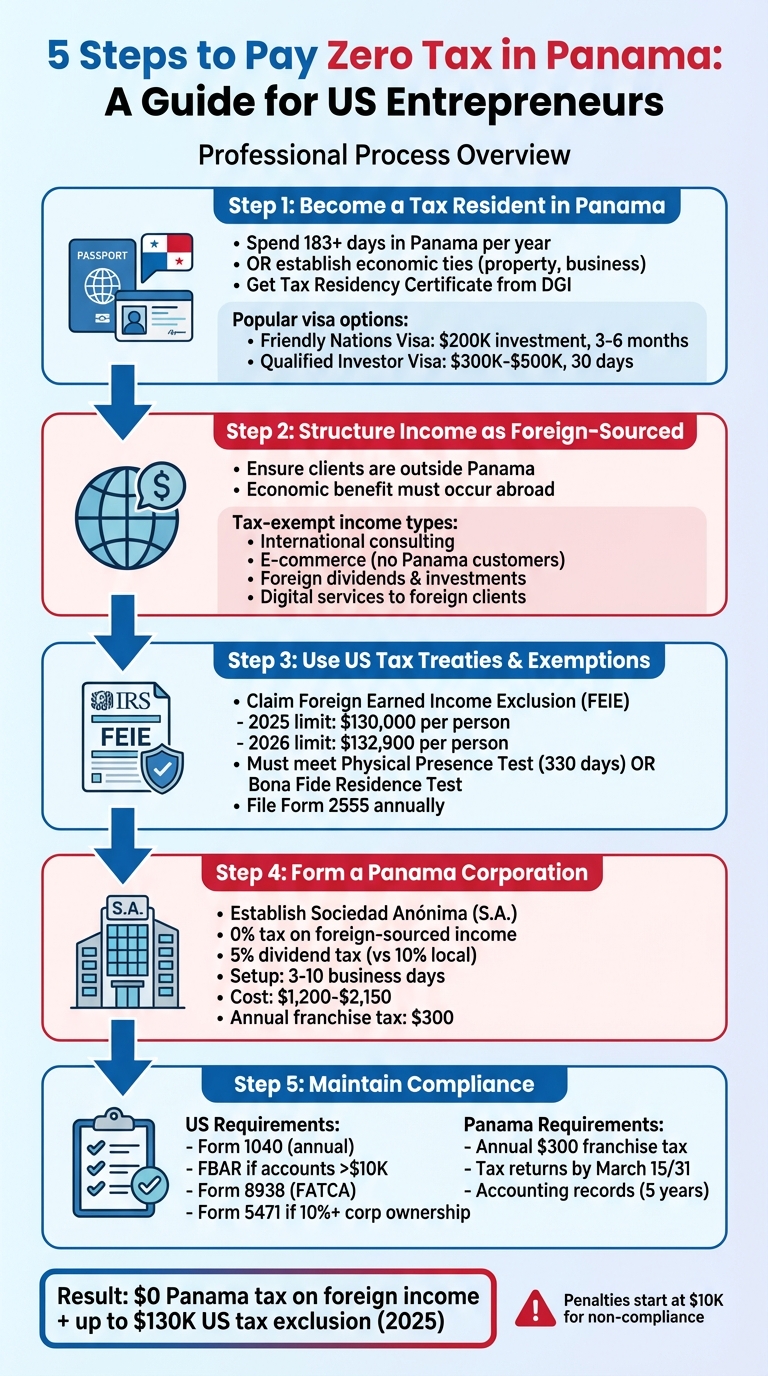

Want to legally pay zero tax on foreign income while living in Panama? Here’s how:

- Panama’s territorial tax system only taxes income earned within its borders. Foreign-sourced income (like consulting, e-commerce, or investments abroad) is completely tax-free.

- Residency is key. Spend at least 183 days in Panama or establish economic ties (property, business, etc.) to qualify as a tax resident and claim Panama’s tax benefits.

- Combine with U.S. tax breaks. Use the Foreign Earned Income Exclusion (FEIE) to exclude up to $130,000 of foreign income (2025) from U.S. taxes.

- Set up a Panama corporation. A Sociedad Anónima (S.A.) lets you run a business with 0% corporate tax on foreign income. Maintain compliance with both Panamanian and U.S. regulations.

