When it comes to safeguarding wealth while minimizing taxes, a few countries stand out for their combination of low-tax policies, strong legal protections, and political stability. This article highlights Singapore, Cayman Islands, United Arab Emirates (UAE), St. Kitts and Nevis, and Liechtenstein, each offering unique benefits for asset protection and tax efficiency.

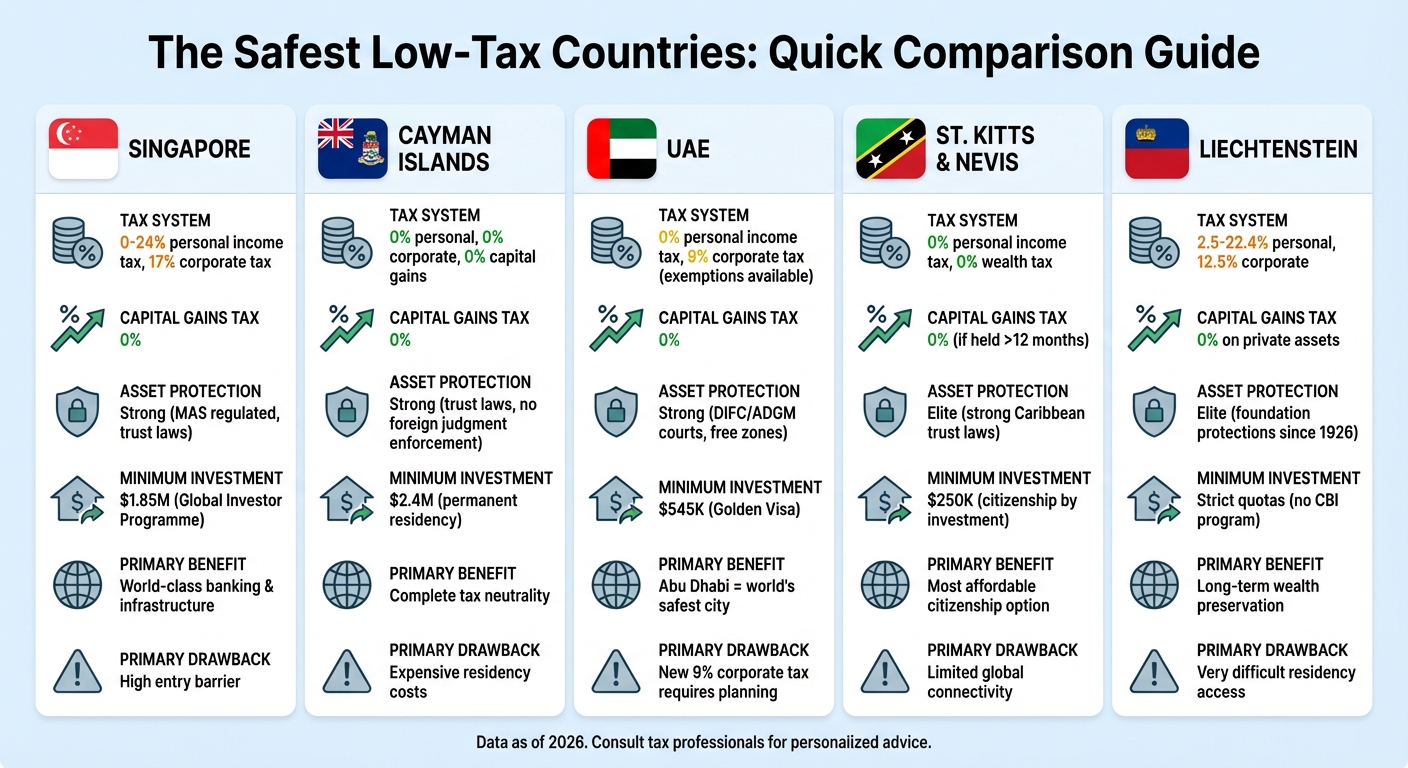

- Singapore: Territorial tax system, no capital gains tax, and strong banking confidentiality. Residency requires a minimum investment of $1.85 million.

- Cayman Islands: Zero personal and corporate taxes, robust trust laws, but high residency costs starting at $2.4 million.

- UAE: No personal income tax, 9% corporate tax (with exemptions), and safe residency options starting at $545,000.

