Wealthy individuals use offshore banking to protect assets, reduce taxes, and access global investments. By 2026, over 60% of the wealthiest 0.01% maintain foreign accounts, leveraging legal systems in jurisdictions like Switzerland, the Cayman Islands, and Singapore. These accounts offer advanced protections, tax deferral, and currency diversification, while also complying with international regulations like FATCA and CRS. Key strategies, such as structuring offshore trusts, include:

- Asset Protection: Jurisdictions like the Cook Islands and Nevis block foreign court rulings and require high bond payments for creditor claims.

- Tax Optimization: Offshore accounts allow tax deferral and help avoid double taxation in tax-neutral locations.

- Global Investments: Access to exclusive opportunities in private equity, venture capital, and emerging markets.

Modern offshore banking is fully compliant with global regulations, including FATCA and CRS, ensuring transparency while safeguarding wealth. However, successful use requires proactive planning and professional guidance to navigate complex legal frameworks and avoid risks.

Key Takeaways:

- Offshore accounts shield assets from lawsuits and domestic instability.

- Tax-neutral jurisdictions reduce overall tax burdens.

- Multi-jurisdiction strategies protect against economic and political risks.

This guide explains how high-net-worth individuals use these tools to secure and grow their wealth.

Why HNWIs Use Offshore Banking

Offshore banking addresses three core priorities for high-net-worth individuals (HNWIs): protecting assets, optimizing taxes, and gaining access to global investments. At its heart lies jurisdictional arbitrage – strategically placing assets in countries with legal systems that offer stronger protections than their home countries. When done right, offshore accounts can turn what might otherwise be a straightforward asset seizure into a drawn-out, expensive cross-border legal battle. This makes it harder for creditors to seize assets while staying fully compliant with regulations. These benefits are what make offshore banking so appealing, starting with its robust asset protection features.

Asset Protection and Privacy

Offshore banking creates a legal shield around assets, making them harder to reach for creditors. For example, jurisdictions like the Cook Islands and Nevis don’t recognize foreign court rulings. This forces creditors to re-litigate their cases locally, under local laws, and meet the "beyond a reasonable doubt" standard – something rarely achieved in civil cases.

Nevis adds another hurdle by requiring creditors to post a $25,000 bond before filing a case, while the Cook Islands ups the ante with a $50,000 bond requirement. These measures also extend to domestic assets. For example, HNWIs can use offshore entities to register mortgages or liens on their real estate, effectively stripping the equity and making the property less appealing to creditors.

Modern offshore structures add even more layers of protection through tools like spendthrift provisions, which block beneficiaries from handing over trust assets to creditors, and flight clauses, which allow trusts to relocate automatically if the jurisdiction becomes politically or legally unstable. These features work together to create a web of legal complexities that discourage claims, all while fitting neatly into the broader strategy of jurisdictional arbitrage.

Tax Optimization and Diversification

Offshore banking isn’t just about protecting assets – it also offers substantial tax advantages. One key benefit is tax deferral, which allows earnings to grow tax-free within offshore entities until they are distributed. This isn’t tax evasion; it’s a legal form of tax planning.

For U.S. citizens living abroad, the Foreign Earned Income Exclusion (FEIE) provides even more opportunities. For instance, a single person earning $300,000 might face an effective tax rate of 39.1% in the U.S., but this could drop to 20.5% when leveraging the FEIE. Married couples could see their rate fall to as low as 10.8%.

Jurisdictions like the Cayman Islands and the British Virgin Islands are considered tax-neutral, which means they help prevent double taxation for global investment groups. This makes them an essential part of international ventures where capital is pooled from multiple sources. Offshore banking also allows for currency diversification, letting HNWIs hold assets in currencies like USD, EUR, GBP, SGD, and CHF. This helps protect against inflation and domestic currency fluctuations. With the U.S. national debt projected to hit $38 trillion by 2026, some are moving assets to countries like Switzerland, where public debt is a far smaller percentage of GDP – around 30–40%.

