Europe offers several low-tax jurisdictions for entrepreneurs, investors, and remote workers in 2026. These countries provide attractive tax rates, residency options, and incentives that can help you reduce your tax burden while aligning with international tax standards. Here’s a quick overview of the key highlights:

- Bulgaria: Flat 10% tax on both corporate and personal income. Simple residency requirements and EU membership make it appealing.

- Hungary: Lowest EU corporate tax rate at 9%. Flat 15% personal tax but higher social contributions.

- Estonia: 0% tax on retained profits, 22% on distributed profits. Flat 22% personal tax rate.

- Romania: Micro-enterprise tax as low as 1% on turnover for small businesses. Flat 10% personal tax.

- Cyprus: 15% corporate tax (from 2026). Non-Dom regime offers 0% tax on foreign dividends and interest.

- Malta: Effective corporate tax as low as 5% with shareholder refunds. Attractive residency programs for non-domiciled individuals.

- Montenegro: Corporate tax starts at 9%. Progressive personal tax up to 15%.

- Serbia: 15% corporate tax, 10% flat personal tax. Tax holidays for large investments.

- Czech Republic: 21% corporate tax, progressive personal tax (15%-23%). R&D incentives available.

- Croatia: 10%-18% corporate tax, progressive personal tax (up to 33%). One of the best digital nomad visas is available here.

- Liechtenstein: 12.5% corporate tax, progressive personal tax up to 24%.

- Andorra: 10% flat corporate and personal tax. Passive residency requires investment of $1 million.

Each country has unique residency requirements and tax incentives. For example, Andorra only requires 90 days of presence for passive residency, while most others require 183 days. EU member states also offer access to the single market and various tax treaties.

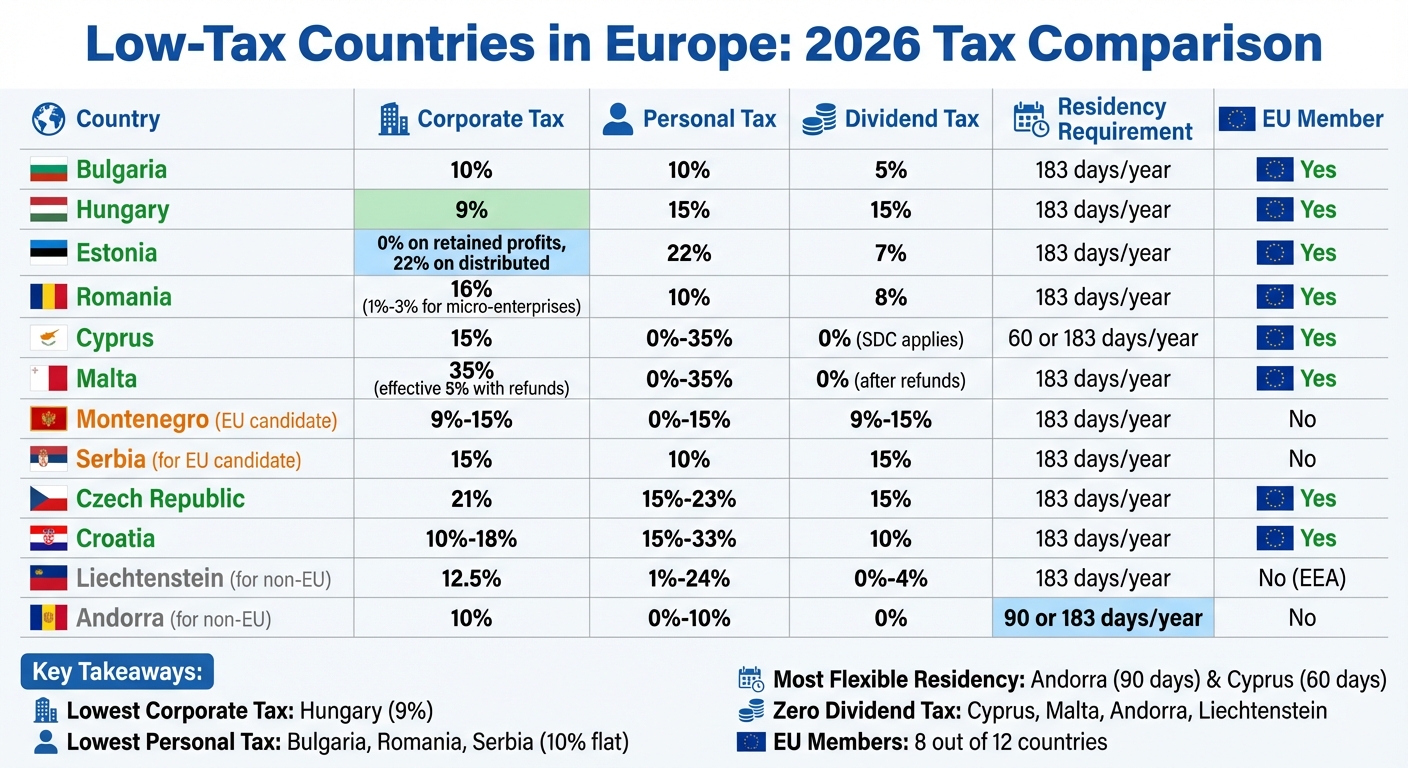

Quick Comparison

| Country | Corporate Tax | Personal Tax | Dividend Tax | Residency Requirement | EU Member |

|---|---|---|---|---|---|

| Bulgaria | 10% | 10% | 5% | 183 days/year | Yes |

| Hungary | 9% | 15% | 15% | 183 days/year | Yes |

| Estonia | 0% on retained profits, 22% on distributed profits | 22% | 7% | 183 days/year | Yes |

| Romania | 16% (1%-3% for micro-enterprises) | 10% | 8% | 183 days/year | Yes |

| Cyprus | 15% | 0%-35% | 0% (SDC applies) | 60 or 183 days/year | Yes |

| Malta | 35% (effective 5% with refunds) | 0%-35% | 0% (after refunds) | 183 days/year | Yes |

| Montenegro | 9%-15% | 0%-15% | 9%-15% | 183 days/year | No |

| Serbia | 15% | 10% | 15% | 183 days/year | No |

| Czech Republic | 21% | 15%-23% | 15% | 183 days/year | Yes |

| Croatia | 10%-18% | 15%-33% | 10% | 183 days/year | Yes |

| Liechtenstein | 12.5% | 1%-24% | 0%-4% | 183 days/year | No (EEA) |

| Andorra | 10% | 0%-10% | 0% | 90 or 183 days/year | No |

When choosing a jurisdiction, consider not just tax rates but also residency rules, cost of living, and lifestyle. For example, Bulgaria and Romania are budget-friendly, while Andorra and Liechtenstein cater to high-net-worth individuals. Always consult a tax advisor to align your plans with local regulations. If you are considering other Atlantic options, you might also explore the Portugal digital nomad visa requirements.