- St. Kitts and Nevis: No personal income or wealth taxes, strong asset protection laws, and citizenship-by-investment starting at $250,000.

- Liechtenstein: Low corporate tax (12.5%), world-class foundation structures for wealth protection, but strict residency quotas.

Each jurisdiction caters to different financial goals, whether you prioritize tax savings, secure asset management, or accessible residency options. Below is a quick comparison to help you decide.

Quick Comparison

| Country | Tax System | Asset Protection | Residency Cost/Access | Primary Drawback |

|---|---|---|---|---|

| Singapore | Moderate (0–24% personal) | Strong (trust laws) | High ($1.85M investment) | High entry barrier |

| Cayman Islands | Zero personal/corporate tax | Strong (trust laws) | High ($2.4M investment) | Expensive residency |

| UAE | Zero personal income tax | Strong (free zones) | Moderate ($545K investment) | New corporate tax (9%) |

| St. Kitts & Nevis | Zero personal/wealth tax | Elite (trust laws) | Affordable ($250K donation) | Limited global connectivity |

| Liechtenstein | Low (12.5% corporate) | Elite (foundations) | Strict quotas | Difficult residency access |

Whether you’re seeking tax neutrality, long-term asset protection, or a secure residency option, these countries offer tailored solutions. Read on for detailed insights into their tax policies, legal frameworks, and residency programs.

Comparison of Top 5 Low-Tax Countries for Asset Protection and Residency

1. Singapore

Tax Policies

Singapore operates under a territorial tax system, meaning foreign-sourced income is exempt from taxation unless it is brought into the country. Additionally, there is no capital gains tax on non-trade-related profits. The country also refrains from imposing gift taxes, estate duties, inheritance taxes, or net wealth taxes.

The corporate tax rate is set at a flat 17%, but startups can benefit from incentives that lower their effective tax rates. For instance, new companies receive a 75% exemption on the first S$100,000 of chargeable income for the first three years. For individuals, the top marginal personal income tax rate is 24%, applicable to income exceeding S$1 million. Singapore has also established over 80 double taxation agreements to reduce withholding taxes on cross-border transactions, making it an attractive jurisdiction for international business.

These tax policies are further enhanced by Singapore’s strong legal framework and asset protection measures.

Asset Protection Strength

Singapore’s legal system, based on English Common Law, provides solid asset protection mechanisms. The Trustees Act 1967, particularly Section 90, safeguards trusts from foreign forced heirship laws as long as the trust is governed by Singapore law and managed by local trustees. Foreign judgments are not automatically enforceable in Singapore; they must go through a local judicial review process.

Banking confidentiality is another notable feature. Section 47 of the Banking Act strictly limits banks from disclosing client information unless required for criminal investigations or international tax compliance. The Monetary Authority of Singapore ensures that banks adhere to stringent capital and liquidity requirements, earning the banking system a perfect 10/10 rating for quality and global integration. Setting up a professional trust typically costs between US$10,000 and US$18,000, while tax planning services range from US$6,000 to US$12,000.

Political and Economic Stability

Singapore’s political and economic stability underpins its reputation as a secure and efficient jurisdiction. As a high-income economy with world-class infrastructure and a business-friendly regulatory system, its environment is ideal for global enterprises. In 2023, the economy grew by 1.1%, demonstrating resilience despite global economic challenges. Black Ledger aptly described Singapore as:

Singapore is more than just a financial hub – it’s a precision-engineered jurisdiction for serious global operators.

Its prime location further strengthens its appeal, serving as a gateway to rapidly growing Asian markets and drawing businesses looking to expand in the region.

Residency/Citizenship Options

Singapore offers several pathways for residency and citizenship. The Global Investor Programme (GIP) requires a minimum investment of S$2.5 million (around US$1.86 million) to qualify for residency. To be considered a tax resident, individuals must live or work in Singapore for at least 183 days within a calendar year. The Overseas Networks & Expertise (ONE) Pass is another option aimed at attracting high-net-worth individuals and top talent.

