Wealthy individuals use multiple citizenships as tools for financial security, tax efficiency, and global mobility. This strategy, often called a "passport portfolio", allows them to reduce risks tied to a single country while gaining access to better legal protections, healthcare, and business opportunities. Here’s how they do it:

- Tax Benefits: Countries like the UAE, Monaco, and St. Kitts & Nevis offer zero or low-tax environments, helping reduce tax burdens.

- Mobility: Passports with visa-free travel to 150+ countries provide flexibility for business and personal travel.

- Asset Protection: Jurisdictions like St. Kitts & Nevis offer legal structures to safeguard wealth from creditors.

- Diversification: Holding citizenships across different regions reduces reliance on one country’s policies.

Programs like those in the Caribbean, UAE, and Vanuatu are popular for their efficient processing and benefits. However, compliance with international tax laws, such as FATCA and CRS, is essential. Many wealthy individuals work with advisors to align citizenship, tax residency, and business interests for maximum efficiency.

Key takeaway: Building a citizenship portfolio is about more than travel – it’s about financial security, legal protection, and long-term flexibility.

How to Structure a Citizenship Portfolio

Creating a citizenship portfolio is about strategically aligning legal and financial systems to support a well-rounded wealth strategy. For the wealthiest individuals, each citizenship is a calculated investment, chosen to enhance protection and flexibility across jurisdictions.

Spreading Risk Across Multiple Jurisdictions

Diversifying across jurisdictions helps mitigate reliance on a single country’s policies. This approach, often called "sovereign diversification," treats citizenship as part of a mobility portfolio rather than just a legal status. It’s about reducing exposure to risks like economic instability or political upheaval in any one place.

A common tactic is "stacking" citizenships, where each one serves a different purpose. For instance:

- EU residency ensures business continuity and access to stable banking.

- Caribbean citizenship provides visa-free travel and tax advantages.

- Middle Eastern bases like the UAE offer a zero-tax environment and capital access.

This layered approach creates a level of protection and flexibility that no single passport can provide. The growing popularity of this strategy is evident in the Grenada Citizenship by Investment Program. Between 2022 and 2023, applications jumped from 1,251 to nearly 1,700, while total investments skyrocketed from $132.8 million to $308.6 million.

Weighing Travel Access, Taxes, and Asset Security

When considering citizenship options, the decision goes beyond visa-free travel. Wealthy individuals evaluate three key factors: global mobility, tax efficiency, and asset protection.

While travel access is important, it’s just the beginning. A passport offering visa-free entry to over 150 countries is valuable for flexibility, but it also needs to support stronger legal protections and reliable asset structures.

Tax efficiency plays a major role. For U.S. citizens, who are taxed on worldwide income, acquiring another citizenship can be a step toward renouncing U.S. citizenship to reduce tax burdens. On the other hand, establishing tax residency in zero-tax jurisdictions like the UAE, Monaco, or Singapore can significantly lower obligations – but only if structured correctly.

"The tax optimization potential of multiple citizenships isn’t just about lower rates. It’s about alignment between your citizenship, residency, and business interests to create legitimate structures that maximize efficiency while maintaining compliance." – Jake Claver, QFOP

Other considerations include "economic mobility" – the share of global GDP accessible with a particular passport – as well as healthcare quality, education options, and banking stability. These factors determine whether a citizenship offers long-term benefits or just short-term perks.

Meeting International Tax Reporting Requirements

Even with the benefits of mobility and tax advantages, compliance is non-negotiable. Holding multiple citizenships often comes with complex reporting obligations, and ignoring these can lead to hefty penalties. Simply acquiring a second passport doesn’t alter tax obligations – formal changes in tax residency are required, and even then, some reporting rules remain.

For U.S. citizens, compliance is particularly strict. The Foreign Account Tax Compliance Act (FATCA) mandates reporting all foreign financial assets, regardless of citizenship. Similarly, many citizenship-by-investment countries, including those in the Caribbean, participate in the OECD‘s Common Reporting Standard (CRS), which facilitates automatic information sharing between nations. This means transparency with tax authorities is essential.

To navigate these challenges, a multidisciplinary approach is key. Citizenship planning should involve legal, tax, and estate advisors familiar with cross-border regulations. Reporting offshore structures early can help avoid penalties. The goal isn’t to hide assets but to structure them legally for tax efficiency while staying fully compliant.