Access to Global Investment Opportunities

Certain high-value investment opportunities are off-limits to residents of specific countries. For instance, private equity funds, venture capital networks, and emerging market portfolios may restrict direct investment from U.S. or UK residents. Offshore corporate entities, however, can provide a legitimate way to access these markets.

Singapore has become a major hub for accessing Asian investments, while Swiss banks are known for facilitating entry into European private placements. These opportunities represent distinct asset classes, each with unique regulatory landscapes, highlighting the importance of offshore structures in 2026.

Offshore accounts also act as a safeguard against economic or political risks. They can protect against capital controls, bank failures, or even domestic political instability.

"If you have all your assets in one country and one day you wake up and your cards do not work… it is too late" – Craig Whyte.

This access to global markets complements the other advantages of offshore banking – asset protection and tax planning – creating a well-rounded strategy for wealth management. It’s no surprise that over 60% of individuals in the top 0.01% maintain offshore accounts. However, these strategies work best when implemented proactively, during stable times. Last-minute transfers can often be undone as fraudulent conveyances.

sbb-itb-39d39a6

Best Offshore Jurisdictions for HNWIs

Top Offshore Banking Jurisdictions for High-Net-Worth Individuals in 2026

Offshore jurisdictions offer tailored advantages depending on your financial objectives. Whether you’re aiming to preserve wealth for future generations, explore Asian investment opportunities, or operate in a tax-free environment, the right jurisdiction can make all the difference. Below are some of the most notable destinations, each catering to different wealth management needs.