Low-Tax Countries in Europe 2026: Tax Rates and Residency Requirements Comparison

1. Bulgaria

Corporate Tax Rates

Bulgaria offers a flat 10% corporate tax rate for small and medium-sized enterprises. However, multinational companies with annual revenues exceeding €750 million (approximately $825 million) are subject to a 15% global minimum tax. For non-residents, dividends are generally taxed at a 5% withholding rate, though payments to EU/EEA parent companies are often exempt. Starting a company in Bulgaria is straightforward, requiring a minimum capital of just 2 BGN (around $1).

Personal Income Tax Rates

Bulgaria employs a flat 10% personal income tax, with no progressive brackets. Freelancers benefit from a 25% expense deduction, effectively reducing their tax rate to 7.5%. Some professions, like authors, lawyers, and craftsmen, can claim a 40% deduction, while registered farmers enjoy a 60% deduction. Additionally, capital gains from shares traded on the Bulgarian Stock Exchange or other regulated EU/EEA markets are tax-exempt, and residents don’t pay taxes on interest earned from EU/EEA bank accounts. Early taxpayers who file by March 31 and pay online can claim a 5% discount on their taxes, up to a maximum of 500 BGN (approximately $275). These incentives make Bulgaria an attractive option for individuals and businesses alike.

Residency Requirements

To become a tax resident in Bulgaria, you need to either spend over 183 days in the country within a 12-month period or demonstrate that Bulgaria is your economic center through residency, business activities, or other connections. EU/EEA and Swiss citizens can live and work in Bulgaria without a visa but must register for a residency certificate after 90 days. Non-EU citizens typically need a Type D long-stay visa followed by a residence permit, which can often be obtained through freelancer registration or company formation. The National Revenue Agency reviews tax residency annually, taking into account physical presence and economic ties.

EU Membership Status

Bulgaria has been a member of the European Union since 2007 and officially joined the Schengen Area in 2024. On January 1, 2026, Bulgaria adopted the Euro, eliminating currency exchange risks within the EU. This transition enhances access to the EU’s single market and tax-related directives, such as the Parent-Subsidiary and Interest and Royalties directives.

sbb-itb-39d39a6

2. Romania

Corporate Tax Rates

Romania is positioning itself as one of Europe’s low-tax jurisdictions for 2026, offering a dual corporate tax system tailored to businesses of different sizes. Small businesses classified as micro-enterprises – those with annual turnovers under €100,000 and at least one full-time employee – are taxed at 1% of their gross revenue. This threshold was lowered from €250,000 as of January 1, 2026.

"The micro-enterprise income tax regime, simplified from 1 January 2026, allows companies with annual revenue below €100,000 to pay a flat 1% tax on turnover – not on profit, but on gross revenue." – Alin Mihai, Managing Partner, Mihai Attorneys

Larger businesses with revenues exceeding €100,000, or those failing to meet micro-enterprise criteria, are subject to a 16% corporate tax. Additionally, companies with annual turnovers above €50 million face a 0.5% minimum turnover tax, although this is set to be removed in 2027. Dividend withholding tax will rise to 16% starting in 2026, though exemptions under the Parent-Subsidiary Directive remain available for EU parent companies.

Personal Income Tax Rates

Romania applies a flat 10% personal income tax on both employment and self-employment earnings. Employees also contribute 35% of their income to social security, with 25% allocated to pensions and 10% to health insurance, significantly increasing overall costs. Capital gains from securities are now taxed at 16%, up from 10%. However, investors may qualify for reduced rates between 1% and 6% by working through Romanian intermediaries.

The standard VAT rate is 21%, with a reduced rate of 11% applied to essentials like food, medicine, and accommodation. Romania’s direct tax revenue as a percentage of GDP is notably low at 4.8%, especially when compared to Germany’s 13.3% [22, 26, 27, 28].

Residency Requirements

Individuals can establish Romanian tax residency by spending more than 183 days in the country within a 12-month period or by having significant personal or professional ties there. Remote workers earning at least €2,000 per month can apply for a one-year digital nomad visa, similar to programs offered in Italy.

For businesses, registration as a Romanian legal entity is required, typically in the form of an SRL (Limited Liability Company) with a minimum share capital of RON 500. To qualify for the 1% micro-enterprise tax rate, companies must employ at least one full-time worker and keep annual revenues below €100,000. Newly established businesses must also open a Romanian bank account within 60 business days of registration to avoid fines of up to RON 10,000 and a "fiscally inactive" designation [22, 30].

Romania’s residency framework is evolving to align with its EU tax commitments, making it an appealing option for individuals and businesses alike.

EU Membership Status

Since joining the European Union in 2007, Romania has leveraged its membership to offer businesses access to the single market and EU tax benefits. Companies can use the reverse charge mechanism to issue VAT-free invoices to corporate customers with valid EU VAT IDs. They can also benefit from the exemptions under the Parent-Subsidiary Directive. Romania’s candidacy for OECD membership further highlights its dedication to international transparency and regulatory standards.

The 2026 tax reforms aim to align Romania’s policies with broader European standards while enhancing tax collection. The country has also emerged as a tech hub, boasting the highest number of certified IT specialists per 1,000 inhabitants in Europe. Additionally, the VAT registration threshold of approximately RON 395,000 (around $87,000) is significantly higher than the EU average of €22,000–€30,000, offering a competitive edge for businesses [22, 9, 28].

3. Hungary

Corporate Tax Rates

Hungary boasts the lowest corporate income tax rate in the European Union, set at a flat 9% – a clear draw for businesses looking for competitive taxation. This rate applies across the board to standard business structures like Kft and Zrt. Resident companies are taxed on their worldwide income, while non-residents only pay 9% on profits generated within Hungary.

Small businesses have the option to use the KIVA (Small Business Tax) regime, which applies a 10% tax on revenue instead of profit. This system replaces both the standard 9% corporate tax and the 13% employer social contribution tax. Starting in 2026, the eligibility threshold was expanded to include companies with fewer than 100 employees and annual revenues under HUF 6 billion (about $15.4 million). Additionally, Local Business Tax (HIPA) rates, ranging from 0% to 2%, provide further opportunities for tax optimization.

"The 9% corporate income tax (CIT) on companies – the lowest rate in the European Union and one of the lowest among all OECD countries." – TaxRavens

While Hungary’s corporate tax system is highly appealing, its personal tax structure tells a different story.

Personal Income Tax Rates

Hungary applies a flat 15% personal income tax to most income types, including wages, dividends, and capital gains. However, when social contributions are added – 18.5% from employees and 13% from employers – the effective tax rate on wages climbs to approximately 46.5%.