In November 2025, Grenada introduced enhanced compliance measures in line with international anti-money laundering (AML) standards, ensuring greater traceability for investments. As stricter oversight becomes the norm across major programs, professional guidance is increasingly critical for building a multi-jurisdictional portfolio.

sbb-itb-39d39a6

Leading Citizenship-by-Investment Programs in 2026

The citizenship-by-investment (CBI) market in 2026 showcases a mix of well-established Caribbean programs, quick Pacific solutions, and emerging opportunities in the Middle East. Globally, this industry generates around $22 billion annually, with some small nations relying on these programs for up to 40% of their GDP.

Caribbean Citizenship-by-Investment Programs

The Caribbean remains a cornerstone of the CBI market, offering affordability, efficient processing, and visa-free travel options. In March 2024, five Caribbean nations – St. Kitts and Nevis, Dominica, Grenada, Antigua and Barbuda, and St. Lucia – agreed on a unified minimum investment threshold of $200,000.

- Dominica: Known for its affordability, Dominica’s program starts at $200,000 for donations or real estate investments. The program has funded over 5,000 climate-resilient homes and contributed $230 million to the country’s economy in 2023 – equivalent to 37% of its GDP. Processing takes 6–12 months, and strict compliance measures led to the revocation of 260 citizenships in 2023 for false information submissions.

- Grenada: This program combines Caribbean mobility with access to the U.S. E-2 Investor Visa. The minimum investment is $235,000 for donations or $270,000 for real estate. In 2024, Grenada secured $412 million in investments and issued over 3,000 passports by mid-year, reflecting a 27% rise in applications. Processing takes 3–8 months.

- St. Kitts and Nevis: As the oldest CBI program (launched in 1984), St. Kitts and Nevis offers visa-free access to 157 destinations. With a minimum investment of $250,000 for donations or $325,000 for real estate, applicants can opt for accelerated processing, receiving approval in just 2–3 months. A shift to a dedicated government authority in 2024 led to a 169% surge in applications.

- St. Lucia: This program offers a $300,000 government bond option, refundable after five years, alongside standard donations starting at $240,000.

- Antigua and Barbuda: Particularly appealing to families, this program allows the inclusion of siblings and offers a University of the West Indies (UWI) donation route for families of six or more. Minimum investments are $230,000 for donations or $300,000 for real estate. Applications soared by 205% in the first half of 2024.

All Caribbean programs now enforce mandatory virtual interviews for applicants over 16 to meet global security standards.

Vanuatu Fast-Track Citizenship Option

For those prioritizing speed, Vanuatu offers one of the fastest CBI programs. With a minimum investment of $130,000, government processing takes just 30–60 days, and the entire process is completed within 4–7 months. However, the program faced challenges after the EU suspended its Schengen visa waiver in December 2024, leading to a 50% drop in revenue. Additionally, applicants must now travel to Dubai, Hong Kong, or Port Vila for biometric enrollments. Despite these hurdles, Vanuatu remains attractive for its quick processing.

UAE Long-Term Residency and Citizenship Pathways

The United Arab Emirates offers a hybrid model, combining long-term residency through its Golden Visa program with selective citizenship options for prominent investors. The UAE passport, ranked first globally in 2026, provides visa-free access to 179 destinations. With no personal income tax, the UAE is a popular choice for high-net-worth individuals seeking tax efficiency. While citizenship is discretionary, many investors pair UAE residency with other passports to maximize their travel and business opportunities.

"In 2026, second citizenship no longer sits in the ‘nice to have’ category. Investors pursue it for speed, mobility, flexibility, and insurance against uncertainty." – APEX Capital Partners

Emerging Programs

New players in the CBI market include:

- Nauru: Launched in January 2025, this program focuses on climate resilience funding, with a $105,000 minimum investment.

- São Tomé and Príncipe: Offers a fully remote application process with a $90,000 minimum investment.

- El Salvador: Introduced the Freedom Visa, requiring a $1 million investment exclusively in Bitcoin or USDT.

While these newer programs provide lower entry points and distinct features, they lack the track record of the Caribbean options. Together, these diverse pathways allow investors to build a flexible citizenship portfolio tailored to their financial and personal goals.

Combining Citizenship, Residency, and Tax Planning

Blending citizenship, residency, and offshore structures creates a well-rounded strategy that supports portfolio diversification while ensuring compliance with international tax laws. Together, these elements form a framework designed to protect assets and optimize financial outcomes.