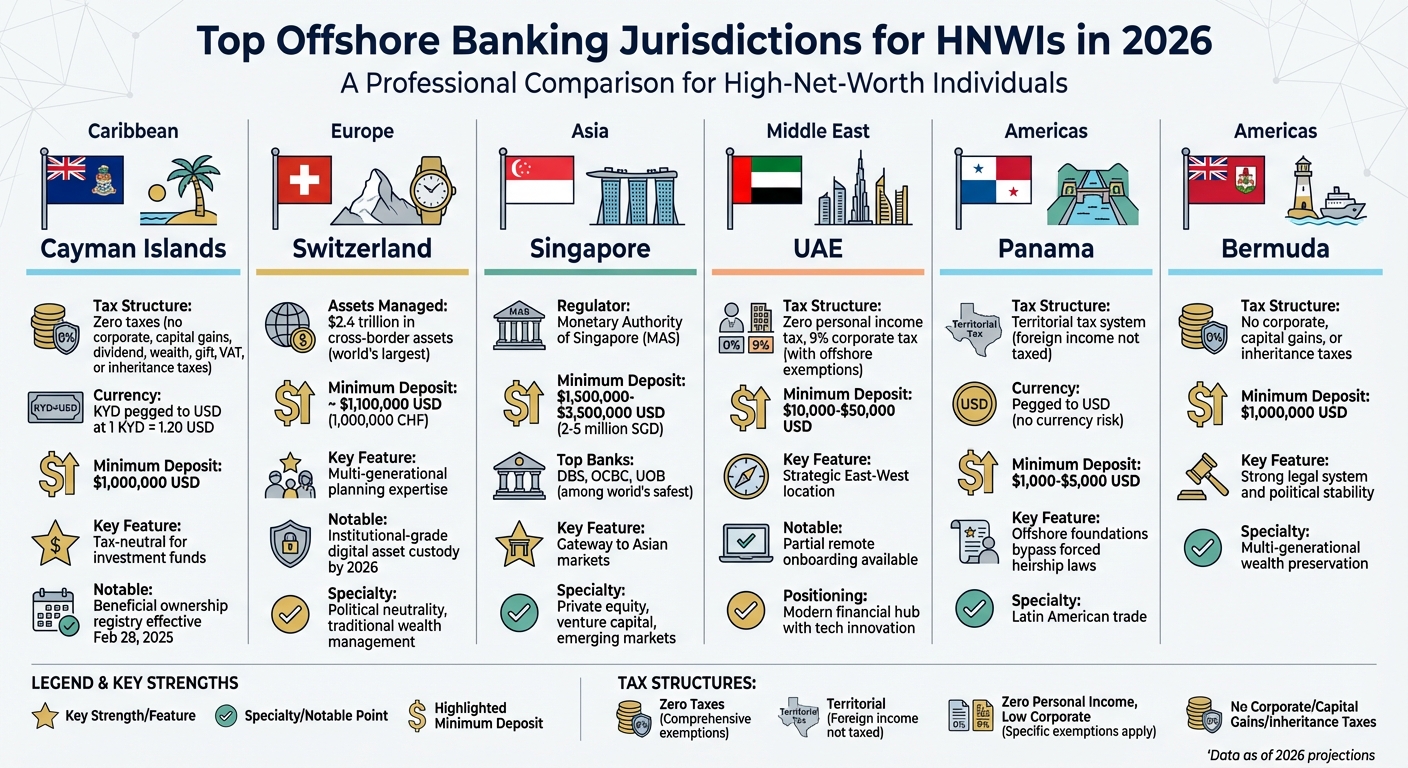

Cayman Islands and Bermuda

The Cayman Islands is renowned for its complete absence of taxes – no corporate, withholding, capital gains, dividend, wealth, gift, VAT, or inheritance taxes exist here. This makes it a go-to choice for investment funds and international business ventures, especially where avoiding double taxation is a priority. Additionally, the Cayman Islands dollar (KYD) is pegged to the US Dollar at a steady rate of 1 KYD = 1.20 USD, ensuring currency stability.

Both the Cayman Islands and Bermuda offer strong legal systems and political stability, key factors for safeguarding wealth through an asset protection private family office. However, opening a banking relationship as a non-resident typically requires a minimum deposit of $1 million. It’s worth noting that the Cayman Islands has introduced a beneficial ownership registry, effective February 28, 2025, which slightly alters its historical privacy protections.

Switzerland and Singapore

Switzerland has long been the gold standard in private wealth management, managing approximately $2.4 trillion in cross-border assets – more than any other offshore center in the world. Swiss banks are celebrated for their expertise in multi-generational planning and political neutrality. By 2026, they’ll also offer institutional-grade digital asset custody, allowing clients to integrate cryptocurrency into traditional portfolios.

"Switzerland remains the world’s largest offshore wealth management centre, managing approximately 2.4 trillion USD in cross-border assets." – HPT Group

Singapore, on the other hand, has gained a reputation for regulatory excellence under the Monetary Authority of Singapore (MAS). Its leading banks – DBS, OCBC, and UOB – are consistently ranked among the safest globally. Singapore is also an ideal gateway to Asian markets, offering access to private equity, venture capital, and emerging market investments. Private banking in Singapore typically requires minimum deposits of 2–5 million SGD (around $1.5–3.5 million USD), while Swiss banks often have a starting threshold of 1 million CHF.

UAE and Panama

The UAE has positioned itself as a modern financial hub with zero personal income tax and a strategic location connecting East and West. While a 9% corporate tax was introduced in 2023, offshore entities can still benefit from tax exemptions. Entry points are relatively accessible, with minimum deposits ranging from $10,000 to $50,000 USD, and partial remote onboarding is available, making it more convenient than many traditional banking centers.

"The UAE represents banking’s future: where traditional financial services merge seamlessly with technological innovation." – Project Black Ledger

Panama operates under a territorial tax system, meaning income earned outside its borders is not subject to local taxation. Its economy, pegged to the US Dollar, eliminates currency risk for American clients. With minimum deposits as low as $1,000 to $5,000 USD, Panama is particularly appealing for those engaged in Latin American trade or seeking to establish offshore foundations that bypass forced heirship laws common in civil law jurisdictions.

Offshore Banking Tools and Account Types

Offshore banking tools can help safeguard wealth, manage taxes effectively, and ensure financial flexibility across borders. These tools work alongside asset protection and tax strategies to create a well-rounded approach to managing offshore wealth.

