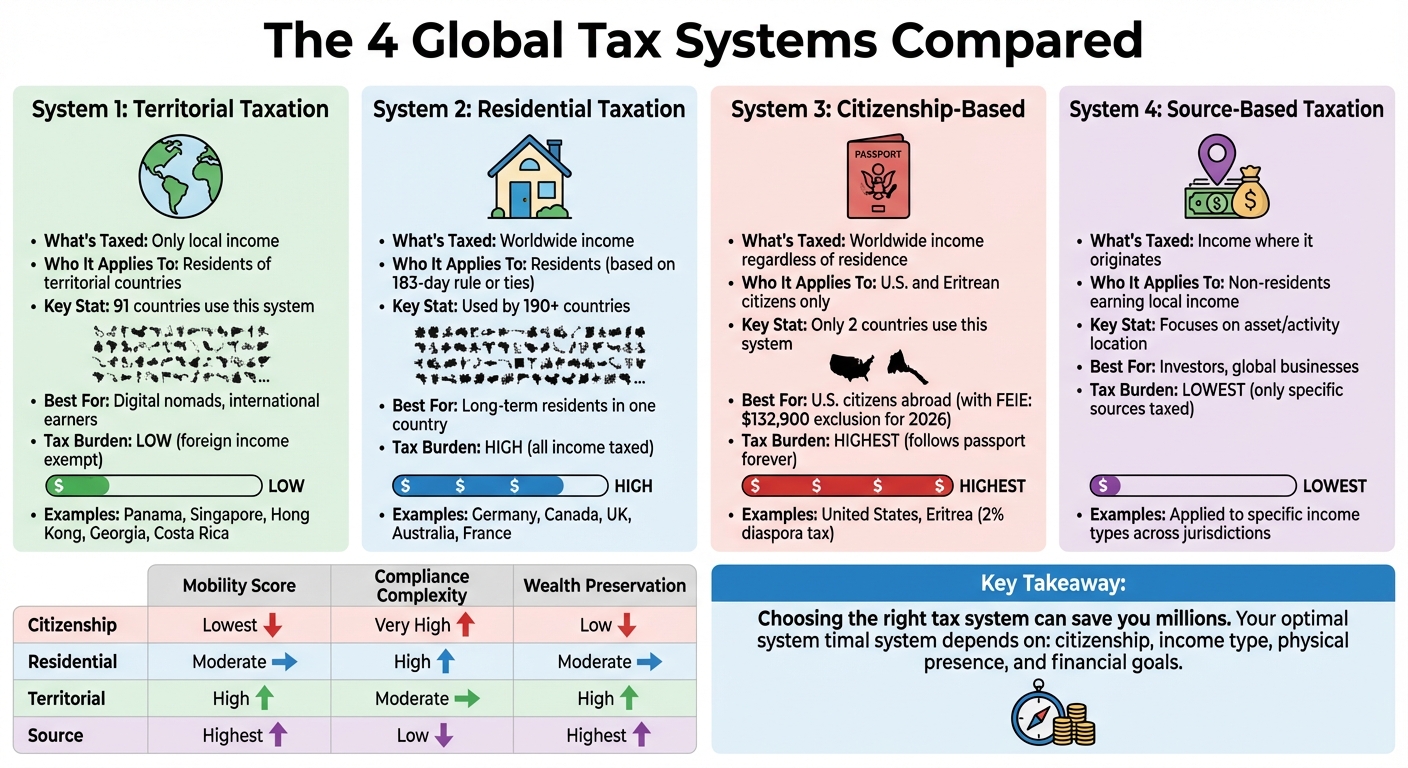

Choosing the right tax system can save you millions. There are four main global tax systems, each with distinct rules and implications for individuals and businesses:

- Territorial Taxation: Taxes only income earned within the country’s borders. Foreign income is exempt.

- Residential Taxation: Taxes worldwide income based on where you live.

- Citizenship-Based Taxation: Taxes worldwide income based on your nationality, regardless of where you live (used by the U.S. and Eritrea).

- Source-Based Taxation: Taxes income where it originates, regardless of your residency or citizenship.

Understanding these systems is critical for minimizing taxes while staying compliant. For example, territorial systems can be ideal for digital nomads or entrepreneurs with international clients, while U.S. citizens face unique challenges under citizenship-based taxation. Your residency, income type, and financial goals determine the best approach.

Quick Comparison

| Tax System | Who It Applies To | What is Taxed | Best For |

|---|---|---|---|

| Territorial | Residents of territorial countries | Only local income | Digital nomads, international earners |

| Residential | Residents of most countries | Worldwide income | Long-term residents in one country |

| Citizenship-Based | U.S. and Eritrean citizens | Worldwide income | U.S. citizens abroad |

| Source-Based | Non-residents earning local income | Income earned in that country | Investors, global businesses |

Comparison of 4 Global Tax Systems: Territorial, Residential, Citizenship-Based, and Source-Based Taxation

Territorial Tax System

A territorial tax system focuses solely on taxing income generated within a country’s borders. Earnings from foreign businesses, overseas clients, or international investments are typically exempt from local taxes. Interestingly, 91 countries currently apply some version of this system.