For 2026, the minimum monthly wage is set at HUF 322,800 (around $880). Families benefit from increased tax allowances starting in January 2026, and mothers under 30 enjoy full personal income tax exemptions without any income cap. Investors using a Long-Term Savings Account (TBSZ) see reduced taxes on investment income: 10% after three years and 0% after five years.

Residency Requirements

Hungary’s residency options complement its tax benefits. Individuals can establish tax residency by spending more than 183 days in the country within a 12-month period or by proving that Hungary is their primary center of interests.

Entrepreneurs can obtain a business residency permit, often called the Guest Self-Employment permit, by forming a Hungarian company – typically a Kft – with a minimum share capital of HUF 3 million (approximately $7,700). Applicants must be over 18, have no criminal record, and either employ at least five Hungarian or EU nationals for six months or demonstrate sufficient business income (usually over $1,600 per month).

For longer-term residency, Hungary offers the Golden Visa (Guest Investor Permit), which provides a 10-year option in exchange for a minimum investment of $250,000 in a government-approved real estate fund or a $1 million contribution to a public-interest trust. Remote workers earning at least $3,000 per month from non-Hungarian sources can apply for the White Card (Digital Nomad Visa), though this permit prohibits local employment or business activities. Business residence permits are initially valid for one year and can be renewed for up to two additional years.

EU Membership Status

Hungary’s membership in the European Union since 2004 enhances its attractiveness for businesses. Companies benefit from direct access to the EU Single Market and enjoy well-established legal and accounting systems. Hungarian residency also grants visa-free travel within the Schengen Area, allowing stays of up to 90 days within any 180-day period.

Hungary adheres to EU and OECD anti-avoidance measures, including the Anti-Tax Avoidance Directive, which ensures compliance and stability in international transactions. Additionally, the country typically imposes no withholding tax on dividends, interest, and royalties paid to foreign corporate entities, facilitating smooth profit repatriation. Hungary has signed over 80 double taxation treaties, although its treaty with the United States ended on January 1, 2024.

Looking ahead, Hungary is introducing incentives for clean technology investments, such as batteries, solar panels, and heat pumps. These projects, starting in 2026, can qualify for tax benefits of up to $30 million.

4. Montenegro

Corporate Tax Rates

Montenegro applies a progressive corporate tax system with rates based on profit brackets: 9% for profits up to €100,000, 12% for profits between €100,000 and €1,500,000, and 15% for profits exceeding €1,500,000. Businesses must register with the Tax Administration within 15 days of incorporation to comply with local regulations. Corporate tax returns and payments are submitted electronically, with a deadline of March 31 for the previous fiscal year.

Companies operating in less-developed municipalities may benefit from an 8-year tax holiday, capped at €200,000. Setting up a Limited Liability Company in Montenegro is straightforward, requiring a minimum share capital of €1, with state registration fees amounting to approximately €22. For payments to non-residents, a 15% withholding tax applies to dividends, interest, and royalties. However, Montenegro’s network of over 40 double taxation treaties can help reduce these rates. The standard VAT rate is 21%, with reduced rates of 7% and 15% for specific goods and services.

Personal Income Tax Rates

Montenegro offers a progressive personal income tax system, starting with a 0% tax rate for monthly earnings up to €700 – the highest non-taxable income threshold in Europe. Earnings between €701 and €1,000 are taxed at 9%, while income exceeding €1,000 is taxed at 15%.

Social contributions include a 10% pension and disability insurance charge for employees and a 0.5% unemployment insurance contribution from both employers and employees. Notably, health insurance contributions have been abolished. Capital gains and dividend distributions are taxed at 15%. Individuals are only required to file an annual tax return if they earn income not taxed at the source, with the filing deadline set for April 30 of the following year.

Residency Requirements

Tax residency in Montenegro is established by spending over 183 days in the country within a calendar year or if Montenegro is deemed the center of an individual’s vital interests. Starting in 2026, the country has adopted an integrated permit model that combines residence and work authorizations into a single administrative process. Temporary residence permits, typically valid for one year and renewable, can be obtained through employment, company formation as an executive, real estate ownership, or a digital nomad visa.

The digital nomad visa allows foreign professionals to stay for up to two years (renewable) if they earn at least €2,000 monthly from non-local sources. Business owners seeking residency must ensure their company contributes at least €5,000 annually in taxes and social contributions. For property-based residency, the taxable property value must be at least €150,000. Applicants may also be required to demonstrate financial stability by depositing between €3,650 and €7,300 in a local bank account. Permanent residency becomes an option after five years of continuous legal temporary residence, provided applicants meet language proficiency requirements. These diverse residency pathways cater to a variety of applicants, reflecting Montenegro’s evolving regulatory landscape.

EU Membership Status

While Montenegro is not yet part of the European Union, it is a leading candidate for EU membership and already uses the Euro as its official currency. As a NATO member, Montenegro continues to align its labor and tax laws with EU standards. In 2022, the country shifted from a flat tax system to a progressive one to meet EU guidelines. Further reforms planned for 2026 aim to strengthen administrative discipline and reinforce its alignment with European norms. These developments have positioned Montenegro as an appealing destination for expatriates and investors, particularly those looking to take advantage of opportunities before the potential "EU premium" comes into play.

5. Serbia

Serbia continues to stand out as a low-tax European destination for 2026, offering a mix of competitive tax policies, appealing incentives, and tax and residency solutions.

Corporate Tax Rates

Serbia applies a flat 15% corporate income tax to domestic companies and foreign branches. For businesses focused on intellectual property, the "IP Box" regime effectively reduces the tax rate to about 3% by excluding 80% of qualifying IP income. Large-scale investors can enjoy a 10-year corporate tax holiday if they invest over 1 billion RSD (approximately $8.5 million) and create at least 100 new jobs. To operate, companies must register with the SBRA and obtain a PIB.

The standard VAT rate is 20%, with a reduced 10% rate for specific goods and services. Businesses with annual turnover exceeding 8 million RSD (roughly $68,000) are required to register for VAT. Corporate tax filings are due within 180 days of the tax year-end, typically by June 30.

Personal Income Tax Rates

Personal income in Serbia is taxed at a flat 10%, covering employment, self-employment, and rental income. However, high earners face additional surtaxes: an extra 10% applies to income above 5,439,096 RSD (around $46,500), and a 15% surtax kicks in for income exceeding six times the average salary.