Priority Banking Portfolios

Private banking services go beyond standard accounts, offering tailored wealth management solutions, specialized lending options, and access to exclusive investment opportunities. Typically, these accounts require minimum deposits ranging from $1,000,000 to $5,000,000. However, priority banking tiers are available with deposits as low as $250,000 to $500,000.

One notable feature of these services is access to Securities-Backed Lines of Credit (SBLOCs). These allow clients to borrow 50%–70% of their portfolio’s value without selling off assets.

In Singapore, institutions like DBS, OCBC, and UOB set private banking thresholds between 2,000,000 and 5,000,000 SGD (around $1,500,000 to $3,500,000 USD). This access to global investment options enhances diversification, a key principle of offshore wealth management.

Offshore Trusts and Portfolio Bonds

Offshore Asset Protection Trusts (APTs) are designed to shield assets from creditor claims. By transferring assets to a trustee in jurisdictions such as the Cook Islands or Nevis, you separate legal ownership, making it significantly harder for creditors to access your wealth.

Jurisdictions like Nevis and the Cook Islands offer unique protective measures, including creditor bond requirements and statutes of limitations, which add extra layers of security. Setting up an offshore trust typically costs between $8,000 and $30,000, with annual maintenance fees ranging from $3,000 to $15,000. High-net-worth individuals often create layered structures where an offshore trust owns an International Business Company (IBC) or LLC, which then holds various assets like bank accounts and real estate.

Private Placement Life Insurance (PPLI), also known as portfolio bonds, wraps investment assets within an insurance policy. This structure provides tax-deferred growth, creditor protection under insurance law, and, in some cases, tax-free distributions to beneficiaries. These policies are generally suited for portfolios requiring $1,000,000 or more in premiums, aligning with earlier tax optimization strategies.

Multi-Jurisdiction Bank Accounts

Multi-jurisdiction accounts take diversification a step further by spreading assets across borders. This distribution reduces risks tied to institutional failures, frozen accounts, or government intervention. For example, FDIC insurance in the U.S. only covers up to $250,000 per depositor, per bank, leaving larger amounts vulnerable. Similarly, during the 2013 Cyprus banking crisis, deposits exceeding €100,000 faced losses of 40% to 60% due to a government-enforced bail-in.

To mitigate such risks, high-net-worth families often maintain five to eight separate banking relationships. For portfolios valued between $5,000,000 and $10,000,000, a common strategy is to allocate about half to domestic banks, a quarter to offshore trusts, and the remainder across other assets and jurisdictions. This approach balances security and accessibility.

A multi-bank strategy often combines traditional banks for asset custody with digital platforms for quicker international transactions. However, timing is critical – asset protection structures must be established well before any legal challenges arise. Transferring assets after a lawsuit has been filed can be deemed a "fraudulent conveyance", potentially invalidating the protection. Taking proactive steps ensures these structures remain effective, reinforcing earlier principles of asset protection.

Legal Requirements and Compliance

Offshore banking is governed by intricate international regulations. Navigating these rules is crucial to ensure compliance while safeguarding your assets.

FATCA, CRS, and Reporting Obligations

The Foreign Account Tax Compliance Act (FATCA) compels foreign financial institutions to disclose U.S. account holders to the IRS. Non-compliance can result in a 30% withholding tax on U.S.-source income, making it nearly impossible for U.S. citizens to conceal offshore accounts.

The Common Reporting Standard (CRS) broadens this transparency to 116 jurisdictions as of 2026. Financial institutions now automatically report account information – balances, interest, and dividends – of non-residents to their home tax authorities annually. This system tracks about 171 million accounts holding nearly €13 trillion in assets. Since 2009, these global compliance efforts have recovered over €135 billion in taxes, interest, and penalties.

Starting January 1, 2026, CRS 2.0 addresses previous gaps by including digital wallets, electronic money accounts exceeding $10,000, Central Bank Digital Currencies, and crypto assets under the Crypto-Asset Reporting Framework (CARF). The first data exchanges are set for 2027.