Business registration fees are low, costing approximately US$300. However, naturalization requires renouncing previous citizenship. Foreigners purchasing residential property face a 60% Additional Buyer’s Stamp Duty (ABSD), though exemptions may apply under certain Free Trade Agreements with countries like the United States and Switzerland.

sbb-itb-39d39a6

2. Cayman Islands

Tax Policies

The Cayman Islands is well-known for its zero-tax system. It imposes no personal income tax, corporate tax, capital gains tax, wealth tax, inheritance tax, or estate duties. Non-residents also benefit from no withholding taxes on dividends, interest, or royalties. This tax-free environment aligns with the jurisdiction’s focus on minimizing tax burdens while ensuring strong asset security.

Businesses like exempted companies, limited liability companies, and unit trusts can even secure government guarantees that ensure they remain tax-free for 20 to 50 years, even if future tax laws change. Instead of direct taxes, the government relies on indirect taxes, such as stamp duties and import duties. For example, real estate transfers are subject to a 7.5% stamp duty, which will increase to 10% for properties worth $2 million or more starting January 1, 2026. Import duties are generally set at 22%.

The Cayman Islands also complies with global standards, including the US Foreign Account Tax Compliance Act (FATCA), the Common Reporting Standard (CRS), and economic substance regulations for specific entities. As of early 2024, the Cayman Islands Monetary Authority (CIMA) oversees more than 12,800 open-ended mutual funds and over 16,700 closed-ended funds.

Asset Protection Strength

Built on English common law, the Cayman Islands’ legal framework is familiar and reliable for international businesses. The Trusts Act (Part VII) protects Cayman trusts from foreign forced heirship claims, and local courts do not enforce foreign judgments that violate these provisions. Additionally, under the Fraudulent Dispositions Act, creditors must prove a transfer was made with the intent to defraud and at undervalue to challenge property dispositions.

The STAR trust regime offers flexibility, allowing trusts to be created for specific purposes or beneficiaries. This is particularly useful for both private wealth and commercial structures [15, 19]. Foundation Companies, introduced in 2017, blend the features of companies and civil law foundations, providing a unique structure for wealth management and succession planning.

The Cayman Islands is also a hub for global finance, with over 40 of the world’s top 50 banks operating there. Its stock exchange boasts a market capitalization exceeding $850 billion. Establishing a trust in the Cayman Islands is relatively affordable, with a stamp duty of CI$40 [14, 15].

Political and Economic Stability

As a British Overseas Territory, the Cayman Islands benefits from the UK’s oversight of internal security, defense, and foreign affairs, contributing to its overall stability. The Privy Council in London serves as the final court of appeal, offering international investors confidence in the legal system [15, 20]. The territory also holds an Aa3 sovereign risk rating.

The local economy is driven by financial services and luxury tourism, which together account for 50–60% of GDP [18, 21]. In 2023, the nominal GDP per capita was around $109,684, and the unemployment rate was a low 2.1% in 2022. The Cayman Islands dollar (KYD) is pegged to the US dollar at a fixed rate of 1 KYD = 1.20 USD, reducing currency risk.

As the world’s fifth-largest banking center, the Cayman Islands is home to over 100,000 registered companies – outnumbering its human population. CIMA plays a key role in maintaining regulatory oversight, with its mission being:

"To protect and enhance the integrity of the financial services industry of the Cayman Islands".

Residency/Citizenship Options

The Cayman Islands provides several residency options for those interested in living or working there. A 25-year residency certificate requires an investment of at least $1.2 million, with at least $600,000 allocated to developed real estate, along with proof of an annual income of $146,000 [17, 20]. Permanent residency, which can lead to British Overseas Territories Citizenship (BOTC), demands a real estate investment of at least $2.4 million and a one-time fee of approximately $122,000 [17, 20].

For remote workers, the Global Citizen Concierge program is available. Applicants must demonstrate an annual income of at least $100,000 and pay an annual fee of $1,500, which covers one dependent. Another option, the Substantial Business Presence pathway, requires either a 10% shareholding in an approved business or a senior management role, with an issuance fee of $6,000.

It’s important to note that US citizens residing in the Cayman Islands remain subject to IRS obligations, so specialized tax planning is strongly recommended.

These residency programs complement the Cayman Islands’ strong asset protection and thriving financial sector, making it an attractive destination for investors and professionals alike.

3. United Arab Emirates

Tax Policies

The UAE is notable for its zero personal income tax policy. This means individuals don’t pay taxes on salaries, investment returns, dividends, or capital gains. For businesses, a 9% federal corporate tax applies only to profits exceeding AED 375,000 (around $102,000), while profits below this threshold are taxed at 0%. Additionally, there are no wealth, inheritance, gift, or estate taxes, making the UAE particularly attractive for multi-generational wealth planning.