The concept is straightforward: where the income is earned matters more than where you live. This means you can be a full tax resident in a territorial country and still owe zero tax on income earned abroad. Compare this to worldwide systems, where residents are taxed on all their income regardless of its origin, or the U.S. system, which taxes its citizens globally, even if they live overseas.

For companies, territorial systems often include "participation exemptions", which allow businesses to exclude foreign dividends and profits from domestic taxation. For entrepreneurs and digital nomads, this opens up opportunities for tax planning – especially when paired with tax-transparent entities like a U.S. LLC serving clients outside the resident country.

How Territorial Taxation Works

Under this system, only income sourced domestically is taxed. Foreign-source income – such as profits from overseas businesses, dividends from foreign companies, salaries paid by non-resident entities, or fees from international clients – remains untaxed. For example, if a resident earns $100,000 locally and $200,000 abroad, only the $100,000 earned within the country’s borders would be taxable.

Countries apply territorial taxation differently. Pure territorial systems like those in Panama and Costa Rica exempt all foreign income, even if the funds are brought into the country. Remittance-based systems like those in Singapore and Malta tax foreign income only when it is transferred into local bank accounts. Some countries, like Uruguay, even offer tax holidays, granting new residents up to 11 years of 0% tax on foreign income.

Examples of notable territorial jurisdictions include Panama, Singapore, Hong Kong, Georgia, Paraguay, Costa Rica, and Malaysia. Even the U.S. adopted a "partially territorial" corporate tax system through the 2017 Tax Cuts and Jobs Act, though individuals remain subject to worldwide taxation.

"Territorial taxation is a system that excludes foreign earnings from a country’s domestic tax base." – Tax Foundation

The focus on the origin of income makes territorial taxation a key tool in international tax and asset protection strategies. This often involves structuring offshore trusts to further shield wealth from domestic liabilities.

Benefits and Real-World Applications

Territorial systems provide clear advantages for globally mobile entrepreneurs and investors. The main perk? You don’t pay tax on income earned outside your country of residence. This eliminates the "lockout effect" seen in worldwide systems, where companies hold off on repatriating foreign earnings to avoid domestic taxes.

For multinational businesses, this system enhances global competitiveness. For instance, under a worldwide system, a U.S. company operating in the UK (with a 20% corporate tax rate) would historically owe an additional 15% to the IRS to meet the pre-2017 U.S. corporate tax rate of 35%. In contrast, a French company under a territorial system would only pay the UK’s 20%, creating a clear cost advantage.

Panama, with its pure territorial system, exempts all foreign income – even if the funds are deposited in local banks or spent domestically. This makes it an attractive option for entrepreneurs managing international e-commerce operations, consulting businesses, or investment portfolios.

Singapore takes a slightly different approach. It generally exempts foreign-sourced dividends, branch profits, and service income when specific conditions are met. However, foreign income deposited into local bank accounts may be taxed, making offshore banking a strategic choice for wealth management.

For digital entrepreneurs, a territorial framework offers creative structuring possibilities. Many combine a tax-transparent U.S. LLC with residency in a territorial jurisdiction like Georgia or Paraguay. If the LLC’s income comes from non-local clients and services are delivered outside the resident country, the income may remain tax-free locally. This works because the LLC itself doesn’t pay U.S. taxes (as it’s treated as a pass-through entity), while the territorial country exempts foreign earnings.

Documentation and Compliance

While territorial systems bring significant tax benefits, compliance requires meticulous documentation. Tax authorities demand proof that income qualifies as foreign-sourced.

Key documents include contracts, invoices, and bank statements. Even in cases where no local tax is due, many territorial countries still require annual tax filings. Records should clearly show where services were performed, where clients are located, and how payments were received.

Physical presence matters. In countries like Georgia or Costa Rica, working for a foreign client while physically present in the country may lead tax authorities to classify that income as "locally sourced" and taxable. Keeping a detailed log of days spent in and out of the country can help avoid this issue.

For remittance-based systems, offshore bank statements are crucial. In Singapore, for instance, using a local bank for foreign income could trigger taxation, while keeping funds offshore keeps them tax-free.

Anti-abuse rules also come into play. Many territorial countries enforce Controlled Foreign Corporation (CFC) rules to prevent tax base erosion, which may tax passive income held in offshore entities. Territorial taxation works best for active business income rather than passive investments.