U.S. persons must also comply with domestic reporting requirements. This includes filing FinCEN Form 114 (FBAR) if their total foreign accounts exceed $10,000 in a year, and IRS Form 8938 for specified foreign financial assets. Non-compliance can trigger audits as tax authorities cross-reference offshore holdings with domestic tax returns through automated data exchanges.

"True privacy in 2026 is not about hiding from the government. It is about protection from everyone else." – Ipanema Partners

These rigorous reporting standards underscore the importance of a well-planned multi-jurisdiction network.

Building a Multi-Jurisdiction Network

To effectively navigate these regulations, establishing a multi-jurisdiction network is essential. A Tax Residency Certificate (TRC) ensures CRS data is sent to the correct tax authority, avoiding errors like reporting to high-tax jurisdictions due to outdated addresses.

Entity classification is another key consideration. Under CRS and FATCA, distinguishing between "Financial Institutions" and "Non-Financial Entities" (NFEs) is critical. Passive NFEs – those earning over 50% of their income from passive sources like dividends – require banks to report their Ultimate Beneficial Owners. By contrast, structuring entities as "Active NFEs" engaged in genuine trade or services shifts the reporting focus to the entity itself, not individual shareholders.

Economic Substance Regulations add another layer of compliance. Jurisdictions like the British Virgin Islands and Cayman Islands require offshore entities to demonstrate a physical presence, local staffing, and income-generating activities. Non-compliance can result in fines ranging from CI$10,000 to CI$100,000, along with mandatory data sharing with tax authorities.

Interestingly, the U.S. does not participate in CRS and rarely reciprocates FATCA data. This makes states like South Dakota, Nevada, and Delaware attractive for financial privacy – though this advantage is limited to non-U.S. citizens.

How Offshore Companies and Trusts Work

Offshore companies and trusts complement a multi-jurisdiction network by providing legal separation, enhancing asset protection, and meeting reporting requirements. Establishing an International Business Company (IBC) typically costs between $2,000 and $5,000, with annual maintenance fees ranging from $1,000 to $3,000.

For CRS and FATCA purposes, the residency of a trust is determined by where its trustees are located, not where its governing law is established. This allows for strategic placement of trustees in jurisdictions with favorable reporting frameworks while retaining asset protection.

Layered structures offer additional benefits. For instance, an offshore trust might own an IBC or LLC, which then holds bank accounts and other assets. However, these structures must be set up before any legal disputes arise to remain effective.

"With each step – financial institution, local authority, foreign authority – comes a risk of a data breach." – Luxembourg-based tax advisers

For U.S. persons, full disclosure is the safest route. Offshore structures can provide legitimate benefits like asset protection and diversification, but attempting to hide assets from tax authorities can lead to severe penalties. The goal is to use these tools to protect against creditors, lawsuits, and institutional risks – not to evade taxes.

Risks and Considerations for 2026

Offshore banking in 2026 comes with its fair share of challenges, many of which require careful navigation to avoid potential pitfalls. One of the most pressing concerns is the increasing scope of regulations. With the implementation of CRS 2.0 on January 1, 2026, reporting requirements now extend to digital wallets, electronic money accounts holding over $10,000, and Central Bank Digital Currencies. Additionally, the Crypto-Asset Reporting Framework (CARF) has introduced mandatory reporting for crypto holdings. Seventy-five jurisdictions have already committed to this framework, with the first data exchanges slated for 2027. In parallel, European exchanges will begin transaction-level crypto reporting under DAC8 in the same year.

Political and economic instability in certain regions also adds to the complexity of offshore banking. For example, jurisdictions on the FATF greylist – such as Monaco, Vietnam, and Bulgaria – face significant operational hurdles. These include delays in wire transfers and frequent rejections by correspondent banks, even though they may offer theoretical privacy benefits. To mitigate these risks, it’s wise to diversify assets across more stable locations like Singapore, Switzerland, and the UAE, which are less prone to capital controls or operational disruptions.