Businesses in designated Free Zones enjoy further benefits, such as 0% corporate tax for periods ranging from 15 to 50 years, alongside exemptions from VAT and customs duties. The standard VAT rate is set at 5%, and the UAE has over 138 double taxation treaties to support efficient international investments. The UAE Dirham, pegged to the US dollar, ensures currency stability, which is particularly appealing to American investors.

To fully utilize these tax benefits and avoid double taxation in their home countries, residents need a Tax Residency Certificate. This requires living in the UAE for at least 180 days, along with securing a long-term lease or property. The application fee is AED 1,000 for individuals and AED 1,750 for businesses. These tax policies are complemented by a robust framework for protecting assets.

Asset Protection Strength

The UAE’s financial free zones, particularly the Dubai International Financial Centre (DIFC) and Abu Dhabi Global Market (ADGM), provide a strong asset protection system rooted in English Common Law. These zones have independent courts and allow investors to set up foundations – legal entities that separate personal wealth from business liabilities and creditor claims.

Foundations include firewall provisions that shield assets from foreign forced heirship laws and conflicting judgments, ensuring protection from inheritance disputes. The DIFC alone manages over $700 billion in assets, supporting families with a combined wealth of approximately $1.2 trillion.

Non-Muslim expatriates can register wills with the DIFC Wills and Probate Registry (fee: AED 10,000) to dictate asset distribution and bypass default Sharia inheritance laws. The popularity of foundations has surged, with annual registrations growing from 128 to around 700 between 2020 and 2025, reflecting growing trust in these legal structures. These systems not only secure assets but also contribute to the UAE’s reputation as a stable and attractive investment destination.

Political and Economic Stability

The UAE is regarded as one of the most politically stable and secure nations in the Middle East, which enhances its reputation as a safe investment hub. In 2025, the country attracted 9,800 new millionaires, marking the highest net inflow globally and signaling strong confidence among high-net-worth individuals. The UAE’s removal from the FATF "grey list" in February 2024 further highlights its improved anti-money laundering and counter-terrorism measures.

"The UAE is considered to be one of the most politically stable and secure countries in the region and consequently is regarded as a safe haven for investment." – Association of Corporate Counsel (ACC)

Beyond political stability, the UAE’s diversified economy – anchored by financial services, real estate, and tourism – adds to its appeal for international investors.

Residency/Citizenship Options

The UAE offers a variety of residency options tailored to investors, professionals, and retirees:

- A 10-year Golden Visa requires a minimum AED 2 million investment (around $545,000) in real estate or investment funds.

- A 3-year Property Investor Visa starts at AED 750,000 (around $204,000).

- A 5-year Green Visa is available for skilled professionals earning at least AED 360,000 (around $98,000) annually.

Golden Visa holders can stay outside the UAE for extended periods without losing their residency and can sponsor family members and domestic staff. For remote workers, the Virtual Work Visa requires a minimum monthly salary of $3,500 from a foreign employer. Retirees aged 55 and older can secure a 5-year visa by showing AED 1 million in savings or property or a monthly income of AED 20,000 (around $5,445).

A 2026 case study by Juriszone highlighted how a high-net-worth individual consolidated $20 million in global assets through a DIFC offshore structure. This approach minimized global tax exposure while maintaining operational flexibility and centralized control of assets across five countries. Additionally, property transfer fees in Dubai are typically 4% of the property value, but transfers to a foundation with the same ultimate beneficial owner may qualify for a reduced rate of 0.125%, subject to Dubai Land Department approval.

4. St. Kitts and Nevis

Tax Policies

Residents and citizens of St. Kitts and Nevis enjoy zero personal income tax on both local and global earnings. This means salaries, investment income, and capital gains on assets held for over 12 months are not taxed. However, assets sold within a year are subject to a 20% capital gains tax. Moreover, the federation imposes no taxes on wealth, gifts, estates, or inheritances, making it easier to transfer wealth across generations.