"Many expats are surprised to learn about Serbia’s annual income tax – it’s separate from monthly withholding and catches high earners who assume their tax obligations are fully handled by their employer." – Aleksandra Markovic, Founder, Tax Advisor Serbia

Social security contributions total approximately 35.05% of gross salary, divided between the employer (15.15%) and employee (19.9%). These contributions are capped at five times the average annual salary. Younger taxpayers – those under 40 years old as of December 31 – can benefit from an additional deduction equal to three times the average annual salary, significantly reducing their tax bill. Dividends and capital gains are taxed at 15%, and personal income tax returns must be submitted by May 15 each year.

Residency Requirements

Serbia offers accessible residency pathways alongside its tax benefits. Spending more than 183 days in the country or demonstrating that Serbia is your center of vital interests – such as family, home, or economic ties – can establish tax residency. Foreign nationals must first secure a residency permit to legally reside and eventually qualify as tax residents.

Starting a Limited Liability Company (DOO) in Serbia is straightforward, requiring minimal capital – just 100 RSD (about $1). Entrepreneurs and small business owners will find this particularly appealing. Additionally, Serbia has signed 64 double taxation treaties (as of 2024) with countries like EU member states, the UK, Canada, and the UAE, reducing withholding taxes on dividends, interest, and royalties. Real estate investors can avoid capital gains tax by holding property for at least 10 years, while the real estate transfer tax is 2.5% of the property price, and annual property tax is approximately 0.4% of the property value.

EU Membership Status

Although Serbia is not yet an EU member, it holds candidate country status and is actively aligning its regulations and tax policies with EU standards. This position offers a strategic advantage: businesses gain proximity and preferential access to EU markets through the Stabilisation and Association Agreement, while benefiting from lower tax rates compared to most EU countries. Serbia also has independent free trade agreements with nations like Russia and Turkey, which can be advantageous for certain industries, particularly manufacturing and exports.

Reforms tied to EU accession, such as the adoption of International Financial Reporting Standards (IFRS) and OECD transfer pricing guidelines, have further strengthened Serbia’s appeal to global investors by creating a more transparent and business-friendly environment.

6. Czech Republic

The Czech Republic provides a stable tax environment integrated within the EU framework, featuring a 21% corporate income tax rate and a progressive personal income tax system. While not the lowest in Europe, the country offers appealing incentives for research and development (R&D) and favorable options for freelancers and entrepreneurs.

Corporate Tax Rates

The corporate income tax rate remains at 21% as of 2026, offering consistency for investors. Special reduced rates apply to specific entities, such as 5% for qualifying investment funds and 0% for pension insurance institutions. This stability is key to long-term business planning.

From January 1, 2026, companies engaging in R&D can claim an enhanced 150% deduction on eligible costs up to CZK 50 million (about $2.1 million). For example, a software company in Prague with CZK 30 million in R&D expenses could increase its deduction base to CZK 45 million, saving CZK 3.15 million (roughly $135,000) compared to the standard 100% deduction. The VAT rate is set at 21%, with a reduced 12% rate for specific items like food and medical supplies. Corporate tax returns are due within 180 days of the fiscal year-end, with an extension available through a tax advisor.

Personal Income Tax Rates

The personal income tax system features two progressive brackets: 15% for income up to CZK 2,262,400 (approximately $96,900) and 23% for income above this threshold. Taxpayers also receive an annual credit of CZK 30,840.

Freelancers benefit from a "60/40" deduction method, which allows them to deduct 60% of gross income as expenses without needing receipts. For instance, a freelancer earning €60,000 (around CZK 1.5 million or $64,500) in 2026 could reduce their taxable base to €24,000. After applying the 15% tax rate and personal credit, their final tax bill would be approximately €2,370 – an effective tax rate of just 4%.

Employees contribute 11.6% of their salary (7.1% for social insurance and 4.5% for health insurance), while employers pay 33.8% (24.8% for social insurance and 9% for health insurance). There is no cap on the health insurance tax base. Additionally, capital gains and cryptocurrency profits are tax-free if assets are held for more than three years or if annual profits are under €4,000 (about $4,300), even for shorter holding periods. Personal income tax returns must be filed by April 1, or May 2 if submitted electronically.

Residency Requirements

Tax residency in the Czech Republic is determined by spending 183 days or more in the country within a calendar year, counting weekends and holidays. Alternatively, maintaining a permanent home – whether owned or rented – with the intent to reside there permanently also establishes residency. When residency is unclear, authorities assess the individual’s center of vital interests, considering factors like family ties, bank accounts, and professional affiliations.

Even without meeting the 183-day threshold, a registered permanent residence (trvalý pobyt) can trigger tax residency. Tax residents are taxed on their worldwide income, while non-residents only pay taxes on income sourced within the Czech Republic. Non-EU citizens may apply for permanent residence after five years of continuous temporary residence. To claim benefits under double taxation treaties, individuals can obtain a tax residency certificate from the Czech Tax Office for a fee of 100 CZK (about $4.30) per year.

EU Membership Status

As an EU member since May 1, 2004, the Czech Republic offers businesses seamless access to the European Single Market and adheres to EU regulations on VAT and other tax matters. This alignment ensures a familiar regulatory framework for international investors while maintaining competitive tax rates compared to Western Europe. The country’s tax system reflects the standards of developed European economies, providing a stable and predictable environment for businesses.

7. Croatia

Croatia is an appealing option for individuals and businesses looking for favorable tax conditions in Europe. With competitive corporate and personal tax rates, alongside incentives for digital nomads and returning emigrants, Croatia has positioned itself as an attractive destination. Since joining the EU in 2013 – and becoming part of the Eurozone and Schengen Area in 2023 – the country offers access to the European Single Market while maintaining lower tax rates compared to many Western European nations.

Corporate Tax Rates

Croatia applies a two-tier corporate income tax system. Businesses with annual revenues up to €1 million (around $1.08 million) are taxed at 10%, while those exceeding this threshold face an 18% rate. The standard VAT rate is 25%, with reduced rates of 13% and 5% for certain goods and services. Notably, starting January 1, 2026, e-invoicing will become mandatory for all business-to-business and business-to-government transactions.

Setting up a limited liability company (d.o.o.) in Croatia requires a minimum share capital of €2,500, with €625 payable upfront. Registration fees range between €1,000 and €2,000. These relatively low entry costs, combined with the tax system, make Croatia a practical choice for entrepreneurs.

Personal Income Tax Rates

Croatia’s personal income tax system is progressive, with rates determined by local municipalities. Income up to €60,000 is taxed at rates between 15% and 23%, while income above this amount is taxed between 25% and 33%. Additionally, individuals are entitled to a basic personal allowance of €600 per month, or €7,200 annually.

Specific exemptions further reduce the tax burden for certain groups:

- Digital nomads are fully exempt from taxes on foreign-sourced income, with the Digital Nomad visa now extended to 36 months as of 2025. Applicants must show a minimum monthly income of €2,540.