"A territorial tax system basically must balance three competing goals: Exempting foreign business activity from domestic taxation, protecting the domestic tax base, and creating simple rules." – Tax Foundation

For the system to work effectively, it’s crucial to sever tax ties with your previous country of residence. Moving from a worldwide taxation system like that of the U.S. or UK to a territorial jurisdiction requires proper exit procedures to avoid dual taxation.

sbb-itb-39d39a6

Residential Tax System

Residential taxation is a system where your global income is taxed based on where you live. Unlike the territorial system, which taxes only income earned domestically, residential taxation applies to all income sources – whether local or international. If you’re classified as a tax resident in a country using this system, you’ll be taxed on earnings from local jobs, foreign investments, overseas rental properties, or even international consulting work. Countries like Germany, Canada, Japan, the United Kingdom, Australia, and France follow this approach. Your tax liability depends on your residency status, unlike citizenship-based systems, where tax obligations follow you regardless of where you live.

Residency rules, however, differ widely between countries. This can sometimes result in dual residency, where two countries claim the right to tax your worldwide income. Knowing how residency is determined and planning accordingly can help you avoid being taxed twice on the same income.

How Residency Is Determined

Many countries rely on the 183-day rule to establish residency: spending 183 days or more in a country often makes you a tax resident. The United States uses the Substantial Presence Test, which applies a weighted formula: 100% of the days in the current year, one-third of the days from the prior year, and one-sixth from the year before that. If the total reaches 183 days, you’re considered a U.S. resident.

Physical presence isn’t the only factor. Countries also consider ties such as where you live, where your family resides, and where your economic interests are centered. For example, Canada and France emphasize these connections, meaning even shorter stays can lead to tax residency.

Some countries have unique rules. In Switzerland, residency can be triggered after just 30 days if you’re working, or 90 days if you’re not. Germany applies residency rules retroactively – staying more than six consecutive months makes you a resident starting from the first day of that period. In the U.S., holding a Green Card makes you a tax resident regardless of physical presence. Meanwhile, countries like Australia and the UK may assess your "domicile", or intent to remain in the country, as a key factor.

If you meet residency criteria in two countries, tax treaties often provide tie-breaker rules. These typically follow this order: Permanent Home, Center of Vital Interests, Habitual Abode, Nationality, and Mutual Agreement between tax authorities.

| Country | Primary Test | Day Threshold | Other Key Factors |

|---|---|---|---|

| United States | Green Card or Substantial Presence | 183 days (weighted 3-year formula) | Legal immigration status |

| United Kingdom | Statutory Residence Test | 183 days (automatic) | Sufficient ties and home ownership |

| Canada | Factual or Deemed Resident | 183 days | Residential ties (property, family) |

| Australia | Resides Test | 183 days | Domicile and family location |

| Germany | Physical Presence or Abode | 6 months (consecutive) | Retrospective application |

| Switzerland | Registration or Stay Duration | 30 days (working) / 90 days (non-working) | Registered residence status |

| Russia | Physical Presence | 183 days in 12 consecutive months |

Countries Using Residential Taxation

Countries like Germany, Canada, Japan, the United Kingdom, Australia, and France implement residential taxation but apply their own residency criteria.

Germany considers anyone staying over six consecutive months a resident, applying this rule retroactively to the start of the period. The UK’s Statutory Residence Test has several layers: spending 183 days or more in the UK during the tax year (April 6 to April 5) automatically qualifies you as a resident. Alternatively, the Automatic Overseas Test deems you a non-resident if you spend fewer than 16 days (if previously a resident in the last three years) or fewer than 46 days (if not). The UK also uses a "Sufficient Ties Test" for those spending between 16 and 182 days in the country.

Canada examines residential ties beyond day counts. Owning or renting a home, having family in Canada, or maintaining local bank accounts or professional activities can all establish residency. Even partial days spent in Canada count as full days.

France prioritizes family ties through its "home" (foyer) test. If your family resides in France, you may be considered a resident even with frequent travel. Switzerland, on the other hand, offers an option for wealthy non-working foreigners: lump-sum taxation, where taxes are calculated based on living expenses rather than worldwide income.

Understanding these residency rules is essential for planning your tax obligations effectively.

Residency Planning Strategies

Strategic residency planning starts with keeping precise records of your travel. Different countries count days differently – Sweden, for example, considers both arrival and departure days as full days, while others count only the arrival day.

Tax years also vary globally. The U.S. follows the calendar year (January 1–December 31), Australia uses July 1 to June 30, and the UK’s tax year runs from April 6 to April 5. Misunderstanding these timelines could inadvertently trigger residency.

To sever tax residency in a high-tax country, you’ll need to cut local ties, such as selling or leasing your home, relocating your family, and closing accounts. In Australia, for instance, notifying Medicare and the Electoral Commission and canceling private health insurance can help demonstrate your intent to leave permanently.