For businesses, International Business Companies (IBCs) and LLCs registered in Nevis benefit from a 0% corporate tax on income earned abroad. Companies operating locally face a corporate tax rate of 33%, though reports suggest this may drop to 25% for resident companies starting in 2024. The standard Value Added Tax (VAT) is 17%, with a reduced 10% rate available for tourism and hospitality-related businesses. Non-residents are subject to a 15% withholding tax on dividends, interest, and royalties. To qualify as a tax resident, individuals must live in the country for at least 183 days per year. Additionally, the Eastern Caribbean Dollar is pegged to the US Dollar at a fixed exchange rate of 1 USD to 2.70 XCD.

These tax policies are complemented by strong asset protection measures, making the federation a popular choice for international investors.

Asset Protection Strength

Nevis has built a reputation for its strong asset protection laws. Its legal framework is designed to safeguard assets from foreign court judgments, creditor claims, and legal disputes through tools like specialized trusts and foundations. Steven James, an Offshore Structures Researcher, highlights this strength:

"Nevis trusts and foundations provide an additional layer of financial security, protecting assets from legal claims, creditors, and foreign judgments."

These structures are bolstered by strict confidentiality laws that shield the identities and holdings of individuals and businesses. Additionally, the territorial tax system ensures that only income generated within the federation is taxed, allowing for efficient international asset management. For optimal protection, investors often favor Nevis-registered entities over standard structures in St. Kitts.

Political and Economic Stability

St. Kitts and Nevis pairs its appealing tax and asset protection policies with a stable political climate. As a member of the Commonwealth, CARICOM, and other key international organizations, the country operates within a framework of stability and international cooperation. A significant milestone came on March 6, 2026, when the U.S. Department of the Treasury lifted a FinCEN advisory related to the Citizenship by Investment (CBI) program. This decision reflected growing confidence in the country’s due diligence processes.

The government primarily relies on indirect taxes, such as VAT, import duties, and excise taxes, rather than income-based levies. While adhering to international agreements like FATCA and the Common Reporting Standard (CRS), St. Kitts and Nevis continues to uphold strong privacy protections for investors.

Residency/Citizenship Options

Since launching in 1984, St. Kitts and Nevis has operated the world’s oldest Citizenship by Investment (CBI) program. The program requires no physical residency or visits, and its citizenship grants visa-free or visa-on-arrival access to 156 destinations, including the EU Schengen Area, the UK, Hong Kong, and Singapore.

Applicants can choose between different investment options. The Sustainable Island State Contribution (SISC) requires a non-refundable donation of at least $250,000 for a single applicant. Alternatively, real estate investments start at $325,000 for approved developments (reduced from $400,000 as of October 2024) or $600,000 for private single-family homes. Real estate must be held for at least seven years before it can be resold to another CBI applicant. Applications typically take three to six months to process.

Due diligence fees are $10,000 for the main applicant and $7,500 for dependents aged 16 or older. The program excludes applicants with criminal records or those holding citizenship from Afghanistan, Belarus, Iran, Iraq, North Korea, or Russia.

5. Liechtenstein

Tax Policies

Liechtenstein stands out as a jurisdiction that combines low taxes with advanced legal frameworks for wealth management. The corporate income tax is a flat 12.5%, while personal income tax rates, including national and municipal surcharges, range from 2.5% to 22.4%. For 2025, the progressive national tax rate tops out at 8% for incomes over CHF 211,401.

Inheritance and gift taxes were abolished in 2011, but gifts or inheritances exceeding CHF 10,000 must be reported. There’s no capital gains tax on private movable assets like shares and investments. Instead, a notional income of 4% of an individual’s net wealth is added to the taxable base.

Liechtenstein’s Private Asset Structure (PAS) offers a streamlined approach for family wealth management, with entities paying a flat annual tax of CHF 1,800 if they avoid commercial activities. Companies can further reduce their taxable income with a 4% notional interest deduction on modified equity. Tax expert Enrique Guillén highlights:

"Liechtenstein isn’t just about low taxes, it’s about peace of mind."

High-net-worth individuals who don’t work in Liechtenstein can choose lump-sum taxation based on their living expenses rather than global income. This is calculated using a flat 25% tax rate on living costs. The standard VAT rate is set at 8.1% as of 2024.

These tax benefits are complemented by Liechtenstein’s strong asset protection measures.

