth protection. However, the wealth tax and cantonal income taxes mean it doesn’t offer the same level of simplicity as some zero-tax jurisdictions. For US citizens, the US-Switzerland double tax treaty provides relief by allowing Swiss taxes to be credited against US tax liabilities, preventing double taxation.

Comparison Table

The table below highlights key factors for reducing capital gains tax liabilities in various jurisdictions.

| Jurisdiction | CGT Status | Residency Requirement | Minimum Investment | Key Consideration |

|---|---|---|---|---|

| United Arab Emirates | 0% on personal gains | 90 days (with nexus) or 183 days | ~$545,000 for Golden Visa | Corporate tax and VAT may apply to business activities |

| Cayman Islands | 0% (no income tax) | Varies by permit type | Varies by program | 22% import duty on most goods; high cost of living |

| Bermuda | 0% (no income tax) | Varies by permit type | Varies by program | High indirect costs; robust legal framework |

| Bahamas | 0% (no income tax) | Varies by permit type | Varies by program | Close proximity to the U.S.; elevated property fees |

| Monaco | 0% (except French citizens) | 183 days | €500,000 bank deposit | Prestigious location with very high living costs |

| Singapore | 0% (capital gains only)* | 183 days | ~$7.4 million for Global Investor Program | Gains from trading may be taxed; operates under a territorial system |

| Hong Kong | 0% (capital gains only)* | 180 days | ~$3.8 million for Capital Investment Entrant Scheme | Territorial tax system; local business gains may be taxable |

| Switzerland | 0% (private securities only)** | 30–90 days depending on employment | CHF 434,700 (~$496,000) for lump‐sum taxation | Private investors enjoy tax‐free capital gains; real estate sales can be taxed up to 50% |

*Gains classified as "trading income" are taxed at regular rates if trading frequency is high.

**Professional traders and real estate sales are subject to taxes; strict criteria distinguish private investors from traders.

Most jurisdictions require at least 183 days of residence annually, though the UAE allows 90 days with appropriate permits. Establishing genuine tax residency is critical for accessing these benefits. It’s worth noting that investors from countries like the U.S., U.K., Australia, or Canada may face exit taxes on unrealized gains when changing residency. Additionally, global reporting standards necessitate a legitimate residency change.

This overview provides a snapshot of how different jurisdictions cater to investors aiming to optimize their capital gains strategies.

Conclusion

Relocating to a jurisdiction with no capital gains tax can play a critical role in preserving wealth for investors and entrepreneurs during liquidity events. Take, for example, a German tech entrepreneur or a global portfolio manager – both managed to sidestep hefty tax liabilities by strategically relocating, showcasing how these jurisdictions can directly influence financial outcomes.

But the benefits extend beyond just tax savings. These locations also provide geopolitical diversification, simplify financial planning for expatriates, and allow profits to be reinvested in full without immediate tax deductions. With capital gains tax rates climbing in the UK and EU, the trend of moving to zero-CGT jurisdictions is gaining traction. However, achieving these advantages requires careful and deliberate planning.

Success in these relocations hinges on meeting strict requirements. Tax authorities expect proof of economic substance, which includes spending over 183 days in the new jurisdiction, securing local housing, and establishing genuine local connections. As Project Black Ledger aptly stated:

"Zero-tax jurisdictions aren’t a magic bullet; they’re strategic tools that, when used wisely, let you keep more of what you earn."

Investors also need to be cautious about how their activities are classified. For instance, in places like Switzerland and Singapore, gains can be taxed at rates as high as 33% if authorities determine the activity falls under professional trading instead of private investment. U.S. citizens, in particular, must account for ongoing tax obligations in their home country, including citizenship-based taxation and potential exit taxes on unrealized gains. Consulting experienced cross-border tax and legal professionals is essential to navigate these complexities.

Tax laws are always evolving. For example, Singapore introduced new regulations for foreign-sourced gains in 2024, and other jurisdictions may follow suit. Given the intricacies of international tax systems and residency rules, professional guidance ensures your relocation strategy aligns with both your home country’s requirements and those of your destination. This approach underscores the importance of informed decision-making in safeguarding wealth and protecting assets through strategic jurisdictional planning.

FAQs

Do I still owe U.S. tax if I move to a 0% capital gains tax country?

Yes, even if you move to a country with a 0% capital gains tax rate, you may still owe U.S. taxes on those gains. The U.S. tax system requires its citizens and residents to report and pay taxes on their worldwide income, including capital gains, no matter where they live.

What steps prove I really changed tax residency (and avoided dual residency)?

To establish a change in tax residency and avoid dual residency complications, it’s essential to show clear intent and have supporting evidence. Here’s what you should focus on:

- Update official documents: Get a driver’s license in your new state or country and register to vote there.

- Shift financial ties: Move your primary banking activities to institutions in your new location and cut financial connections with your previous residence.

- Track your time: Maintain detailed records of where you spend your days, ensuring you meet the residency requirements of your new location – like staying there for more than 183 days if applicable.

These steps help demonstrate your commitment to the new residency and can protect you from overlapping tax obligations.

How do I avoid my gains being treated as taxable “trading income”?

To ensure your investment gains aren’t classified as taxable “trading income,” consider relocating to or creating investment structures in regions that don’t impose capital gains taxes. It’s crucial to comply fully with the laws in these areas to safeguard your earnings legally. Working with a qualified professional can help you understand and meet the specific legal and financial requirements of these jurisdictions.