How Panama’s Territorial Tax System Works

Panama takes a unique approach to taxation by only taxing income generated within its borders. This is in stark contrast to the U.S. system, which taxes worldwide income. The foundation of this policy lies in Article 694 of Panama’s Tax Code, which applies to everyone, regardless of their citizenship or residency status. For example, if you’re operating a consulting business from Panama City but your clients are based in the United States, that income is entirely exempt from Panamanian taxes. Similarly, dividends from foreign companies, interest from overseas accounts, and profits from e-commerce businesses (where goods never enter Panama) also fall outside the scope of local taxation. This clear separation makes it essential to categorize and document income properly.

"The Panama territorial tax system operates on the principle that income tax liability is determined strictly by the source of the income, rather than the nationality or residency of the recipient." – Pacific Legal

What Qualifies as Foreign-Sourced Income

The cornerstone of Panama’s territorial tax system is determining where the economic benefit of a service occurs, not where the work is physically performed. For instance, if you’re a software developer living in Panama and building applications for U.S. clients, your income counts as foreign-sourced because the client is abroad and the product is used outside Panama. To support this tax position, it’s crucial to maintain clear documentation like contracts and invoices that specify where the services are used.

Here are some common types of foreign-sourced income:

- Business profits: Revenue from operations conducted entirely outside Panama, such as international e-commerce or re-invoicing where goods never touch Panamanian soil.

- Professional and consulting services: Services provided from Panama but exclusively used by clients overseas.

- Investment income: Earnings from foreign sources, including dividends from overseas companies, interest on foreign bank accounts, and capital gains from international asset sales.

- Digital services: Income from online activities like software development, graphic design, or selling courses to customers outside Panama.

Some local-source incomes also enjoy exemptions. For example, interest earned on savings accounts, time deposits in Panamanian banks, and Panamanian government securities is not taxed. Understanding these distinctions is key to navigating the tax system effectively.

Panama Tax Rates and Exemptions

While foreign-sourced income is fully exempt, income generated within Panama is subject to taxation. For individual residents, the first $11,000 of Panamanian-sourced income is tax-free. Income between $11,001 and $50,000 is taxed at 15%, while anything above $50,000 is taxed at 25%.

| Annual Taxable Income (USD) | Tax Rate |

|---|---|

| $0 – $11,000 | 0% |

| $11,001 – $50,000 | 15% |

| Over $50,000 | 25% |

For corporations, the tax rate on local-source income is a flat 25%. However, if a Panamanian corporation operates exclusively with international clients and has no local sales, it pays zero corporate income tax. Such corporations are still required to pay a $300 annual franchise tax to stay compliant.

Dividend taxation in Panama operates on a two-tier system: dividends from foreign-sourced income are subject to a 5% withholding tax, while dividends from local-sourced income incur a 10% tax.

Beyond income taxes, Panama does not impose wealth taxes, inheritance taxes for direct heirs, or gift taxes. The standard Value Added Tax (ITBMS) is 7%, and owner-occupied primary residences valued at up to $120,000 are exempt from property tax. Combined with the use of the U.S. Dollar as legal tender, these features make Panama an attractive choice for entrepreneurs looking to structure their operations around foreign-sourced income.

sbb-itb-39d39a6

Step 1: Become a Tax Resident in Panama

Becoming a tax resident is the first step to taking advantage of Panama’s territorial tax system. Unlike a residency permit, tax residency determines your tax obligations. Without this status, you cannot legally enjoy zero taxes on foreign-sourced income or claim the Foreign Earned Income Exclusion on your U.S. tax return.

To qualify, you need to spend at least 183 days in Panama within a calendar year. These days don’t have to be consecutive – you can come and go as needed. Alternatively, you can establish Panama as your "economic and family center of interest" by owning property, running a local business, or maintaining close family ties. Once you meet the requirements, you can apply for a Tax Residency Certificate from the Directorate General of Revenue (DGI). This certificate serves as official proof for both Panamanian and U.S. tax authorities.