Using Multiple Residencies and Citizenships for Risk Management

High-net-worth individuals often rely on multiple citizenships and residencies to spread their legal and financial exposure across different jurisdictions. This "jurisdictional diversification" helps reduce the risk of any single government having full control over their wealth. While minimizing tax burdens is a factor, the broader goal is to manage overall legal and financial risks.

For U.S. citizens – who are taxed on worldwide income – second citizenships can offer a path to renounce U.S. taxation. Programs in countries like St. Lucia or Dominica provide such opportunities. By combining this with controlled residency in low-tax jurisdictions, such as St. Kitts & Nevis (which imposes no personal income, capital gains, or inheritance taxes), individuals can avoid being taxed as residents in high-tax countries. This approach, often referred to as the "fiscal nomad" strategy, requires meticulous record-keeping and expert guidance to navigate complex tax treaties and residency rules.

"The tax optimization potential of multiple citizenships isn’t just about lower rates. It’s about alignment between your citizenship, residency, and business interests to create legitimate structures that maximize efficiency while maintaining compliance."

- Tax attorney specializing in international planning

Another advantage of second citizenships is improved access to global banking. With an alternative passport, individuals can open accounts in financial hubs like Switzerland or Singapore, which may simplify certain reporting requirements depending on the agreements between jurisdictions.

To strengthen asset protection even further, many investors turn to offshore legal structures.

Using Offshore Structures for Asset Protection

In addition to leveraging citizenship and residency, offshore structures like trusts and International Business Companies (IBCs) play a key role in safeguarding wealth and maintaining financial privacy.

For example, Anguilla – a British Overseas Territory – offers a stable legal environment with no income, capital gains, inheritance, or corporate taxes. Its High-Value Resident (HVR) program requires an annual tax payment of $75,000, providing a straightforward option for those seeking tax efficiency and legal stability.

Pairing St. Kitts & Nevis citizenship with a Nevis trust is another popular strategy. Nevis trusts provide robust asset protection by requiring creditors to post a $100,000 bond and meet a "beyond reasonable doubt" standard – typically reserved for criminal cases – when pursuing claims. This creates a formidable barrier against creditor challenges.

IBCs in Caribbean jurisdictions also offer benefits by legally separating personal assets from business holdings. These companies often enjoy tax neutrality on foreign income, adding another layer of financial efficiency.

Timing is crucial when establishing these structures. Citizenship processes can take anywhere from one month (as in Vanuatu) to three years (as in Malta). Delays in setting up these frameworks during stable periods can jeopardize long-term wealth protection. Recognizing this, many family offices are now incorporating citizenship and residency planning into their core services, ensuring that legal positioning across multiple jurisdictions complements traditional investment management.

How to Evaluate Citizenship Programs

When assessing citizenship programs, it’s essential to weigh various priorities. While global mobility often takes center stage, the sheer number of visa-free destinations isn’t the only measure of value. For high-net-worth individuals, access to key regions like the Schengen Area, the UK, Hong Kong, and Singapore often holds more weight than just a high visa-free count. For instance, the UAE passport, projected to rank #1 globally in 2025 with visa-free access to 179 destinations, highlights how strategic access can be more impactful than raw numbers.

Other critical factors include tax benefits and political stability. Jurisdictions with 0% personal income tax or territorial tax systems – such as St. Kitts & Nevis, Antigua and Barbuda, and Vanuatu – offer significant advantages for preserving wealth. Citizenship also ensures the right of entry during emergencies like geopolitical crises or pandemics, a benefit that proved invaluable during the travel restrictions of 2020–2021, when residency-only holders often faced limitations.

Processing time and family inclusion are additional considerations. Vanuatu, for example, processes applications in as little as 30 days, while Caribbean programs generally take 6–10 months due to stricter vetting processes. Including spouses, children, and other dependents in a single application strengthens long-term wealth protection across generations.

"The investment citizenship market is undergoing a transformation from competition based on price to competition based on speed and the conditions for obtaining passports for the entire family."

- Elena Garnitsarik, Head of Legal, Passportivity

Banking access is another practical advantage. A second passport can simplify meeting Know Your Customer (KYC) requirements and help avoid automatic blocks at international banks, particularly for individuals from sanctioned countries. For those managing cross-border operations, this benefit often outweighs even tax savings.