- Returning Croatian emigrants who have lived abroad for at least two years can enjoy a 100% income tax exemption on employment income for five years.

- Workers under 25 years old receive a full exemption on the lower tax bracket, while those aged 26 to 30 benefit from a 50% exemption.

- Capital income, including dividends and capital gains, is taxed at a flat rate of 12%, which is lower than the Czech Republic’s 15%.

For social contributions, employees pay 20% of their salary toward pension insurance (capped at a monthly base of €11,958, or roughly $12,875). Employers contribute 16.5% for health insurance without a cap. Freelancers earning up to €40,000 can opt for the paušalni obrt (lump-sum) regime, which can result in an effective tax rate as low as 3.30%.

Residency Requirements

Tax residency in Croatia is based on spending at least 183 days in the country or maintaining a long-term property. Individuals transitioning from non-resident to resident status must obtain a Personal Identification Number (OIB) and submit Form TU to the tax office. Tax residents are taxed on worldwide income, while non-residents are only taxed on income sourced within Croatia.

Local municipal rates also vary, meaning that choosing to live in a smaller town with a 15% lower-bracket rate instead of Zagreb, where rates can go up to 23%, can significantly reduce tax obligations.

EU Membership Status

Croatia’s EU membership, along with its inclusion in the Eurozone and Schengen Area, provides businesses with seamless access to the European Single Market. Companies benefit from the Parent-Subsidiary Directive, allowing for 0% withholding tax on dividends distributed within the EU. Additionally, Croatia has double taxation treaties with over 65 countries, including all EU member states and the United States.

8. Cyprus

Cyprus continues to be a popular choice for businesses and high-net-worth individuals, thanks to its favorable tax policies and benefits as a member of the European Union. With new changes coming into effect on January 1, 2026, the island nation is making adjustments to align with international tax standards while maintaining its appeal to investors.

Corporate Tax Rates

Starting January 1, 2026, Cyprus will increase its corporate tax rate from 12.5% to 15%, aligning with OECD Pillar II guidelines. Alongside this change, the government has removed stamp duty and extended the loss carry-forward period to seven years. A flat 8% tax will apply to profits from crypto-asset disposals, while the IP Box regime offers reduced tax rates on qualifying intellectual property profits, potentially as low as 3%. Additionally, businesses can take advantage of R&D super-deductions of 120%, which are available until 2030. Dividend income for holding companies remains fully exempt under participation exemption rules.

To access these tax benefits and avoid being classified as a "shell company", businesses need to establish a physical office, employ a local director, and maintain a Cypriot corporate bank account. The VAT rate remains steady at 19%.

Cyprus has also introduced updates to its personal tax structure to attract global investors and professionals.

Personal Income Tax Rates

Cyprus operates a progressive income tax system with rates ranging from 0% to 35%. Under the 2026 reforms, the tax-free threshold has been raised from €19,500 to €22,000, and the top tax rate now applies only to income exceeding €72,000.

For new residents, a 50% income tax exemption is available for earnings over €55,000. Additionally, the Non-Dom regime offers a 0% tax rate on dividends and interest for up to 17 years, though a 2.65% Health System contribution applies to dividends, capped at €180,000.

Retirees can benefit from a flat 5% tax rate on foreign pension income exceeding €5,000 annually. Meanwhile, capital gains from crypto-asset transactions are taxed at a flat rate of 8%. Both employees and employers will contribute 8.8% to social insurance starting in 2026.

Now let’s look at how Cyprus simplifies residency options for newcomers.

Residency Requirements

Cyprus offers two main pathways to tax residency. The standard 183-day rule applies to individuals spending more than 183 days in the country within a calendar year. Alternatively, the 60-day rule provides a more flexible option. To qualify under this rule, individuals must spend at least 60 days in Cyprus, avoid spending more than 183 days in any other single country, maintain a permanent residence (owned or rented), and engage in business, employment, or directorship in a Cyprus-based company.

As of January 1, 2026, individuals can qualify under the 60-day rule even if they are tax residents elsewhere. To meet the requirements, it’s important to keep detailed records like boarding passes, passport stamps, utility bills, and local bank transactions. Permanent residency can also be secured by investing at least €300,000 in real estate or local funds. Tax residents are taxed on their worldwide income, while non-residents are only taxed on income sourced within Cyprus.

EU Membership Status

Cyprus is a full member of the European Union and the Eurozone, providing businesses with access to the EU single market. This includes the benefits of EU directives, such as the Parent-Subsidiary Directive, which facilitates tax-efficient dividend distributions. Furthermore, Cyprus has double taxation treaties with more than 60 countries, including the United States, offering protection against dual taxation for international investors and businesses.

9. Malta

Malta offers a flexible corporate tax system with a dual-track approach. While the standard corporate tax rate is 35%, shareholder refunds can significantly reduce the effective rate. For example, shareholders can claim a 6/7 refund on trading income, effectively lowering the tax rate to 5%. For passive income and royalties, a 5/7 refund applies. Alternatively, the FITWI regime, introduced in 2025, offers a flat 15% tax rate without refunds, simplifying compliance with Controlled Foreign Company rules. This setup allows businesses to tailor their tax structure to their needs.

Personal Income Tax Rates

Malta’s progressive income tax system ranges from 0% to 35% for residents. Single individuals enjoy a tax-free threshold of €12,000 ($13,080), with income above €60,000 ($65,400) taxed at the top rate. Married couples filing jointly benefit from a higher tax-free threshold of €15,000 ($16,350), while families with two children see this threshold rise to €22,500 ($24,525).

Malta also offers tax advantages for non-domiciled residents through its remittance-based system. Non-doms only pay tax on Maltese-source income and foreign income if remitted to Malta, while foreign capital gains remain untaxed. However, non-doms earning over €35,000 ($38,150) from foreign income must pay a minimum annual tax of €5,000 ($5,450).

For non-EU nationals, the Global Residence Programme (GRP) provides a flat 15% tax rate on remitted foreign income, with a minimum annual tax of €15,000 ($16,350). Applicants must meet property criteria, such as purchasing real estate worth at least €275,000 ($299,750) or renting a property with a minimum annual rent of €9,600 ($10,464). Lower thresholds are available in Gozo and South Malta. Additionally, remote workers can benefit from the Nomad Residence Permit, which offers a 0% tax rate for the first 12 months and a 10% flat rate thereafter on eligible remote work income, provided they earn at least €42,000 ($45,780) annually.