Asset Protection Strength

Liechtenstein has been a trailblazer in trust law within continental Europe. Assets placed in foundations (Stiftungen) or trusts are legally separated from the personal estates of founders, settlors, or beneficiaries, offering strong protection against creditor claims and foreign judgments. Challenges to asset transfers into these structures can only be made under specific conditions – primarily if the transfer occurred within two years of the individual’s death. The lack of a rule against perpetuities further supports long-term wealth preservation.

Markus Summer and Hasan Inetas from Marxer Attorneys explain:

"With a corporate tax rate of 12.5 per cent and the reduction of the effective tax rate even further through the notional interest deduction, Liechtenstein has joined the league of most tax-efficient jurisdictions by European standards."

The Princely Court of Justice oversees trusts and foundations, ensuring disputes are resolved fairly and beneficiary rights are protected. To retain PAS status, entities must strictly avoid any commercial activities.

Political and Economic Stability

Liechtenstein demonstrates strong fiscal discipline, following a constitutional rule to maintain a balanced budget by aligning expenditure growth with income growth. The country operates with virtually no debt and holds financial assets worth one to three times its operating expenses. Its government wage bill is among the lowest in Europe, at just 5.2% of GDP. As a member of the European Economic Area (EEA) and the European Free Trade Association (EFTA), Liechtenstein enjoys access to the European Single Market without being part of the EU. The use of the Swiss Franc (CHF) adds further monetary stability. Over the past 20 years, the tax-to-GDP ratio has averaged 14.75%, significantly below the Euro area average.

The International Monetary Fund commends Liechtenstein’s approach:

"Liechtenstein maintains a lean government and a strong fiscal position notwithstanding low corporate and personal income tax rates."

In 2024, Liechtenstein implemented OECD Pillar II tax reforms, introducing a 15% minimum tax for large multinational corporations. Its legal framework for trusts and foundations, originally established in 1926, was modernized in 2009 to improve governance and asset protection.

This fiscal and legal stability makes Liechtenstein an attractive destination for high-net-worth individuals.

Residency/Citizenship Options

Liechtenstein maintains strict residency policies and does not offer a citizenship-by-investment program. EEA nationals can apply for residency through a lottery system held twice a year, which allocates half of the permits by chance. Non-EEA citizens must secure permits through direct government approval.

To qualify for tax residency, individuals must either have a permanent home in Liechtenstein or reside there for over 183 days in a tax year. Non-employed foreigners can opt for lump-sum taxation based on living expenses, which appeals to those not actively engaged in business. Before establishing tax residency, transferring assets into irrevocable foundations or trusts can help minimize wealth tax exposure, though distributions may still be taxable. Setting up a foundation or trust involves a one-time tax of 0.2% of the statutory capital, while PAS entities pay a minimum annual tax of CHF 1,800.

Advantages and Disadvantages

This section breaks down the pros and cons of each jurisdiction to help you make an informed choice. Each location comes with its own set of trade-offs in terms of tax benefits, legal protections, and residency options.

The UAE stands out with zero personal income tax and an accessible residency option through its Golden Visa program, which requires a property investment of $545,000. Abu Dhabi’s reputation as the world’s safest city makes it especially appealing for families. However, the introduction of a 9% corporate tax on income exceeding AED 375,000 means businesses need careful planning, such as operating through free zones, to retain tax exemptions.

Singapore is known for its stable banking system and ranks third on the Safe Cities Index. However, its progressive tax system can go up to 24% for top earners by 2026. The Global Investor Program, requiring a minimum investment of SGD 2.5 million (around $1.85 million), creates a high entry barrier. In contrast, St. Kitts and Nevis offers a faster and more affordable route to citizenship starting at $250,000, with no personal income or wealth taxes. Its strong trust laws further bolster asset protection, requiring creditors to post a bond of at least $100,000 before pursuing claims.

The Cayman Islands provides complete tax neutrality, with no personal, corporate, or capital gains taxes. However, residency costs are steep, with permanent residency requiring an investment of $2.4 million. The jurisdiction’s refusal to enforce foreign civil judgments enhances its asset protection appeal. Liechtenstein, on the other hand, is ideal for long-term wealth preservation, thanks to its foundation system under strict judicial oversight. But its strict residency quotas and alignment with Swiss standards make access challenging for investors.