"Establishing your tax residency in Panama is not an evasion strategy; it’s a smart optimization decision. It’s about legally structuring your finances to protect your assets and maximize your growth in a global economy." – PanamaWay

Residency Programs for Entrepreneurs

For U.S. citizens, Panama offers several pathways to legal residency, with the Friendly Nations Visa being a popular choice for entrepreneurs. This program allows you to demonstrate economic or professional ties to Panama through one of three options:

- Purchasing property worth at least $200,000

- Placing $200,000 in a fixed-term deposit with a Panamanian national bank for at least three years

- Securing a work contract with a Panamanian company

Another option is the Qualified Investor Visa, which offers permanent residency in just 30 days. However, it requires a larger real estate investment of $300,000 to $500,000. Note that the $300,000 minimum is a limited-time offer and is expected to increase.

| Visa Program | Minimum Investment | Approval Time | Residency Status |

|---|---|---|---|

| Friendly Nations Visa | $200,000 (Real Estate/Deposit) or Employment | 3–6 Months | 2-year provisional, then permanent |

| Qualified Investor Visa | $300,000–$500,000 | 30 Days | Immediate Permanent Residency |

Both programs lead to a permanent residency card (E-cedula), which also functions as your Panamanian tax ID. While the Friendly Nations Visa usually results in permanent residency within six months, the Qualified Investor Visa speeds up the process for those willing to make a larger investment.

How to Apply for Residency

Once you’ve decided on a visa program, you’ll need to start the application process. All residency applications in Panama must be handled by a licensed local attorney. Your attorney will guide you, but you’ll need to prepare certain documents. For U.S. citizens, this includes an FBI criminal background check (apostilled before leaving the U.S.), as well as apostilled and translated birth certificates and marriage licenses. Translations must be done by a certified Panamanian translator.

On average, the costs are around $5,000 per person, not including travel and accommodation. This breaks down as follows:

- $2,000 in attorney fees

- $900 to $1,600 for company incorporation (if required)

- $800 for a mandatory deportation retainer

- Various government fees

- A $5,000 minimum deposit into a Panamanian bank account

- $2,000 per dependent

Once you begin the application process, do not leave Panama until you’ve received your multiple-entry visa, which typically takes 10 to 14 days. Leaving before this could result in a $2,000 fine. After obtaining your permanent residency card, wait about 30 days before applying for your E-cedula, which serves as both your national ID and tax identification number.

Finally, once you’ve secured legal residency and met the 183-day physical presence requirement, apply for your Tax Residency Certificate with the DGI. Be sure to include supporting documents like passport stamps, utility bills, and lease agreements. This certificate is essential for proving to the IRS that you are subject to Panama’s tax system, allowing you to access Panama’s territorial tax benefits. Establishing tax residency in Panama is the cornerstone of leveraging its favorable tax system.

Step 2: Structure Your Income as Foreign-Sourced

Once you’ve secured tax residency in Panama, the next critical step is ensuring your income is categorized correctly to maintain its tax-exempt status. Panama only taxes income generated within its borders, so understanding how to structure your revenue streams is essential.

Panama uses an "economic use test" to determine the source of income. Essentially, the taxability of your earnings depends on where the economic benefit of your services is realized. For instance, if you’re working from an office in Panama City but providing consulting services to a U.S. company for its American operations, that income is considered foreign-sourced since the economic benefit occurs outside of Panama.

"In practical terms, a company with an office and employees based in Panama does not pay any income tax, if it only performs international operations from Panama." – Business Panama

To keep your tax-exempt status, you need to steer clear of providing services to Panamanian companies or managing local assets. Even offering advice to a Panamanian subsidiary of a foreign company could result in local taxation if it impacts Panama’s economy. The Panamanian tax authority (DGI) closely examines the economic reality of your operations, so it’s important to document where your services are used, where decisions are made, and where value is created.

Operating a Business Outside Panama

If you’re running a business from Panama but aiming to keep your income tax-exempt, you’ll need to structure your operations carefully. Contracts and invoices should explicitly state that your services are exclusively for foreign entities, and payments should be routed through foreign bank accounts.

Many U.S. business owners use Panamanian corporations, such as a Sociedad Anónima (S.A.), to bill international clients. These entities enjoy a 0% corporate tax rate on foreign-sourced income and benefit from a reduced 5% dividend withholding tax on foreign earnings, compared to the 10% rate applied to local income. To ensure compliance, document management decisions with detailed meeting minutes and resolutions to demonstrate that operations align with global business practices. Keep in mind that under Law 254 of 2021, all Panamanian entities – even those with only foreign income – must maintain accounting records and submit them annually to their Resident Agent. If your business serves both local and international clients, separate accounting records are essential to avoid reclassification of foreign-sourced income.