Residency Requirements

To establish tax residency in Malta, individuals must spend more than 183 days in the country within a calendar year. GRP participants must also avoid spending over 183 days in any other single jurisdiction while maintaining a residence in Malta. The Malta Permanent Residence Programme (MPRP) requires applicants to demonstrate €500,000 ($545,000) in assets, purchase property valued at €375,000 ($408,750), or commit to an annual rent of €14,000 ($15,260). Additionally, participants must make a government contribution and donate €2,000 ($2,180) to a recognized NGO. Maintaining separate bank accounts can assist in managing tax obligations. These measures are designed to attract international investors by offering a clear and structured tax framework.

EU Membership Status

As a member of both the European Union and the Eurozone, Malta provides businesses with seamless access to the EU single market. It benefits from directives like the Parent-Subsidiary Directive, which supports tax-efficient dividend distributions. Malta has also signed double taxation agreements with 81 countries, including the United States, ensuring international investors are protected from dual taxation. Additionally, Malta’s VAT rate of 18% is among the lowest in the EU.

10. Estonia

Estonia stands out with its forward-thinking, digital-first approach to taxation, making it a prime choice for global entrepreneurs. The country operates a deferred corporate tax system that has kept it at the top of the International Tax Competitiveness Index for 12 straight years. Here’s how it works: companies pay 0% tax on retained and reinvested profits, while corporate income tax is only applied when profits are distributed as dividends. Starting in 2026, distributed profits are taxed at a flat rate of 22%, following the abolition of the reduced 14% rate for some dividend distributions on January 1, 2025.

Setting up a company in Estonia is incredibly efficient. Thanks to the e-Residency program, the entire process can be completed online – usually within one business day – for a state fee of around $289. There’s also virtually no minimum share capital requirement, making it even more accessible for entrepreneurs.

"Estonia’s core advantage stays intact in 2026. Companies pay zero tax on profits they keep in the business – whether for operations, equipment, hiring, or growth." – TaxRavens

This system not only simplifies corporate taxation but also aligns seamlessly with Estonia’s transparent personal tax policies and residency rules.

Personal Income Tax Rates

Estonia employs a flat 22% personal income tax rate, ensuring simplicity and predictability. Starting in 2026, the country will introduce a universal tax-free allowance of approximately $763 per month (or $9,156 annually), replacing the prior income-dependent system. Pensioners enjoy a slightly higher allowance of about $846 per month (or $10,152 annually). Employers, meanwhile, face a total social tax burden of 33.8%, which includes 33% for social tax and 0.8% for unemployment insurance. As for VAT, the standard rate has been set at 24%, a rate made permanent as of July 2025 [112,115].

Residency Requirements

Estonia also offers appealing residency options for digital entrepreneurs. To qualify as a tax resident, individuals must either spend at least 183 days in the country over a 12-month period or maintain a permanent residence there. However, the popular e-Residency program, while allowing digital management of Estonian companies, does not grant physical or automatic tax residency.

For those looking to live and work in Estonia, the Digital Nomad Visa allows non-EU nationals to stay for up to one year. However, staying fewer than 183 days typically means retaining tax residency in one’s home country. Businesses must also register a legal address in Estonia. If none of the board members are Estonian or EU residents, they must appoint a local contact person, which costs about $218 per year [112,115].

EU Membership Status

As a member of both the European Union and the Eurozone, Estonia provides businesses with seamless access to the EU single market. Through the Parent-Subsidiary Directive, qualifying intra-EU dividends may be exempt from withholding taxes. Estonia has also been proactive in updating its tax treaties, with new agreements with Qatar and Botswana taking effect in January 2026, and a treaty with Liechtenstein signed in July 2025.

Estonia’s digital infrastructure is another standout feature, with 98% of tax returns filed electronically. However, the Tax and Customs Board has ramped up scrutiny on VAT registrations for e-Residency companies that lack genuine economic activity [112,116].

11. Liechtenstein

Liechtenstein continues to stand out among European low-tax jurisdictions as we look ahead to 2026. Known for its strong privacy protections and straightforward tax system, it’s particularly attractive to high-net-worth individuals and family offices. While gaining residency in this small principality is notoriously challenging, those who succeed enjoy one of the most favorable tax setups in Europe. The country uses the Swiss Franc (CHF) as its currency and shares a customs union with Switzerland, adding to its economic stability and its reputation for banking privacy.

Corporate Tax Rates

Liechtenstein’s corporate tax system is straightforward, featuring a flat 12.5% tax on net profits – one of the lowest rates in the European Economic Area. Additionally, there are no withholding taxes on dividends, interest, or royalties. For multinational companies with consolidated revenues exceeding €750 million, a 15% global minimum tax applies under the OECD’s Pillar Two framework.

The jurisdiction also offers a 4% Notional Interest Deduction (NID) on qualifying equity, which can help reduce the effective tax rate. For businesses, the minimum annual corporate tax is CHF 1,800. Companies that manage private assets can opt for Private Asset Structure (PAS) status, which allows them to benefit from this lower tax rate. However, setting up a business in Liechtenstein can be costly, with expenses ranging from $10,000 to $50,000.

Personal Income Tax Rates

Liechtenstein uses a progressive personal income tax system, with a national base rate ranging from 1% to 8%. However, communal surcharges – ranging from 150% to 250% of the national tax – bring the effective top rate to approximately 22.4%–24%. Tax exemptions include CHF 15,855 for single individuals and CHF 31,710 for married couples.

The country does not impose a capital gains tax on the sale of shares or other movable assets, and there’s no separate wealth tax. Instead, a notional income equivalent to 4% of net wealth is added to taxable income. Inheritance and gift taxes were abolished in 2011, and the standard VAT rate is 8.1%.

For high-net-worth individuals who are not employed locally, a lump-sum taxation regime is available. This system bases taxes on living expenses rather than global income. Digital nomads also have the option to apply for a one-year visa, provided they meet the minimum annual income requirement of CHF 100,000.

Residency Requirements

Securing residency in Liechtenstein is no easy feat. For EEA and Swiss nationals, residence permits are issued twice a year – half through a lottery system and half through direct government allocation. Non-EEA nationals usually need to qualify as managers, specialists, or highly skilled professionals with relevant expertise.

Applicants who are not employed must demonstrate sufficient financial resources to avoid reliance on state assistance and must have comprehensive health insurance coverage. Tax residency is determined by either maintaining a permanent home in Liechtenstein or residing there for more than 183 days in a tax year. Additionally, third-country nationals are generally restricted from purchasing residential real estate until they’ve lived in the country for 10 years. Citizenship requires 30 years of residency, and dual citizenship is not permitted.

EU Membership Status

Though not an EU member, Liechtenstein is part of the European Economic Area (EEA) and the European Free Trade Association (EFTA). This allows the principality full access to the EU’s internal market, including the free movement of goods, people, services, and capital. At the same time, Liechtenstein retains its independent tax policies and is not obligated to implement all EU tax directives. However, it does adhere to EEA rules on competition and state aid, ensuring compliance while maintaining its advantageous tax environment.