Here’s a quick comparison of the strengths and drawbacks of each jurisdiction:

| Country | Tax Efficiency | Asset Protection | Residency Access | Primary Drawback |

|---|---|---|---|---|

| Singapore | Moderate (0–24% personal; 17% corporate) | Very strong (MAS regulated) | Low (minimum ~$1.85M) | High investment barrier |

| Cayman Islands | Elite (0% all taxes) | Strong (no enforcement of foreign judgments) | Low ($500K–$2.4M) | Expensive residency costs |

| UAE | Elite (0% personal; 9% corporate) | Strong (DIFC/ADGM courts) | High (~$545K) | New corporate tax requires planning |

| St. Kitts & Nevis | High (0% personal/wealth tax) | Elite (strong Caribbean trust laws) | Very high (starting at $250K) | complex IRS reporting requirements |

| Liechtenstein | Moderate (12.5% corporate) | Elite (foundation protections) | Very low (strict quotas) | Difficult residency access |

While zero-tax jurisdictions like the Cayman Islands offer immediate tax relief, they may attract more scrutiny from international compliance organizations compared to established financial hubs like Singapore or the UAE. Currency stability is another consideration – the UAE’s AED is pegged to the US dollar, and Liechtenstein’s access to the Swiss Franc provides added security compared to smaller Caribbean nations.

Conclusion

Choosing the right jurisdiction depends heavily on your specific priorities. If your goal is complete tax neutrality, the Cayman Islands is a strong contender. It offers zero personal, corporate, and capital gains taxes, along with legal protections that block the automatic enforcement of foreign civil judgments. For those seeking excellent infrastructure and global connectivity, both Singapore and the UAE stand out with their low taxes and well-established free zones. The UAE, in particular, is a great choice for families – Abu Dhabi is ranked as the world’s safest city, and its Golden Visa program starts at an investment of about $545,000.

If safeguarding assets is your main concern, St. Kitts and Nevis shines with its strong trust laws and citizenship options starting at just $250,000. For preserving wealth across generations, Liechtenstein’s foundations offer a unique advantage, combining asset segregation with a fixed annual tax of only 1,800 CHF, regardless of the total assets held. However, it’s equally important to weigh these benefits against domestic tax obligations.

For U.S. investors, domestic tax rules remain a critical factor. As Josh Katz, CPA at Universal Tax Professionals, explains:

A tax haven in 2026 is only as effective as the underlying laws; global transparency standards have rendered offshore secrecy largely ineffective.

U.S. citizens are taxed on worldwide income, no matter where they live. In zero-tax jurisdictions, you can only take advantage of the Foreign Earned Income Exclusion – not the Foreign Tax Credit – because no local income tax is paid. On the other hand, Singapore’s territorial tax system might offer more flexibility for U.S. citizens looking to optimize their tax planning.

The global shift from secrecy to substance means that successful offshore strategies now demand real economic activity. This could mean establishing physical residency, running active business operations, or setting up properly structured legal entities. Ultimately, the best jurisdiction for you will depend on whether your focus is immediate tax savings, long-term asset protection, or accessible residency options.

FAQs

Which country is best if I want low taxes without giving up safety?

The United Arab Emirates (UAE) is a top pick for those seeking low taxes and a secure lifestyle. With zero personal income tax, it’s a haven for individuals looking to maximize their earnings. The country also boasts an exceptionally safe environment – Abu Dhabi consistently ranks as one of the safest cities in the world. Add to that its modern infrastructure and long-term residency options, such as the Golden Visa program, and it’s clear why the UAE is so appealing.

While alternatives like Switzerland, Singapore, and the Cayman Islands also offer attractive benefits, the UAE’s mix of tax advantages and safety truly sets it apart.

Do I have to actually live there to get the tax benefits?

Many countries allow you to enjoy their tax benefits without needing to live there full-time. They offer residency or citizenship programs that come with tax perks, often without requiring you to be physically present. These programs are tailored for people looking to streamline their taxes while keeping their lifestyle flexible.

How do U.S. tax rules affect moving to a low-tax country?

The U.S. tax system plays a big role when Americans consider moving to a low-tax country. Why? Because the U.S. taxes its citizens on their worldwide income – no matter where they live. Even if you relocate abroad, you’re still required to file U.S. tax returns and report all global income.

This means that without careful planning, you could face double taxation or run into compliance problems. To navigate this, it’s crucial to seek proper tax planning and legal advice. That way, you can make the most of potential tax benefits while staying on the right side of the law.