Common Types of Foreign-Sourced Income

To fully benefit from Panama’s tax exemptions, you need to identify and categorize your income properly. Here are some examples of income that qualify as foreign-sourced:

- International consulting and professional services: Services like management consulting, legal advice, accounting, or marketing strategies provided to foreign companies qualify when the economic benefit is realized outside Panama.

- E-commerce and online businesses: If your business has no Panamanian customers or operations, such as selling software subscriptions, digital products, or online courses internationally, it’s completely tax-exempt.

- Re-invoicing operations: Transactions where merchandise never physically enters Panama are classified as foreign-sourced income.

- Dividends: Dividends from income generated outside Panama are considered foreign-sourced and benefit from a reduced withholding tax rate.

| Income Type | Classification | Tax Rate |

|---|---|---|

| Consulting for a U.S. company on U.S. market strategy | Foreign Source | 0% |

| Software sold to foreign businesses | Foreign Source | 0% |

| Consulting for a Panamanian company | Local Source | 25% |

| Sale of Panama real estate | Local Source | 25% |

While Panama won’t tax your foreign-sourced income, U.S. citizens remain subject to U.S. tax obligations. However, the Foreign Earned Income Exclusion (approximately $130,000 for 2025) can help reduce your U.S. tax liability, making Panama’s territorial tax system even more attractive for U.S. entrepreneurs. As always, thorough documentation is key to staying compliant with both Panamanian and U.S. tax laws.

Step 3: Use US Tax Treaties and Exemptions

The US and Panama don’t have a formal income tax treaty. This means you can’t rely on bilateral agreements to avoid double taxation. Instead, you’ll need to use IRS tools like the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC) to lower your US tax obligations while living in Panama. By taking advantage of Panama’s 0% tax on foreign-sourced income and pairing it with the FEIE, US entrepreneurs can potentially reduce their tax liability to almost nothing. However, this approach requires strict compliance with IRS rules and filing the necessary forms. Missing even one filing can result in penalties starting at $10,000. Properly utilizing these IRS mechanisms alongside Panama’s tax-friendly system is essential to minimizing taxes.

Claiming the Foreign Earned Income Exclusion

The FEIE allows you to exclude a portion of your foreign-earned income from US federal taxes. For the 2025 tax year, the exclusion limit is $130,000, increasing to $132,900 in 2026. For married couples where both spouses qualify, the combined limit rises to $265,800 in 2026.

To claim the FEIE, you need to establish a tax home in Panama – essentially, your main place of work or business – and pass either the Physical Presence Test or the Bona Fide Residence Test.

- The Physical Presence Test requires you to spend at least 330 full days in a foreign country during any 12-month period. Be meticulous about tracking your travel, as even a short US layover counts as a US day and could disqualify you.

- The Bona Fide Residence Test requires uninterrupted residency in Panama for a full tax year (January 1 to December 31). Strengthen your claim by obtaining a Panamanian national ID card (e-cedula), a local driver’s license, and a taxpayer identification number (NIT).

"The ‘E-Cedula’… is primary evidence used to pass the Bona Fide Residence Test on IRS Form 2555, allowing you to claim exclusions even if you spend more than 35 days a year in the U.S." – I Go Panama

While the FEIE can significantly lower your tax burden, it doesn’t eliminate self-employment taxes. The 15.3% US self-employment tax still applies, as there’s no totalization agreement between the US and Panama.

To claim the FEIE, you must file IRS Form 2555 with your annual tax return – it’s not automatic. Additionally, you may qualify for the Foreign Housing Exclusion, which lets you deduct housing costs (like rent and utilities) exceeding $15,750, up to a maximum of $39,000 for 2025.

| Tax Year | FEIE Exclusion Limit | Combined Limit (Married) |

|---|---|---|

| 2024 | $126,500 | $253,000 |

| 2025 | $130,000 | $260,000 |

| 2026 | $132,900 | $265,800 |

Meeting IRS Reporting Requirements

After establishing your tax home and meeting the FEIE tests, it’s critical to comply with IRS reporting standards.

US citizens are required to report their worldwide income, no matter where they live. Even if the FEIE reduces your taxable income to zero, you still need to file Form 1040 annually and submit additional forms to stay compliant.