12. Andorra

Tucked away in the Pyrenees between France and Spain, Andorra stands out as a top low-tax destination for 2026. With the Euro as its currency and a straightforward tax system, it offers a sharp contrast to its high-tax neighbors. Although Andorra isn’t part of the EU, it maintains a customs union for manufactured goods and has built a growing network of 22 double taxation agreements as of 2025, including recent pacts with the UK and Estonia.

In January 2026, the "Omnibus 2" law introduced stricter financial requirements for new residents. According to Marc Cantavella, Co-Founder of AndorraInc:

"Following the approval of the ‘Omnibus 2’ law in January 2026, the minimum requirements have been significantly tightened. Applicants must now invest at least €1,000,000 in Andorran assets".

This change addresses housing market pressures and has made residency more exclusive than before.

Corporate Tax Rates

Andorra’s 10% flat corporate income tax is among the lowest in Europe, applying to the worldwide income of resident companies. New businesses benefit from a reduced 2% rate in their first tax period, with a 50% base reduction for the first financial year. Since January 1, 2023, profitable companies face a minimum effective tax rate of 3% after deductions.

Holding companies enjoy exceptional benefits under the participation exemption regime, with 0% tax on dividends and capital gains from subsidiaries. However, to avoid being labeled as "shell companies", businesses must maintain a physical office of at least 215 square feet (20 square meters) and have local management. The minimum share capital for a Limited Liability Company is $3,200 (€3,000).

Andorra’s VAT, known locally as IGI, is just 4.5%, the lowest in Europe. Companies are required to make an advance corporate tax payment in the ninth month of their tax period, calculated as 50% of the prior year’s tax liability.

On top of these corporate advantages, Andorra also offers appealing personal income tax rates.

Personal Income Tax Rates

The first $25,600 (€24,000) of income is tax-free, with the next $17,100 (€16,000) taxed at 5%, and income above $42,700 (€40,000) taxed at 10%.

Dividends distributed by Andorran companies to local tax residents are fully exempt from personal income tax, preventing double taxation. Capital gains on stock sales are taxed at 0% if the individual owns less than 25% of the company’s share capital. Additionally, there are no wealth, inheritance, or gift taxes for direct heirs. Savings income is taxed at 10%, but the first $3,200 (€3,000) is exempt.

Andorra’s competitive tax structure is paired with residency options tailored to various needs.

Residency Requirements

To qualify as a tax resident in Andorra, individuals generally need to spend more than 183 days per year in the country. In 2026, Andorra introduced two distinct residency pathways, each with unique requirements:

- Active residency: Designed for entrepreneurs and self-employed individuals, this option requires establishing an Andorran company, owning at least 34% of it, and depositing $53,400 (€50,000) with the Andorran Financial Authority. Active residents must spend 183 days annually in Andorra and are permitted to work for local companies.

- Passive residency: Geared toward non-working individuals, this option now requires a minimum investment of $1,068,000 (€1,000,000) in Andorran assets as of January 2026. For property investments, each must be worth at least $854,400 (€800,000). Additionally, applicants must make a non-refundable deposit of $53,400 (€50,000), plus $12,800 (€12,000) per dependent. Passive residents are only required to stay 90 days per year and cannot work for Andorran companies.

Andorra also offers a digital nomad visa for remote workers earning at least $4,300 (€4,000) per month from non-Andorran sources. This visa requires a 90-day annual stay and a $3,200 (€3,000) application fee. U.S. citizens typically enter Andorra through France or Spain using their 90-day Schengen visa-free privileges or a digital nomad visa in Spain before applying for residency, as Andorra lacks an airport.

Since 2025, Andorran tax authorities have tightened their scrutiny of "effective residency", requiring proof such as bank statements, utility bills, and local purchase receipts before granting tax residency certificates. Citizenship, however, remains a long-term commitment, requiring 20 years of residency – one of the lengthiest timelines in Europe.

EU Membership Status

Andorra’s non-EU status plays a key role in its appeal as a low-tax jurisdiction. While not part of the European Union or Schengen Area, Andorra offers access to international markets through its growing network of double taxation agreements. Foreign nationals, including EU citizens, must secure a residency permit to live there.

This independence allows Andorra to maintain its low tax rates while adhering to international standards such as the OECD’s Common Reporting Standard for automatic tax information exchange. Experts frequently highlight Andorra’s tax-friendly environment and its strategic position as one of Europe’s most attractive business destinations.

Tax Rates and Residency Requirements Comparison

Here’s a breakdown of tax rates and residency requirements across 12 low-tax European jurisdictions:

| Country | Corporate Tax Rate | Personal Income Tax Rate | Dividend Tax | EU Member State | Minimum Residency for Tax Status |

|---|---|---|---|---|---|

| Bulgaria | 10% flat | 10% flat | 5% | Yes | 183 days/year |

| Romania | 16% flat (1-3% for micro-enterprises) | 10% flat | 8% | Yes | 183 days/year |

| Hungary | 9% flat | 15% flat | 15% | Yes | 183 days/year |

| Montenegro | 9% flat (15% for banks) | 9-15% progressive | 9% | No (Candidate) | 183 days/year |

| Serbia | 15% flat | 10% flat | 15% | No | 183 days/year |

| Czech Republic | 21% (15% for small businesses) | 15-23% progressive | 15% | Yes | 183 days/year |

| Croatia | 18% (10% for small businesses) | 23.6-35.4% progressive | 10% | Yes | 183 days/year |

| Cyprus | 12.5% | 0-35% progressive | 0% (SDC applies) | Yes | 183 days/year |

| Malta | 35% (effective 0-5% with refunds) | 0-35% progressive | 0% (after refunds) | Yes | 183 days/year |

| Estonia | 20% (on distributions only) | 24% flat | 7% | Yes | 183 days/year |

| Liechtenstein | 12.5% | 1.5-22.4% progressive | 0-4% | No (EEA) | 183 days/year |

| Andorra | 10% flat | 0-10% progressive | 0% | No | 183 days/year (active) or 90 days/year (passive) |

This table highlights not just the differences in tax rates but also how EU membership shapes regulatory frameworks and residency conditions. EU countries – such as Bulgaria, Romania, Hungary, Czech Republic, Croatia, Cyprus, Malta, and Estonia – are required to follow the Anti-Tax Avoidance Directive (ATAD). This directive includes rules like Controlled Foreign Company (CFC) measures and limits on interest deductions to curb tax avoidance practices. In contrast, non-EU jurisdictions like Montenegro, Serbia, Liechtenstein, and Andorra enjoy more independence in setting their tax policies.