"Changing your tax residence away from those high-tax jurisdictions… is therefore a critical first step if you want to enjoy a tax-optimized, global lifestyle." – Chris Natterer, Founder, Globalization Guide

Leaving strict jurisdictions like Australia often requires establishing a new, permanent residence in a low-tax country – such as Panama, Paraguay, or Georgia – rather than adopting a nomadic lifestyle. Tax authorities are generally skeptical of individuals claiming no fixed home, which can lead to ongoing residency claims in your former country.

For those spending significant time in multiple countries, managing your "sufficient ties" is crucial. In the UK, for instance, having a property available for 91 consecutive days can trigger residency, even if used sparingly. Leasing out such properties long-term can prevent this issue.

If you qualify as a resident in two countries, consult the relevant tax treaty to apply tie-breaker rules. Tools like Foreign Tax Credits or the Exemption Method can help avoid double taxation. Proper documentation – such as flight records, lease agreements, utility bills, and tax filings – is key to proving your residency status and minimizing tax liabilities.

Citizenship-Based Tax System

Citizenship-based taxation operates differently from most tax systems around the world. Rather than taxing individuals based on where they live or earn income, it’s tied to the passport you hold. The United States is one of only two countries that enforces this system – the other being Eritrea, which applies a 2% diaspora tax. This means that if you’re a U.S. citizen, your global income is subject to U.S. taxes, no matter where you live or where that income comes from.

Unlike residency-based tax systems – where moving abroad typically ends your tax obligations – citizenship-based taxation stays with you. For example, you could live in Singapore for decades, earn all your income there, and never return to the U.S., but you’d still need to file U.S. tax returns annually. This also applies to dual citizens and "Accidental Americans" – individuals born in the U.S. or to U.S. parents who may have never lived in the country.

"The key distinction: Citizenship-based taxation follows your passport. Residency-based taxation follows your physical location."

– Mike Wallace, CEO, Greenback Expat Tax Services

U.S. citizens living abroad face additional reporting requirements beyond the standard tax return. They must file the FBAR (Foreign Bank Account Report) for accounts exceeding $10,000 and FATCA Form 8938 for broader foreign assets. Green Card holders are also subject to these rules until they formally surrender their status using Form I-407.

Unlike the systems used by over 190 other countries, U.S. citizens cannot end their tax obligations without renouncing their citizenship. Understanding this system is crucial for managing tax liabilities and preserving wealth. Let’s dive into what sets this system apart.

What Makes Citizenship Taxation Different

Citizenship-based taxation disregards residency entirely. Most countries tax based on where you live – if you leave places like Germany or Canada and establish residency elsewhere, your tax obligations to those countries typically end. Under the U.S. system, however, your passport dictates your tax liability, not your address. This creates a permanent filing obligation. U.S. citizens abroad face the same tax brackets, deductions, and filing requirements as those living in the U.S.. Even if you owe no taxes due to exclusions or credits, you’re still required to file returns and other reports annually.

In addition to Form 1040, expats must navigate a maze of international reporting forms. For instance, owning 10% or more of a foreign corporation requires Form 5471; investments in foreign mutual funds or ETFs may trigger Form 8621; and receiving large gifts from foreign individuals necessitates Form 3520. These forms are intricate, and errors can result in severe penalties.

"This taxation system means that even if you earn your entire income abroad, hold permanent residency in another country, or haven’t lived in the U.S. for decades, you’re still on the hook for an annual U.S. tax return."

– Katelynn Minott, CPA & CEO, Bright!Tax

The IRS has strengthened its enforcement capabilities. As of 2026, it uses AI-driven data matching to cross-check foreign bank interest with FBAR and FATCA filings in real time. Foreign banks, under FATCA, also routinely request U.S. Tax ID numbers, which often alerts "Accidental Americans" to their filing obligations.

The penalties for non-compliance are steep. In 2024, failing to file an FBAR could cost over $16,000 for an unintentional error, while willful violations could exceed $160,000. The IRS can even notify the State Department about "seriously delinquent tax debt", potentially leading to passport denial or revocation. These measures highlight the importance of staying compliant, even if no taxes are ultimately owed.

Next, we’ll explore the broader framework of the U.S. tax system and how it applies to global income.

The U.S. Tax System Explained

The U.S. taxes three groups of individuals on their worldwide income: citizens (including dual citizens and "Accidental Americans"), Lawful Permanent Residents (Green Card holders), and foreign nationals meeting the Substantial Presence Test. This applies to all income sources – whether it’s wages, investments, rental income, business profits, or cryptocurrency gains.