Here are the key reporting requirements:

- FBAR (FinCEN Form 114): This is required if your foreign financial accounts exceed $10,000 at any point during the year. Penalties for non-willful violations start at $10,000, while willful violations can cost the greater of $100,000 or 50% of the account balance. The initial deadline is April 15, with an automatic extension to October 15.

- FATCA (Form 8938): You need to report foreign financial assets if they exceed certain thresholds. For single filers, the threshold is $200,000 on the last day of the year or $300,000 at any point during the year. Panamanian banks also report account data to the IRS under an Intergovernmental Agreement.

- Form 5471: If you own 10% or more of a Panamanian corporation (like a Sociedad Anónima), you must file this form. Failing to do so triggers an automatic $10,000 penalty.

| Reporting Requirement | Form | Threshold |

|---|---|---|

| FEIE Claim | Form 2555 | Must meet the Physical Presence or Bona Fide Residence Test |

| FBAR | FinCEN Form 114 | Total foreign account balances exceed $10,000 |

| FATCA | Form 8938 | > $200,000 (single) or > $400,000 (joint) on the last day of year |

| Foreign Corp. | Form 5471 | 10% or more ownership in a foreign corporation |

US expats get an automatic two-month extension to file their federal tax return (until June 15), but any taxes owed must still be paid by April 15 to avoid interest. Before moving to Panama, consider establishing residency in a state with no income tax – like Florida or Texas – to avoid state tax obligations, as the FEIE only applies to federal taxes.

Step 4: Form a Panama Corporation

Setting up a Panamanian corporation – referred to as a Sociedad Anónima (S.A.) – can be a smart move for U.S. entrepreneurs looking to reduce their tax liabilities. Thanks to Panama’s territorial tax system, income earned from clients or business activities outside of Panama is taxed at 0%. On top of that, the separation between personal and corporate assets provides added protection for your wealth while keeping tax commitments minimal.

A Panama S.A. also offers privacy benefits. Shareholder information is not publicly disclosed, and there are no restrictions on nationality or residency. Directors and shareholders can be from anywhere in the world and don’t need to live in Panama. Additionally, since Panama uses the U.S. Dollar as its official currency, entrepreneurs avoid currency exchange risks, making financial management simpler.

Advantages of Incorporating in Panama

One of the biggest perks is the tax advantage. If your business earns revenue from clients in the U.S., Europe, or other regions outside Panama, that income is exempt from Panamanian income tax. However, income generated within Panama is subject to a 25% corporate tax rate. Dividends from local income are taxed at 10%, while dividends from foreign-sourced income are taxed at a lower rate of 5%.

Another key benefit is asset protection. A Panama S.A. creates a legal buffer that separates your personal assets from business liabilities, shielding your wealth from lawsuits or creditor claims. Setting up a corporation in Panama is also relatively quick and straightforward, often taking just 3 to 10 business days. With over 60 international and local banks operating in the country, you’ll also have access to a well-established banking system.

Privacy is a core feature of a Panama S.A. While the names of directors are made public, shareholder details remain confidential. For those seeking even more privacy, nominee directors can be appointed, keeping your name out of public records entirely. Although the standard authorized capital is $10,000, there’s no requirement to pay this amount upfront.

How to Register a Panama Corporation

The process of registering a corporation in Panama is relatively simple but requires careful attention to certain steps. First, you’ll need to choose a unique company name with a suffix like S.A., Inc., or Corp. Typically, you’ll submit three name options to verify availability. Next, appoint at least three directors – a President, Secretary, and Treasurer – who can be individuals or legal entities from any country.

Every corporation must have a licensed Panamanian lawyer or law firm as its resident agent. This agent will prepare the Articles of Incorporation (also called the "Social Pact") in Spanish, notarize it with a Panamanian Notary Public, and file it with the Public Registry. Once the corporation is registered, you’ll need to obtain a Tax ID (RUC) from the Dirección General de Ingresos (DGI).

To legally operate, you’ll also need a Notice of Operations (Aviso de Operación), which can be obtained through the "Panama Emprende" platform. Fees for this range between $55 and $100, depending on your business type. Additionally, you’ll need to register with the local municipality (such as MUPA in Panama City) to pay local taxes and secure any necessary permits.