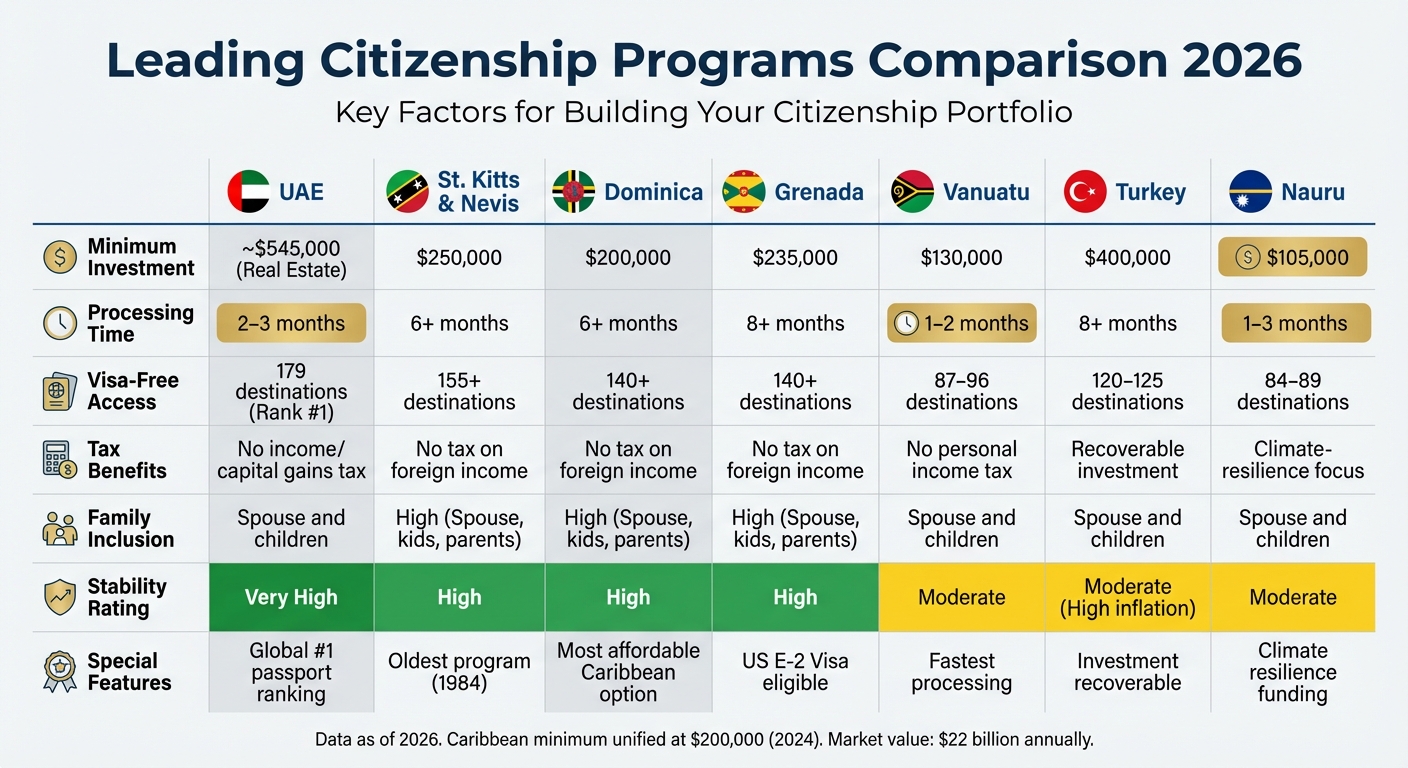

Comparison of Citizenship Programs

The table below highlights key features of leading citizenship programs:

| Country | Min. Investment | Processing Time | Visa-Free Access | Tax Benefits | Family Inclusion | Stability Rating |

|---|---|---|---|---|---|---|

| UAE | ~$545,000 (Real Estate) | 2–3 months | 179 (Rank #1) | No income/capital gains tax | Spouse and children | Very High |

| St. Kitts & Nevis | $250,000 | 6+ months | 155+ | No tax on foreign income | High (Spouse, kids, parents) | High |

| Dominica | $200,000 | 6+ months | 140+ | No tax on foreign income | High (Spouse, kids, parents) | High |

| Grenada | $235,000 | 8+ months | 140+ | No tax on foreign income | High (Spouse, kids, parents) | High (US E-2 Visa eligible) |

| Vanuatu | $130,000 | 1–2 months | 87–96 | No personal income tax | Spouse and children | Moderate |

| Turkey | $400,000 | 8+ months | 120–125 | Recoverable investment | Spouse and children | Moderate (High inflation) |

| Nauru | $105,000 | 1–3 months | 84–89 | Climate-resilience focus | Spouse and children | Moderate |