To avoid double taxation, the U.S. provides several tools. The Foreign Earned Income Exclusion (FEIE) allows qualifying expats to exclude up to $132,900 of foreign earnings from taxable income for 2026. To qualify, you must meet either the Physical Presence Test (spending at least 330 full days in a foreign country within a 12-month period) or the Bona Fide Residence Test, which requires establishing a "tax home" abroad.

The Foreign Tax Credit (FTC) offers a dollar-for-dollar credit for foreign income taxes paid, preventing double taxation on the same income. Unlike the FEIE, the FTC applies to both earned and passive income, such as dividends or capital gains. However, you can’t use both the FEIE and FTC on the same income, so choosing the right strategy is critical.

The Foreign Housing Exclusion or Deduction allows expats to exclude or deduct certain housing expenses exceeding a base amount (16% of the FEIE maximum, roughly $21,264 for 2026). This exclusion is capped at 30% of the FEIE. Self-employed individuals must use the deduction instead of the exclusion.

Tax treaties between the U.S. and other nations can reduce or eliminate U.S. taxes on certain income types and provide "tie-breaker" rules for dual residents. For those qualifying as residents in both countries, treaty provisions may limit U.S. taxation to U.S.-sourced income.

U.S. citizens abroad also benefit from an automatic two-month extension, moving the filing deadline to June 15. However, interest accrues on unpaid taxes from April 15 onward. Additionally, Totalization Agreements with various countries help prevent double taxation on social security or payroll taxes.

Starting January 1, 2026, the One Big Beautiful Bill Act (OBBBA) permanently raised the Estate Tax Exemption to $15 million per individual (or $30 million for couples). Meanwhile, the Child Tax Credit for 2025–2026 is set at $2,200 per child, with a refundable portion of up to $1,700. However, claiming the FEIE disqualifies you from receiving the refundable portion.

Tax Planning for U.S. Citizens Abroad

Navigating this system requires careful planning, especially for expats. One major decision is whether to use the Foreign Earned Income Exclusion or the Foreign Tax Credit. The FTC often works best in high-tax countries like the UK, Germany, or France, where foreign taxes paid can exceed U.S. liability, potentially eliminating your U.S. tax bill and allowing unused credits to carry forward. On the other hand, the FEIE is usually more advantageous in low-tax or no-tax countries like the UAE or Singapore.

Another consideration is the "CTC trap." Using the FEIE disqualifies you from the refundable portion of the Child Tax Credit, potentially costing up to $1,700 per child. In high-tax jurisdictions, opting for the FTC instead of the FEIE may unlock this benefit.

To qualify for the FEIE under the Physical Presence Test, you must spend at least 330 full days in a foreign country within any 12-month period. This timeline doesn’t need to align with the calendar year, so planning your travel dates strategically can make a difference. For the Bona Fide Residence Test, maintaining personal and economic ties outside the U.S. is essential to establish your "abode" abroad.

With these strategies in mind, let’s shift focus to the source-based tax system for additional options.

Source-Based Tax System

Source-based taxation focuses on taxing income in the country where it is generated, rather than where someone lives or holds citizenship. Unlike residential or citizenship-based systems, this approach zeroes in on the income’s origin. For instance, if you earn money in Singapore, Singapore taxes that income. Similarly, income earned in Panama is taxed by Panama.

This system is often called "territorial taxation" when applied broadly. Countries like Hong Kong, Singapore, Panama, Costa Rica, Malaysia, Georgia, and Paraguay follow this model. In these places, income earned outside their borders is typically exempt from local taxes. Even many G7 nations – such as Canada, France, Germany, Italy, Japan, and the UK – use a version of this system, exempting most foreign business income from domestic taxation.

Under international tax principles, the country where the income originates gets the first right to tax it. Meanwhile, the country of residence may offer tax credits to prevent double taxation. For example, the United States has tax treaties with over 60 countries to coordinate rules and reduce withholding taxes on payments like interest, dividends, and royalties. For businesses, profits are taxed where their permanent establishment (e.g., a branch or office) is located. For employees and freelancers, taxes depend on where the work is physically performed.

How Income Source Is Determined

Different types of income are taxed based on specific sourcing rules:

- Salaries and Wages: These are taxed where the services are physically performed. For instance, if a U.S. citizen works in a Paris office for three months, that income is considered foreign-source, even if paid into a U.S. bank account.

- Interest: Taxed based on the residence of the payer or borrower.

- Dividends: Sourced to the country where the paying corporation is incorporated.

- Rents and Real Estate Sales: Taxed in the location of the property.

- Royalties: Linked to where the intellectual property is used.

- Business Profits: Taxed where business activities or the permanent establishment occur.