The final step involves opening a corporate bank account. Be prepared to meet strict Know Your Customer (KYC) requirements, which include providing passport copies, proof of address, professional references, and a detailed business plan. The approval process for a corporate bank account can take anywhere from 1 to 4 weeks, depending on the bank.

| Incorporation Step | Requirement | Timeline/Cost |

|---|---|---|

| Name Selection | Submit three name options via your resident agent | 1–2 days |

| Appoint Directors & Officers | Minimum of three (President, Secretary, Treasurer) | Immediate |

| Draft & Notarize Articles | Resident agent and notary involvement | 2–3 days |

| File with Public Registry | Filing with the Public Registry | 3–10 business days |

| Obtain Tax ID (RUC) | Register with DGI | 1–2 days |

| Notice of Operations | Approval via Panama Emprende | $55–$100 |

| Municipal Registration | Local registration (e.g., MUPA) | Varies |

| Open Corporate Bank Account | Setup with a Panamanian bank | 1–4 weeks |

The total cost to incorporate, including professional and registration fees, usually falls between $1,200 and $2,150. Additionally, an annual franchise tax (Tasa Única) of $300 is required to keep the corporation active. Under Law 52 of 2016, you’re also required to maintain accounting records and supporting documents for at least five years.

It’s crucial for U.S. entrepreneurs to understand that forming a Panama corporation does not exempt them from U.S. tax obligations. U.S. citizens are taxed on their global income, regardless of where they incorporate. To avoid compliance issues, work with a U.S.-qualified CPA to manage IRS reporting requirements, including those related to Controlled Foreign Corporations (CFC), Global Intangible Low-Taxed Income (GILTI), and Form 5471 if you own 10% or more of the corporation.

Step 5: Maintain Compliance in Both Countries

Once you’ve structured your income and set up your corporation, the next big task is staying compliant in both the U.S. and Panama. This step is crucial because U.S. citizens are taxed on their worldwide income, even though Panama uses a territorial tax system. Missing deadlines or failing to file required forms can lead to hefty penalties, so it’s important to fully understand your responsibilities in both countries.

U.S. Tax Filing Requirements

If your income exceeds the IRS thresholds, you must file Form 1040 annually, even if Panama doesn’t tax your income. U.S. expats get an automatic extension until June 15, but filing on time is essential if you want to claim benefits like the Foreign Earned Income Exclusion (FEIE) for the applicable tax year.

For those with foreign financial accounts totaling more than $10,000 at any point in the year, an FBAR (FinCEN Form 114) is required by October 15. Penalties for non-compliance can be steep – up to $10,000 for non-willful violations and, for willful violations, either $100,000 or 50% of the account balance, whichever is greater. Additionally, you’ll need to file Form 8938 under FATCA if your foreign assets surpass $200,000 at year-end or $300,000 at any point during the year (for single individuals living abroad).

If you hold at least 10% of a Panamanian corporation, you must submit Form 5471 along with your tax return. Late or incomplete filings automatically incur a $10,000 penalty. To ensure compliance, keep detailed records of your residency and income sources. For example, document your physical presence outside the U.S. to meet the 330-day physical presence test for the FEIE, and maintain a Panamanian bank account and address to establish Panama as your tax home.

While fulfilling U.S. tax obligations is essential, don’t overlook Panama’s requirements.

Panama Compliance Requirements

To keep your Panamanian corporation in good standing, you must pay an annual franchise tax (known as tasa única) of $300. Missing this payment can result in asset freezes, which will delay any transactions until the issue is resolved.

Individual tax returns in Panama are due by March 15, while corporate returns must be filed by March 31. If your income is entirely foreign-sourced, your Panamanian tax liability may be minimal or even nonexistent. However, you’ll need to obtain a Panamanian Tax ID number (NIT) for local filings, as it’s often required by banks as well. To strengthen your global tax strategy and guard against claims from other jurisdictions, it’s wise to get a Tax Residency Certificate.

Under FATCA, Panamanian banks are required to report information about U.S. account holders to the IRS. So, when opening local accounts, be ready to provide your Social Security Number and fill out Form W-9. Staying on top of these obligations allows you to enjoy the benefits of Panama’s territorial tax system without unnecessary hiccups.