Caribbean programs remain a benchmark in the industry, partly due to the unified minimum investment threshold of $200,000 introduced in 2024 under increasing regulatory scrutiny. Grenada, in particular, stands out for its eligibility for the US E-2 Investor Visa, enabling its citizens to live and work in the United States through business investments.

It’s vital to regularly check visa-free access statuses to ensure a program aligns with current travel and regulatory needs. With the citizenship-by-investment market valued at around $22 billion, many investors now diversify by acquiring multiple citizenships to guard against potential changes in visa-free access.

Conclusion: Creating Your Citizenship Portfolio

A citizenship portfolio is more than just a document – it’s a tool to protect your wealth, secure your family’s future, and provide flexibility in an unpredictable world. For the wealthiest individuals, citizenship isn’t just about where they live; it’s about having mobility capital – a resource they can use when political, economic, or personal situations change.

The best time to build your portfolio is during stable periods. Waiting until a crisis hits can lead to missed opportunities and higher costs.

Your portfolio should reflect your long-term priorities, whether that’s reducing taxes, safeguarding assets, preparing for climate challenges, or accessing better educational opportunities. A well-rounded strategy often includes four key components: an EU base, a North or Latin American anchor, a Middle Eastern or Asian hub, and a wildcard option. This setup ensures no single government can fully restrict your mobility or control your assets. It’s about spreading risk and enhancing financial and personal security.

Navigating this process requires professional expertise. Legal, tax, and citizenship advisors play a critical role in ensuring your plan complies with international regulations. With the citizenship-by-investment market now exceeding $20 billion annually, having the right guidance is more important than ever.

At Global Wealth Protection, we specialize in turning these concepts into actionable plans. From offshore company formation to asset protection trusts and tax strategies, we help you create a citizenship portfolio designed for resilience and success.

FAQs

How do I legally change my tax residency after getting a second passport?

Changing your tax residency after acquiring a second passport requires careful planning and documentation. The process typically involves cutting ties with your previous country, building new connections in another jurisdiction, and following the necessary legal steps. Here’s how it works:

- Choose the right jurisdiction: Select a country with favorable tax policies that align with your financial goals.

- Meet residency requirements: Fulfill the specific criteria for establishing residency, such as spending a minimum number of days in the new country.

- Reduce ties to your former country: This might include selling property, closing local bank accounts, or resigning from memberships that suggest ongoing connections.

- Comply with new tax laws: Stay informed about the tax regulations in your new country to avoid penalties or disputes.

Seeking advice from a tax professional is highly recommended to navigate this complex process and ensure you meet all legal requirements.

What are the biggest risks of holding multiple citizenships (tax, banking, reporting)?

Holding multiple citizenships can come with its fair share of challenges. One of the biggest concerns is increased tax obligations. Depending on the countries involved, you might be required to pay taxes in more than one jurisdiction. This could lead to double taxation, where the same income is taxed by two different governments.

Another issue is the complex reporting requirements. For example, U.S. citizens with foreign accounts may need to file an FBAR (Foreign Bank Account Report) if their account balances exceed certain thresholds. Missing these filings can result in hefty penalties.

On top of that, financial institutions and regulators may subject you to greater scrutiny. With global transparency laws tightening, such as FATCA, banks and other entities are often required to ensure compliance, which can make managing your finances more complicated.

Which citizenship-by-investment option fits my goals: speed, travel access, or asset protection?

The best citizenship-by-investment program depends on what matters most to you – whether it’s how quickly you can get it, the travel perks it offers, or how well it protects your assets.

- Speed: If time is your top concern, there are programs that can grant citizenship in just a few months.

- Travel access: For frequent travelers, countries offering extensive visa-free travel – like many in the Caribbean or Europe – might be the perfect fit.

- Asset protection: If safeguarding your wealth is your priority, look for jurisdictions known for strong legal protections and confidentiality.