For remote workers, tracking daily physical locations is essential, as many tax authorities base service income on where the work is performed. Investors should also verify the country of incorporation for their holdings and consult tax treaties when applicable.

| Income Type | Determination of Source |

|---|---|

| Salaries & Wages | Where services are physically performed |

| Interest | Based on the payer’s or borrower’s residence |

| Dividends | Country where the paying corporation is incorporated |

| Rents | Physical location of the property |

| Royalties | Where the intellectual property is used |

| Real Estate Sales | Physical location of the property |

| Business Profits | Where business activities or a permanent establishment occur |

Countries Using Source-Based Taxation

Countries with source-based (territorial) taxation systems do not tax income earned outside their borders. Payments like dividends and interest are often taxed at the source through withholding.

For example, under the Tax Cuts and Jobs Act (TCJA), a U.S. subsidiary in Ireland earning $250 in profit from $1,000 in assets might see the first $100 (a typical 10% return) exempt from U.S. tax under territorial principles. The remaining $150 could be treated as Global Intangible Low Tax Income (GILTI). This shift reflects the U.S. adopting a partially territorial system for corporations after the 2017 TCJA. Over the past three decades, many OECD countries have moved from worldwide to territorial taxation to help domestic businesses compete globally.

Benefits for Different Income Types

Source-based taxation offers clear advantages depending on the type of income:

- Remote Workers: Workers benefit when their compensation is tied to their physical work location. In jurisdictions that exempt foreign-source income, this can mean lower tax liabilities.

- Business Owners: Structuring transactions to recognize income in lower-tax jurisdictions can be advantageous. For example, income from inventory sales is sourced to where the title is transferred, while income from produced inventory is tied to the production location. Setting up a foreign office can also help shift sales to foreign sources, potentially reducing domestic tax burdens.

- Investors: For rental income and real estate gains, taxes depend on the property’s location. Investing in regions with favorable tax rules can reduce liabilities. Similarly, dividends and interest are determined by the payer’s location, allowing for strategic asset placement to minimize withholding rates.

For non-residents in the U.S., there’s a de minimis rule: they can earn up to $3,000 for services performed within the country without that income being considered U.S.-source, provided they stay for fewer than 90 days. This creates opportunities for short-term work assignments without triggering significant tax obligations.

Comparing the 4 Tax Systems

Tax System Comparison Table

Here’s a quick breakdown of how different tax systems handle foreign income, suit mobile lifestyles, and impact compliance and wealth preservation:

| Tax System | Tax Burden (Foreign Income) | Suitability for Mobile Individuals | Compliance Complexity | Wealth Preservation |

|---|---|---|---|---|

| Citizenship-Based | Highest (worldwide income is always taxed) | Lowest (requires formal renunciation to exit) | Very High (annual filing required regardless of location) | Low |

| Residential | High (worldwide income taxed if resident) | Moderate (can exit by moving) | High (tracking days and local ties is necessary) | Moderate |

| Territorial | Low (only income earned locally is taxed) | High (ideal for mobile individuals) | Moderate (focused on reporting local sources) | High |

| Source-Based | Lowest (only specific local sources are taxed) | Very High (tax liability follows the asset/activity) | Low (limited to local asset/activity reporting) | Highest |

The citizenship-based system imposes the greatest administrative burden. For example, the IRS can revoke a citizen’s passport if they owe over $50,000 in unpaid taxes. This system taxes worldwide income regardless of where you live, making it highly restrictive for individuals seeking financial flexibility.

Residential taxation, the most common system globally, is used by over 190 countries. While it offers stability, it requires careful monitoring of physical presence and local ties. For instance, spending too many days in a country or maintaining a permanent home there can trigger tax residency in high-tax jurisdictions.

Territorial systems, on the other hand, provide more freedom for international earners. Many OECD countries, including Australia, Germany, and the UK, apply territorial-style rules for corporate taxation to remain competitive. Under these systems, foreign-sourced income is generally exempt, making them appealing for digital entrepreneurs and investors with income from diverse locations.

What the Comparison Reveals

When it comes to aligning your tax system with financial goals, this comparison highlights a clear trade-off. Citizenship-based taxation offers extensive oversight but places a heavy burden on mobile individuals, particularly those with international income streams.

Territorial and source-based systems, however, stand out for their wealth preservation advantages. By taxing only local income, they allow foreign earnings to remain untouched, which is why many multinational companies keep substantial profits offshore. This approach not only minimizes tax liability but also simplifies compliance.

"The current hybrid U.S. system … embodies the worst features of both a pure worldwide system and a pure territorial system from the perspective of simplicity, enforcement and compliance." – U.S. Treasury Department

The complexity of compliance also varies widely. For instance, only the United States and Eritrea enforce citizenship-based taxation. Eritrea applies a flat 2% "diaspora tax" on its non-resident citizens, a practice that has led to diplomatic tensions, including the expulsion of its diplomats from Canada and the Netherlands in 2013 and 2018 for aggressive collection efforts. In contrast, most countries rely on the simpler 183-day rule to determine tax residency.