Reputational risks are another critical factor to consider. Financial institutions are increasingly applying enhanced due diligence to clients who use Citizenship by Investment (CBI) or Residence by Investment (RBI) programs. Applicants from countries flagged as high risk by the OECD, such as Vanuatu and Dominica, face heightened scrutiny. Adding to this, new OECD rules now classify a home office as a "fixed place of business" if a director spends more than half their working time there. This could expose offshore company profits to taxation in high-tax jurisdictions.

To navigate these risks, proactive planning is key. Establishing trusts and offshore entities before encountering legal or political hurdles is a smart move. Diversifying banking relationships – across private, commercial, and digital banks – can also provide a safety net. Obtaining a Tax Residency Certificate ensures flexibility and helps maintain accurate CRS data reporting.

For U.S. persons, full transparency is essential. While offshore structures can offer legitimate advantages like asset protection and diversification, attempting to hide assets from tax authorities is a risky gamble that can lead to severe penalties. The focus should remain on protecting wealth from threats like creditors, lawsuits, and institutional risks – not on evading taxes.

Conclusion

In this guide, we’ve explored how high-net-worth individuals (HNWIs) use offshore banking to protect and diversify their wealth. By 2026, offshore banking isn’t just a tool for safeguarding assets – it’s a strategic approach to wealth management. The wealthiest individuals understand that placing assets in top global jurisdictions creates a legal shield against risks like creditors, lawsuits, and geopolitical instability. It’s no surprise that over 60% of the top 0.01% hold foreign accounts, making this a key pillar of modern wealth protection.

When it comes to asset protection and tax planning, proactive strategies are essential. As James G. Bohm, Partner at Bohm Wildish & Matsen, LLP, puts it:

"Offshore asset protection is still viable, but it’s no longer a ‘hidden vault.’ Today, it’s most effective as part of a transparent, legally compliant, and professionally structured estate and asset plan."

Setting up these structures during stable times is critical. Modern offshore strategies often involve a mix of offshore trusts and foundations, operating companies, and diversified banking relationships. This combination ensures strong asset protection, liquidity, and compliance with FATCA and CRS reporting requirements, while also opening doors to global investment opportunities.

As regulations continue to evolve, staying ahead means regularly updating your approach. Working with seasoned professionals who understand the nuances of offshore banking is crucial. Firms like Global Wealth Protection specialize in helping HNWIs navigate these complexities. Their services include offshore company formation, asset protection trusts, and tailored consultations to safeguard and grow wealth across jurisdictions.

Whether your goal is to shield assets from litigation, reduce exposure to domestic risks, or optimize your tax strategy, offshore banking can offer the security and flexibility your wealth needs. The time to act is now. Secure your financial future with a strategy that works for you.

FAQs

Is offshore banking legal for U.S. citizens?

Yes, U.S. citizens can legally open offshore bank accounts, provided they follow the law and maintain transparency. This includes accurately reporting the accounts to the IRS and adhering to all relevant tax and financial regulations. Offshore accounts can provide advantages like enhanced privacy and asset protection, but it’s crucial to use them responsibly and stay compliant with legal requirements.

What do I have to report to the IRS if I open an offshore account?

U.S. taxpayers are required to report all income earned worldwide, including income from foreign accounts. This means filing Schedule B with your tax return and, if your foreign assets surpass specific thresholds, completing Form 8938 as well.

Additionally, if the total value of all foreign accounts exceeds $10,000 at any time during the year, you must also file FinCEN Form 114 (FBAR). Failing to meet these requirements can result in significant penalties, so it’s important to stay compliant.

How much money do I need to start offshore banking?

The amount you need to deposit to open an offshore bank account can differ widely depending on the bank and its location. Some institutions may ask for a minimum deposit of just $1,000, while others might require $62,000 or more. These thresholds are set based on the bank’s policies and the jurisdiction in which it operates, so it’s crucial to explore options that fit your financial objectives.