How Global Wealth Protection Can Help

Navigating Panama’s territorial tax system while staying compliant with U.S. regulations – covering residency, corporate formation, and tax reporting – can feel overwhelming. That’s where Global Wealth Protection steps in. They specialize in helping U.S. entrepreneurs create tailored international tax strategies, so you can focus on growing your business while leaving the complexities of compliance to the experts. Their services are designed to make the most of Panama’s tax advantages while ensuring a smooth process for you. Let’s break down how they simplify residency and corporate structuring for U.S. entrepreneurs.

Custom Solutions for U.S. Entrepreneurs

Global Wealth Protection offers hands-on support throughout your Panama tax planning journey. Whether you’re considering the Friendly Nations Visa, Investor Visa, or Pensioner Visa, their team helps you choose the best residency option for your specific situation.

They also assist in securing your Tax Residency Certificate, a critical document for establishing your tax residency under Panama’s territorial tax system.

When it comes to corporate structuring, they provide guidance on forming offshore companies in locations like Panama and Anguilla. Whether you need a corporation or an LLC, they’ll help you customize the structure to fit your business goals. Additionally, their Resident Agent services ensure compliance with Panama’s Law 254 of 2021, which includes maintaining accurate accounting records to avoid penalties.

GWP Insiders Membership Benefits

Global Wealth Protection goes a step further with their GWP Insiders Membership, offering ongoing resources and support for entrepreneurs looking to expand internationally. Members benefit from consultations that address both U.S. and Panamanian tax obligations, including help with the Foreign Earned Income Exclusion (FEIE), FBAR, FATCA reporting, and Form 5471 for foreign corporations.

The membership also provides access to strategies for reducing tax liabilities, guidance on selecting the right jurisdictions, and step-by-step plans to establish and maintain your presence in Panama. This program is particularly helpful for entrepreneurs who need continuous support as tax laws change or as their businesses evolve. With GWP Insiders, you’re not just getting advice – you’re building a long-term partnership that keeps you ahead of compliance challenges in both the U.S. and Panama.

Conclusion

Panama’s territorial tax system offers a pathway to zero tax liability for U.S. entrepreneurs who carefully structure their financial and business operations. By following a five-step process – obtaining legal residency, categorizing income as foreign-sourced, utilizing U.S. tax exclusions like the FEIE, incorporating a Panamanian entity, and ensuring compliance with both countries’ regulations – you can legally operate without paying taxes on foreign income while adhering to the rules.

The key is that Panama only taxes income earned within its borders. This means your earnings from activities like e-commerce, consulting, or international investments remain entirely tax-exempt if sourced outside Panama’s jurisdiction. When paired with the FEIE, this approach allows you to optimize your tax situation while staying within legal boundaries.

That said, implementing this strategy requires strict compliance with Panamanian and U.S. laws. Staying tax-efficient involves meeting several obligations, such as maintaining a physical presence in Panama for at least 183 days per year, keeping detailed accounting records under Law 254 of 2021, and filing all necessary U.S. forms. For instance, failing to submit IRS Form 5471 could result in an immediate $10,000 penalty. Staying diligent with these requirements is essential to avoid costly mistakes.

FAQs

What mistakes can make my income “Panama-sourced” by accident?

Common pitfalls include generating income through activities within Panama, such as offering services, selling products locally, or setting up a physical presence like an office or hiring employees. Additionally, mistakes like mislabeling foreign income as Panama-sourced or improperly organizing business entities can result in unexpected taxation. To steer clear of these issues, it’s crucial to plan thoroughly, define operational boundaries clearly, and seek advice from legal or tax experts well-versed in Panama’s tax regulations.

Can I still owe U.S. self-employment tax while living in Panama?

U.S. citizens are required to report and pay self-employment tax on their worldwide income, even while residing in Panama. Living abroad does not exempt individuals from this responsibility, as the U.S. taxes global earnings, including income from self-employment.

What records do I need to prove Panama tax residency and foreign-sourced income?

To establish tax residency in Panama, you’ll need specific documents. These include notarized copies of your passport, proof of a local address (such as a utility bill), and evidence that you’ve spent more than 183 days in Panama. If applicable, you may also need business or investment records.

For income sourced outside Panama, you’ll need to provide supporting documents like bank statements, tax declarations, or other financial records that confirm your income originates from abroad. Under Panama’s territorial tax system, only income earned within the country is subject to taxation.