For individuals with diverse income sources, territorial taxation often strikes the best balance. It simplifies reporting while exempting most foreign earnings. When paired with tax and residency solutions and a solid grasp of tax treaties, this system can offer significant financial advantages.

How to Choose the Right Tax System

Factors That Determine the Best System

Your citizenship plays a major role in determining your tax obligations. For example, U.S. and Eritrean citizens are subject to citizenship-based taxation, meaning they owe taxes no matter where they live. For most other nationalities, tax obligations hinge on where you establish residency and where your income is generated. These core factors shape the foundation of any tax strategy tailored to individual circumstances.

The type of income you earn also matters. Active income, such as salaries or consulting fees, is taxed differently from passive income like dividends, interest, or capital gains. Territorial tax systems often exclude foreign-sourced income, which can work well for those earning from clients or investments outside their country of residence. Picture a digital consultant living in Panama but working with European clients – they might not owe Panamanian taxes on their income earned abroad.

Physical presence is another key factor, usually determined by residency tests like the 183-day rule in many countries or the U.S. Substantial Presence Test. Additionally, broader ties such as family, property, and economic interests help define your "center of vital interests". Understanding these elements is essential to align your residency with a solid asset protection plan.

Your domicile also plays a crucial role. Unlike residency, which can change based on where you live, domicile refers to your permanent home and can extend tax obligations even if you move abroad. For instance, in the U.K., the non-dom remittance basis charge can amount to £30,000 or £60,000 annually, depending on how long you’ve been a resident.

Recommendations by Profile

Different financial profiles call for tailored tax strategies. Here’s how some common scenarios align with tax systems:

- Digital Nomads: Territorial tax systems are a great fit for digital nomads. Countries like Panama, Malaysia, Georgia, and Costa Rica tax only locally sourced income, making them appealing for remote workers with international clients.

- High Earners: High earners can benefit from remittance-based systems in places like the U.K., Ireland, or Malta. These jurisdictions tax foreign income only when it’s brought into the country. This approach works well if you can keep a significant portion of your income offshore and limit what you bring in for local use.

- High-Net-Worth Individuals and Investors: Zero-tax jurisdictions such as the Bahamas, Cayman Islands, UAE, or Monaco are popular among wealthy individuals. While these places may impose other fees – like property taxes or stamp duties – they don’t levy income tax, offering a potential advantage for asset protection and preserving wealth.

- U.S. Citizens: U.S. citizens face unique tax challenges. The Foreign Earned Income Exclusion (FEIE) allows qualifying individuals to exclude up to $126,500 of earned income for the 2024 tax year, but passive income remains fully taxable regardless of residence. Strategic planning might include fully utilizing the FEIE or, in extreme cases, considering renunciation.

How Tax Treaties Affect Your Choice

Tax treaties add another layer of complexity and opportunity when choosing the right tax system. These agreements are designed to prevent double taxation and often reduce withholding taxes on income like interest, dividends, and royalties.

If you qualify for dual residency, tax treaties use tie-breaker rules to determine which country has taxing rights. These rules prioritize factors like your permanent home, center of vital interests, habitual abode, nationality, and, if necessary, mutual agreement between tax authorities.

Tax treaties also protect businesses from being taxed unfairly. For example, they ensure a country can’t tax your business profits unless you maintain a fixed place of business there, typically for at least six months (or 12 months for certain construction projects).

To claim treaty benefits, you’ll need to prove tax residency in one of the treaty countries. For U.S. taxpayers, this means submitting Form 8802 to obtain Form 6166 as proof of residency. Be mindful of "Limitation on Benefits" clauses, which can restrict treaty shopping, and remember that U.S. state tax rules may differ from federal treaty provisions.

Timing your move can also simplify things. Aligning with the start of the tax year – like April 6 in the U.K. or January 1 in most EU countries – makes transitioning to non-resident status easier. Proper documentation, such as travel logs, utility bills, and deregistration from your previous address, is essential to establish clear residency in a favorable jurisdiction and maintain a defensible tax position.

Tax Optimization and Compliance

Tax Optimization vs. Tax Evasion

When navigating global tax systems, it’s essential to distinguish between tax optimization and tax evasion. The difference lies in legality. Tax optimization uses lawful strategies to minimize tax liabilities, while tax evasion involves illegal actions that violate tax laws.

Tax optimization involves transparency and compliance with legal frameworks. For instance, setting up a holding company in Cyprus to take advantage of 0% withholding tax on dividends under a tax treaty is a legitimate strategy. On the other hand, hiding assets in undisclosed offshore accounts constitutes tax evasion and carries serious legal consequences.