A few unique features stand out. Estonia plans to increase its flat personal income tax rate to 24% by 2026. Meanwhile, the Czech Republic offers freelancers a "60/40 method", allowing a 60% lump-sum expense deduction, effectively reducing their income tax rate to around 4%. Additionally, most of these jurisdictions allow foreigners to establish and fully own companies, including Bulgaria, Romania, Hungary, Serbia, Croatia, Cyprus, Malta, and the Czech Republic.

Residency requirements also vary slightly. While most jurisdictions demand a minimum presence of 183 days per year to qualify for tax residency, Andorra offers a passive residency option requiring only 90 days annually. These details enable entrepreneurs and investors to align their tax strategies with their personal and financial priorities.

What to Consider Before Moving in 2026

Before making a move in 2026, it’s important to think through several key factors: living costs, healthcare, language accessibility, financial obligations, and residency requirements.

Living costs can vary a lot depending on where you’re headed. For instance, in Bucharest, Romania, renting a one-bedroom apartment in the city center can cost between €500–€900 ($530–$955) per month. A single expat might need a monthly budget of around €900–€1,600 ($955–$1,700) to cover overall expenses. Bulgaria and Serbia are even more affordable, with cost of living indices of 41.6 and 42.6, respectively, compared to New York City’s index of 100. Grocery bills across the region are relatively consistent, ranging from €250–€450 ($265–$477) per person per month, while eating out costs about €8–€15 ($8.50–$16) in Central and Eastern Europe, compared to €15–€25 ($16–$27) in Western Europe. These estimates give a good starting point for budgeting your relocation.

Healthcare access is another crucial consideration. In places like Bulgaria, Romania, Cyprus, and Malta, public healthcare systems are still developing, so private health insurance is often necessary. Countries such as the Czech Republic and Estonia have public systems that meet EU standards, while Liechtenstein offers care comparable to Switzerland’s. For short-term stays, UK or EU citizens can use an EHIC/GHIC card for healthcare in EU/EEA countries, but long-term residents will need to enroll in local systems or purchase International Private Medical Insurance (IPMI), which typically costs between €50–€200 ($53–$212) per month. Notably, Andorra mandates private insurance for residency.

Language and cultural accessibility can significantly impact your daily life. Malta and Cyprus are more English-friendly, making them easier for English speakers to navigate. On the other hand, countries like Bulgaria, Hungary, and Romania often have limited English usage outside major cities. For example, in January 2026, a client successfully integrated into the Czech Republic’s business community with help from Pexpats, an agency that assisted with setting up essentials like bank accounts and SIM cards. In Bulgaria, proving fiscal residency might require demonstrating that the country is your primary social and economic base. Language barriers and integration challenges should be weighed alongside financial considerations.

Financial obligations are another critical factor. In Romania, social security contributions can reach around 35%, which might outweigh the appeal of its 10% flat income tax for high earners [[74]](https://indotinc.com/articles/Tax Rates for Expats in the EU.php). Property taxes, however, are relatively low – about 0.15% in Bulgaria and 0.1% in Romania annually. Many countries now offer Digital Nomad Visas, which come with minimum monthly income requirements ranging from €1,500 in Bulgaria to €3,700 in Romania. Public transportation costs are also worth noting, with monthly passes priced between €40–€90 ($42–$95), depending on the city.

Residency requirements often hinge on physical presence. Most countries expect residents to spend at least 183 days per year within their borders. Andorra offers more flexibility with only 90 days required for passive residency, while Cyprus requires just 60 days. In Montenegro, however, being away for more than 30 consecutive days could lead to residency termination. Malta takes a stricter approach, requiring "actual residence" that reflects genuine community involvement – not just a formal address. To maintain your tax residency status, it’s wise to keep evidence of your local ties, such as utility bills, bank statements, or memberships in local organizations. These tangible connections can help secure your residency if questioned.

Conclusion

Europe’s tax-friendly options in 2026 provide plenty of opportunities for individuals and businesses aiming to reduce their tax burdens. Hungary stands out with the EU’s lowest corporate tax rate at 9%, while Bulgaria keeps things simple with a 10% flat tax on both personal and corporate income. Estonia offers a unique approach, allowing businesses to reinvest profits tax-free, and Romania’s micro-enterprise scheme can lower taxes to just 1% on turnover for eligible companies. Meanwhile, Cyprus and Malta appeal to international professionals with non-domiciled regimes, where foreign-sourced income may remain untaxed if not brought into the country.

However, picking the right jurisdiction involves more than just looking at tax rates. It’s crucial to assess the full tax picture, including corporate, dividend, and personal income taxes. As the GO-EU Guide advises, "The safest way to choose a low-tax country is to look at the full picture: corporate tax + dividend tax + income tax". Other factors, like residency rules, substance requirements, cost of living, healthcare options, and double tax treaties, are equally important. For instance, Cyprus only requires 60 days of residency per year to qualify.

Tax authorities in 2026 are paying closer attention to "center of life" indicators. It’s no longer enough to simply be present in a country – proof of genuine ties, such as utility bills or local bank accounts, is often required. Without meeting substance rules, companies risk being taxed in their home country, erasing any potential tax savings.

Every situation is different. A plan that works for a digital entrepreneur might not suit a high-net-worth individual or a startup. Consulting experienced tax advisors who understand both your current needs and the regulations of your target country is essential. Tailor your strategy to match your income type, lifestyle, and long-term goals instead of focusing solely on the lowest tax rate. This thoughtful approach will ensure you make the most of Europe’s tax opportunities in 2026.

FAQs

How do I avoid being taxed in two countries after moving?

When relocating, it’s essential to take steps to avoid double taxation. Start by establishing tax residency in just one country and adhering to its tax regulations. Many countries have tax treaties in place, which can allow you to claim credits or exemptions to reduce your tax burden. Additionally, consider how your income and assets are structured to align with the tax rules of your new country.

To qualify as a resident for tax purposes, you may need to meet specific criteria, like maintaining a physical presence for a certain number of days or having legal and financial ties to the country. Since tax laws can be complex and vary widely, working with a qualified tax advisor can help you navigate these requirements and create a plan tailored to your unique circumstances.

Do I need to form a company to get low-tax treatment?

In some places, individuals might enjoy low personal income tax rates or take advantage of favorable residency programs without needing to set up a company. That said, forming a company can be a smart move for entrepreneurs or investors aiming to manage their tax responsibilities more effectively – especially in regions with lower tax rates.

What proof of “substance” do tax authorities usually require?

Tax authorities often demand proof that a company has real economic substance to ensure it isn’t merely a "letterbox" entity. This involves showing evidence of genuine business activities, such as actual decision-making processes, operational tasks, and a tangible presence like office space or employees. These elements help confirm that the entity is engaged in legitimate business and meets substance regulations.