A key aspect of effective tax planning is demonstrating commercial substance. This means having real operations, such as physical offices and employees, in the jurisdictions where your entities operate. A notable example is General Electric, which employed nearly 1,000 staff in its tax department as of September 2012 to ensure compliance with complex U.S. tax laws. Such efforts underscore the importance of adhering to legal requirements over taking illegal shortcuts.

International Reporting Requirements

Global tax transparency has increased significantly, requiring extensive reporting from individuals and businesses alike. Two major frameworks drive this transparency:

- The Common Reporting Standard (CRS): Over 100 jurisdictions participate in this system, where financial institutions automatically share information about account holders’ tax residency with local tax authorities.

- The Foreign Account Tax Compliance Act (FATCA): This U.S. law mandates that foreign financial institutions report details of accounts held by U.S. taxpayers to the IRS.

These systems rely on disclosure. When opening financial accounts, individuals must declare all tax residencies. Financial institutions then report account balances, interest, dividends, and other financial details to the relevant tax authorities. For U.S. persons, compliance also includes filing an FBAR (Report of Foreign Bank and Financial Accounts) for foreign accounts exceeding $10,000, in addition to FATCA reporting requirements.

In many low-tax jurisdictions, economic substance rules now require businesses to demonstrate real operations, such as having employees, physical offices, and actual expenses within the jurisdiction. U.S. shareholders of controlled foreign corporations face further reporting obligations under GILTI (Global Intangible Low-Taxed Income) and Subpart F rules. These provisions tax certain foreign earnings at rates starting at 10.5%, with an increase to 13.125% scheduled after 2025.

Understanding and complying with these reporting requirements is critical for aligning tax strategies with broader wealth protection goals.

Combining Tax Planning with Asset Protection

Tax planning works best when integrated with strategies for protecting wealth. Choosing a territorial tax jurisdiction, such as Panama or Georgia, allows you to build capital in a tax-neutral environment. This capital can then be moved into protective vehicles like trusts or estate planning structures.

Offshore trusts are particularly effective for separating legal ownership from control, enhancing asset protection, and potentially reducing estate tax exposure. Meanwhile, holding companies offer centralized management of assets, simplifying the transfer of subsidiaries and reducing tax leakage on dividends through treaty networks. For example, a well-structured holding company can leverage Double Tax Agreements to avoid double taxation on the same income while safeguarding cross-border assets.

Full disclosure is non-negotiable. Structures must comply with FATCA and CRS requirements to avoid penalties. Additionally, professional advice is invaluable. International tax laws are complex, and even minor errors can lead to fines or audits. Maintain detailed records to support residency claims and ensure compliance during audits. Proper documentation strengthens your legal position and keeps your wealth protection strategy on solid ground.

Conclusion

Understanding the four global tax systems – territorial, residential, citizenship-based, and source-based – is key to making smart financial decisions that could save you substantial amounts in taxes. Choosing the right tax strategy depends on your income sources, where you live, and your long-term financial goals.

Strategic tax planning can make a huge difference. For example, aligning your residency with a favorable tax system can legally reduce or even eliminate taxes on foreign-source income. Using tax treaties effectively can help avoid double taxation. For U.S. citizens living abroad, the 2026 Foreign Earned Income Exclusion allows eligible individuals to exclude up to $132,900 of foreign earnings from U.S. taxation. However, poor planning can lead to hefty penalties, such as FBAR fines of $10,000 per account per year for non-willful violations.

This is why working with a professional is so important. International tax laws are complex and change frequently. Experts can help you understand the difference between legal residence (where you’re allowed to live) and tax residence (where you’re taxed), navigate tie-breaker rules in tax treaties, and ensure compliance with global transparency standards. Missteps, like confusing a residency permit with tax status or failing to disclose offshore structures, can result in penalties that far exceed the taxes themselves.

FAQs

How do I know which country counts me as a tax resident?

Tax residency is determined by the specific rules of each country, which often take into account factors like the amount of time you’ve spent there (commonly 183 days or more), where your permanent home is located, and your personal or economic connections. For example, the United States bases tax residency on citizenship, while many other countries focus on physical presence or residency. It’s essential to check the detailed criteria for each country to figure out your tax status correctly.

Can I owe taxes in two countries on the same income?

Yes, it’s possible to be taxed on the same income by two different countries. For instance, U.S. citizens are required to pay taxes on their worldwide income, even if they’re living or working in another country. If the country where you’re residing or earning income also imposes taxes on that income, you might find yourself with dual tax obligations. However, tax treaties and credits between certain countries can help ease this burden, depending on the specific agreements in place.

What records do I need to prove my income is foreign-sourced?

To verify income earned outside the U.S., it’s important to maintain proper records. These can include foreign tax returns, bank statements, employment contracts, rental agreements, and other documentation that shows income received abroad. Keeping these records organized helps confirm the source of your income and ensures you meet tax compliance requirements.